Loading price data

This is the Global Economic, Commodities, Scrap Metal and Recycling Report, by our BENLEE Roll off Trailer and Gondola Trailer, November 2nd, 2020.

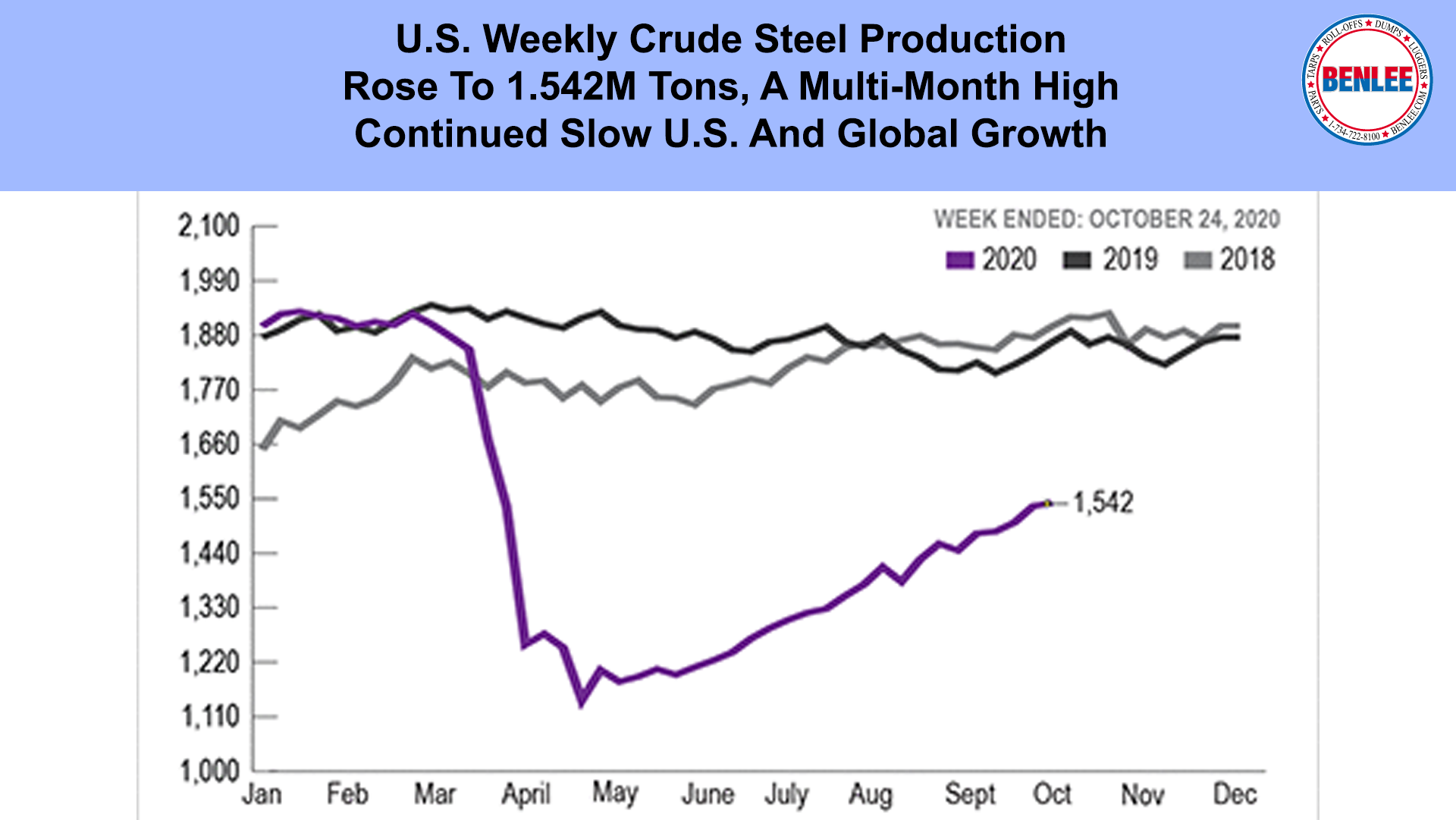

U.S. Weekly crude steel production rose to 1.542 M Tons a multi-month high on continued slow U.S. and global growth.

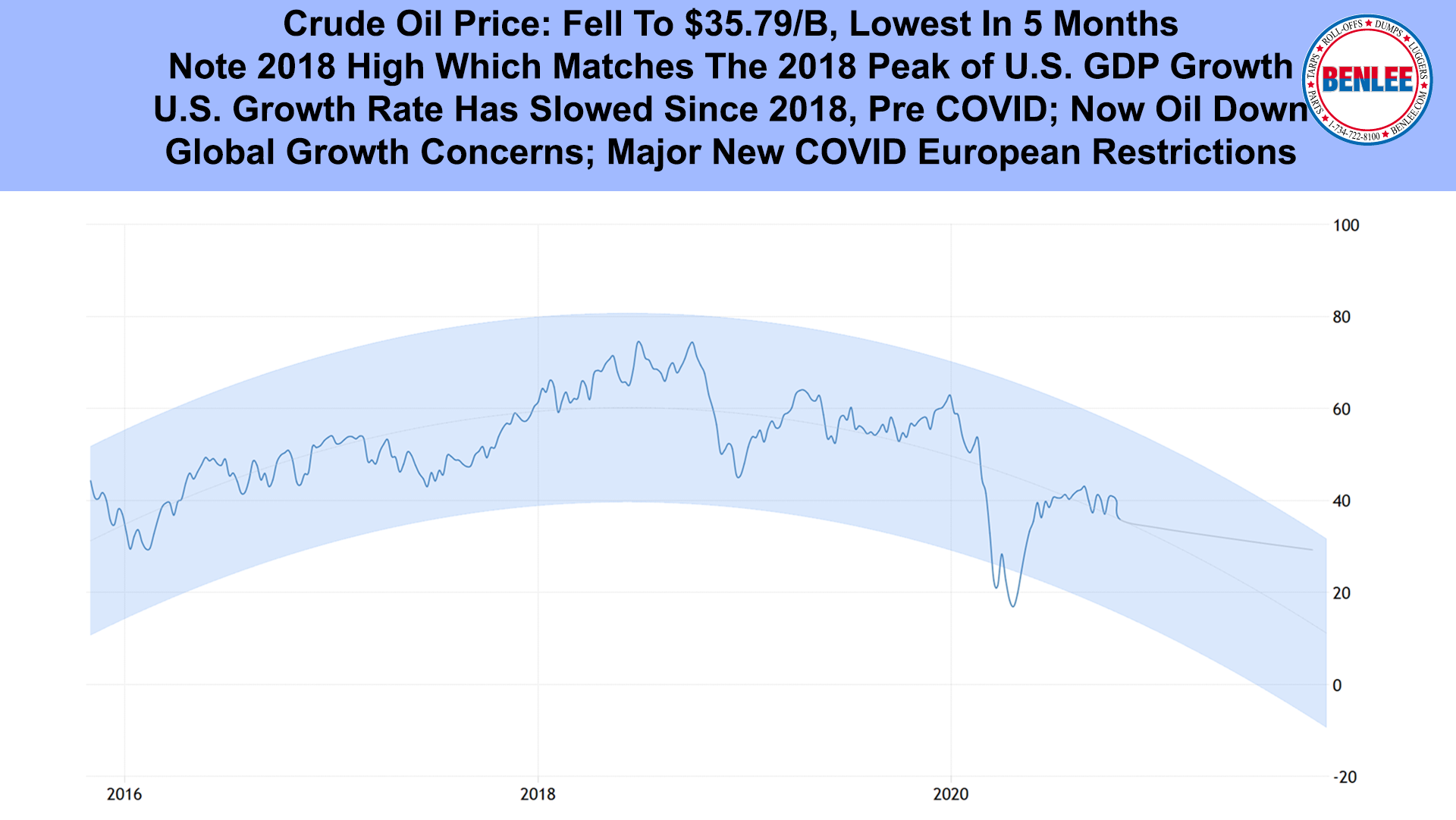

Crude Oil price fell to $35.79/b, the lowest in 5 months. Note the 2018 high, which matches the 2018 peak of U.S. GDP growth. Importantly the U.S. growth rate has slowed since 2018, pre COVID. Now oil is down on global growth concerns as there are major new COVID European restrictions.

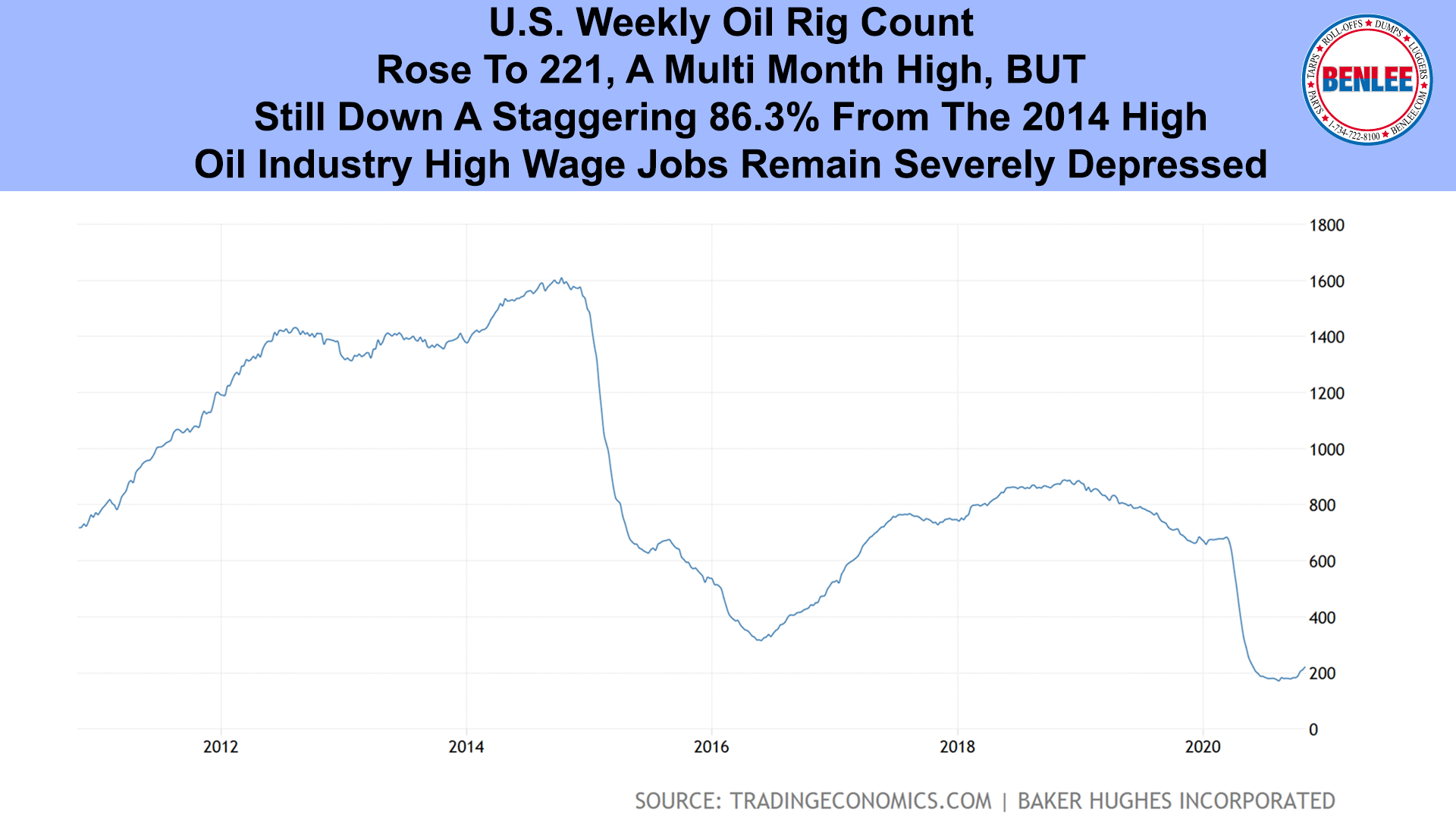

The U.S. weekly Oil rig count rose to 221, a multi month high, but it is still down a staggering 86.3% from the 2014 high. Oil industry high wage jobs remain severely depressed.

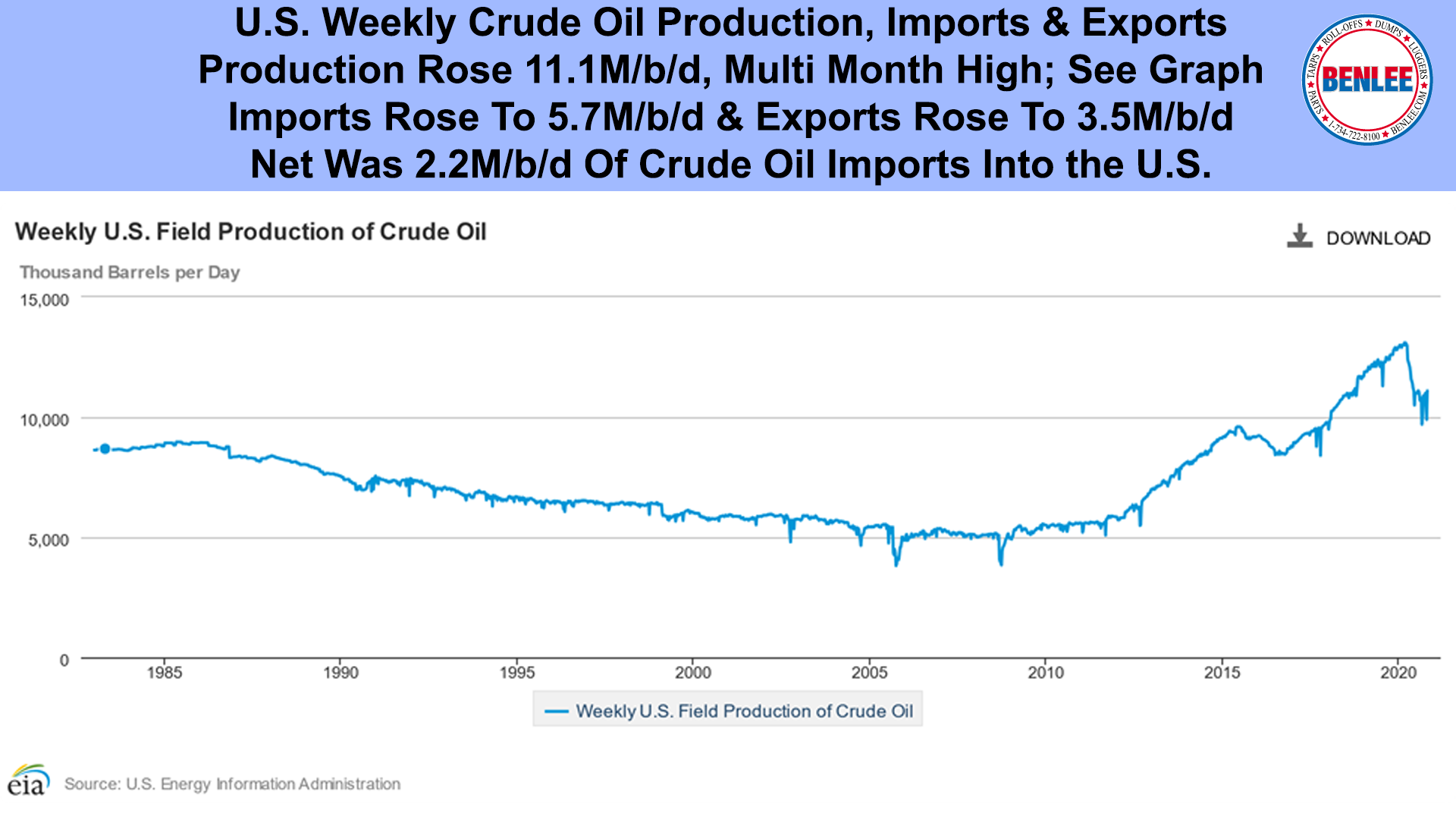

U.S. weekly crude oil production, imports and exports. Production rose to 11.1M/b/d, a multi month high. See Graph. Imports rose to 5.7m/b/d and exports rose to 3.5m/b/d, so the net was 2.2m/b/d of crude oil imports into the U.S.

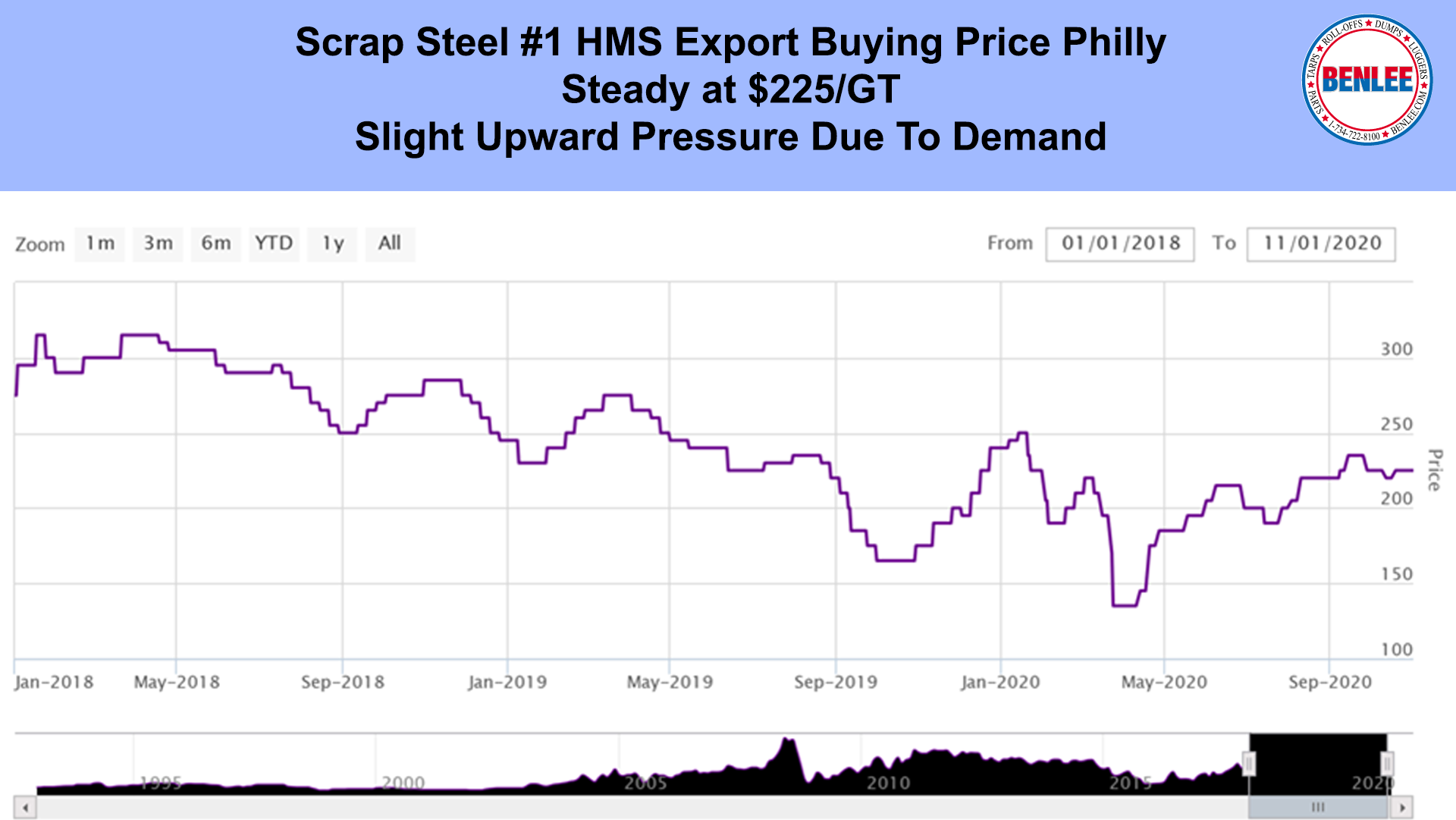

Scrap Steel #1 HMS Export buying price Philly, remained steady at $225/GT on slight upward pressure due to demand.

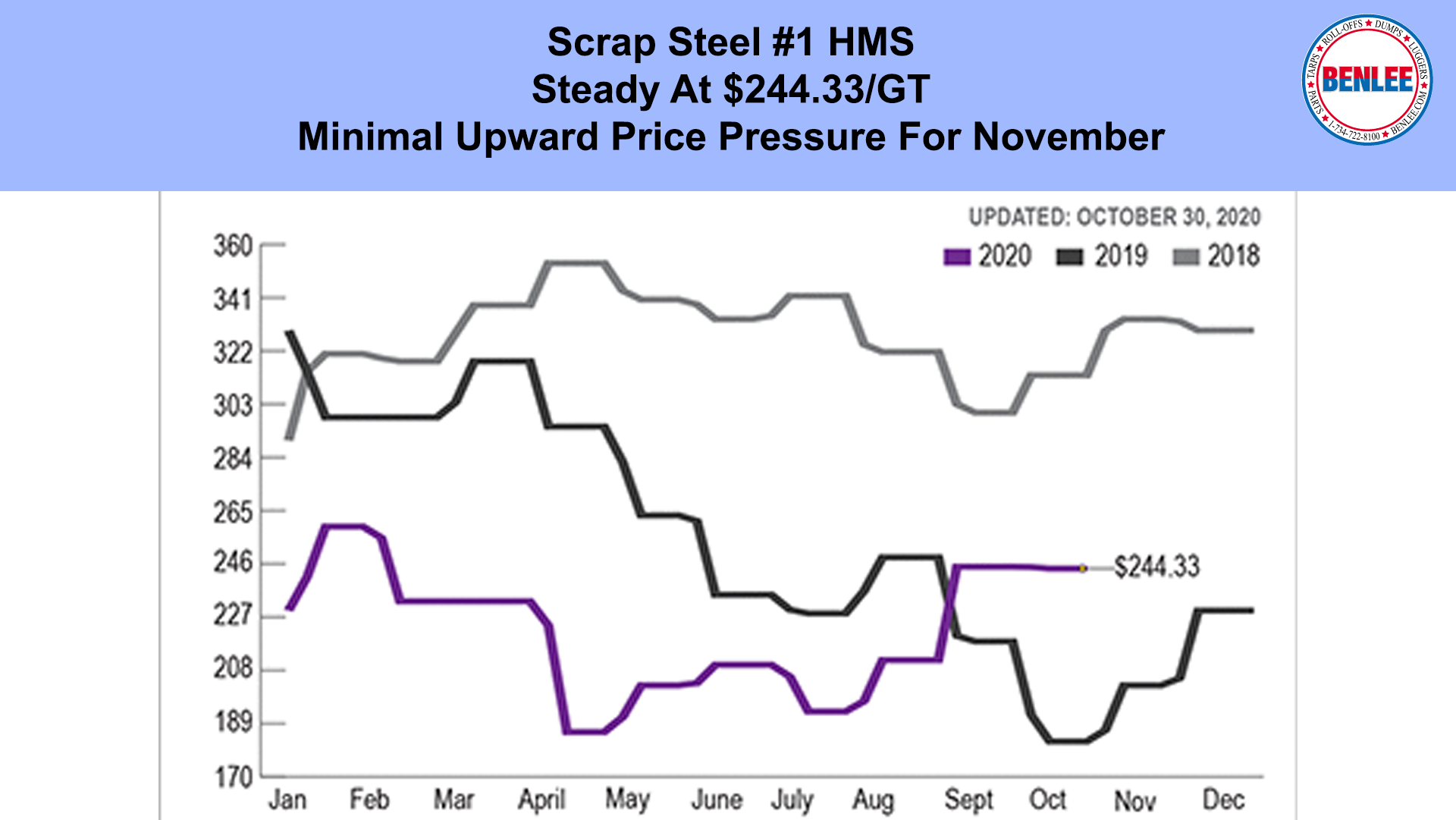

Scrap steel #1 HMS price was mostly steady at $244.33/GT with minimal upward price pressure for November.

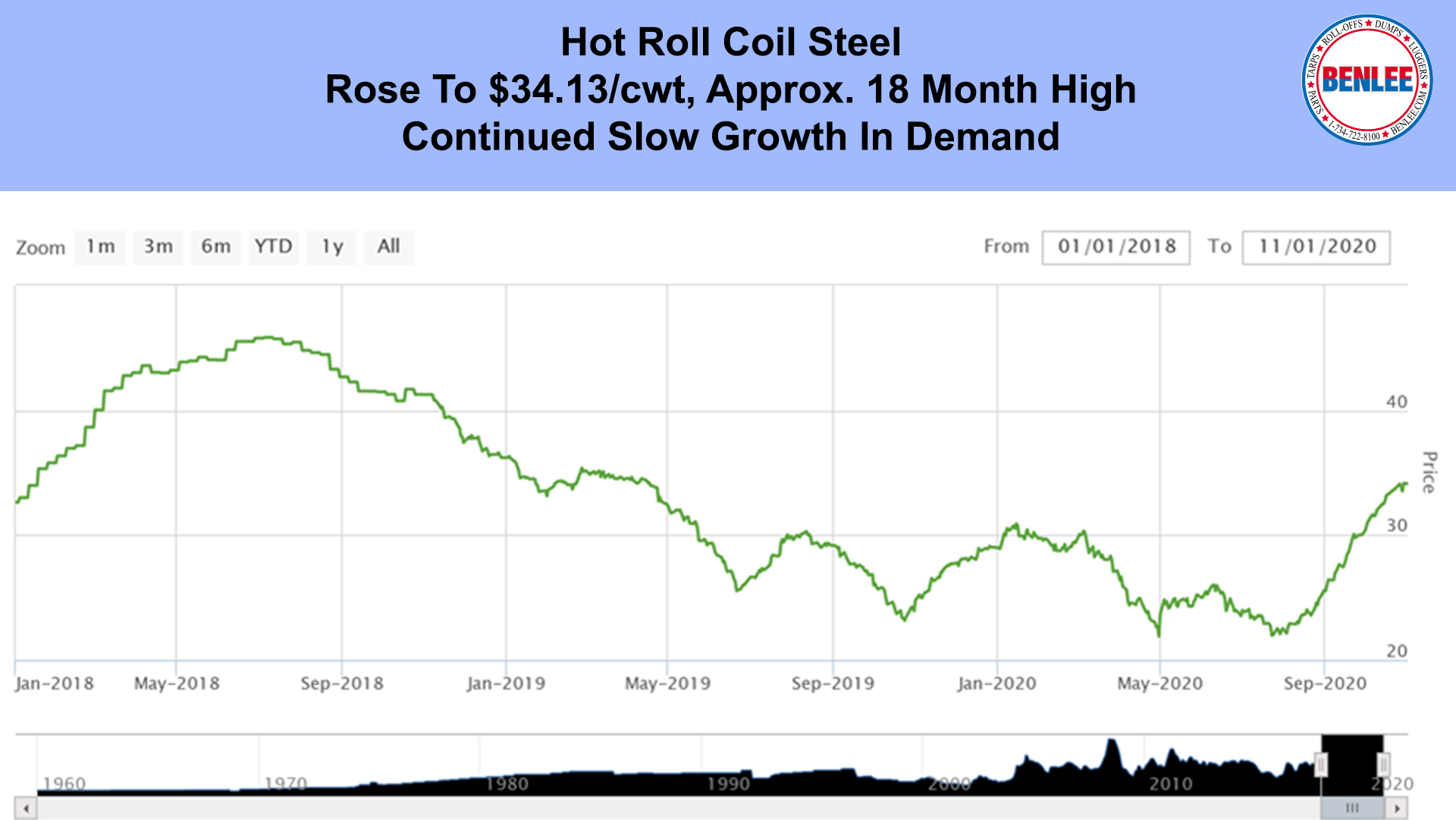

Hot Roll Coil steel rose to $34.13/cwt, an approximate 18 month high on continued slow growth in demand.

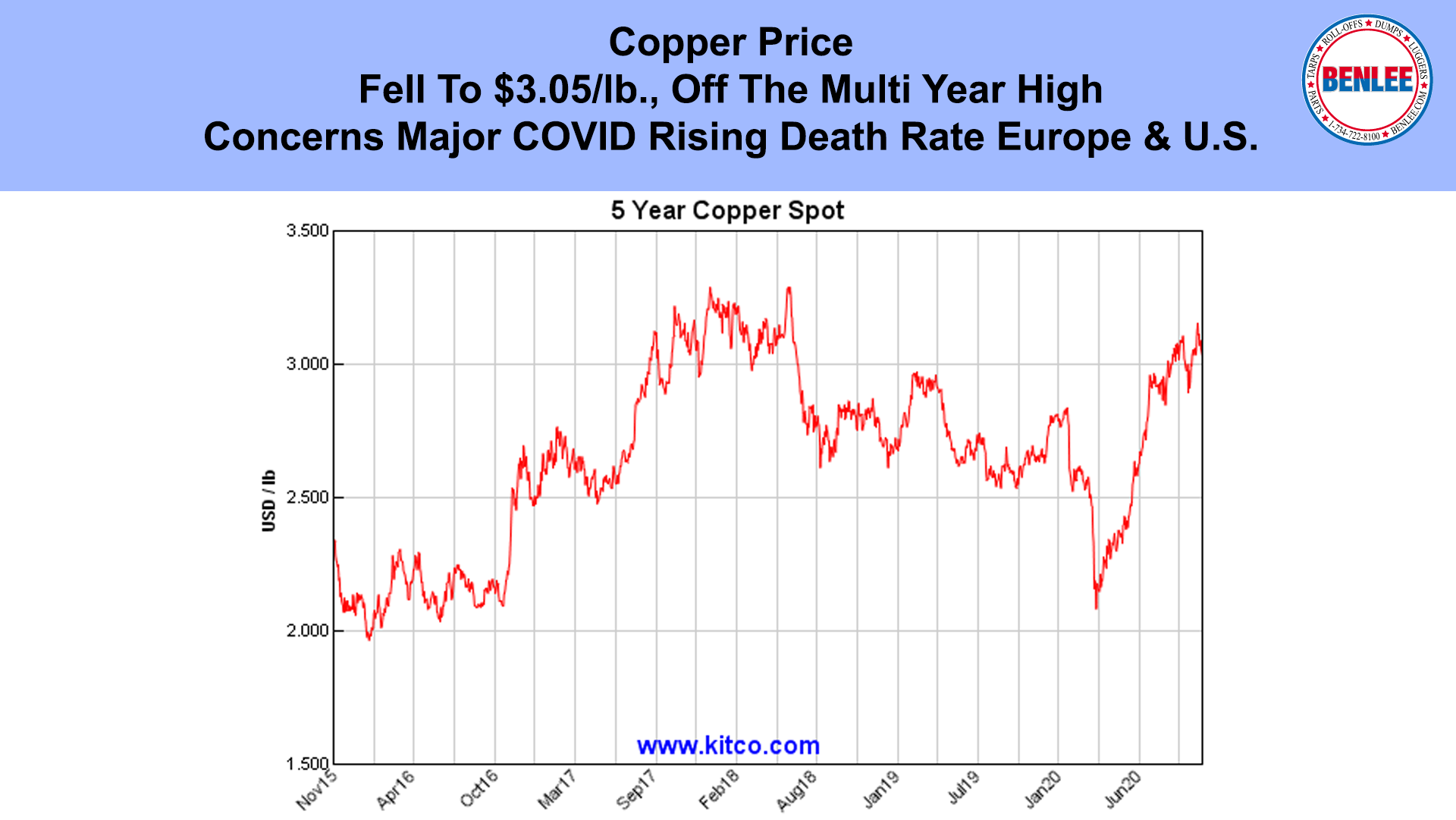

Copper Price fell to $3.05/lb. off the multi-year high on concern about the major rising COVID death rate, in Europe and the U.S.

Aluminum price fell to 82.3 cents per pound, off the multi-month high, on the same COVID concerns and its effect on global economic growth.

China’s October CAXIN manufacturing index fell to 51.4, meaning slower growth as COVID is causing slow global growth, so hurts China’s exports, but note the 2018 recovery from U.S. tariffs and February’s COVID crash.

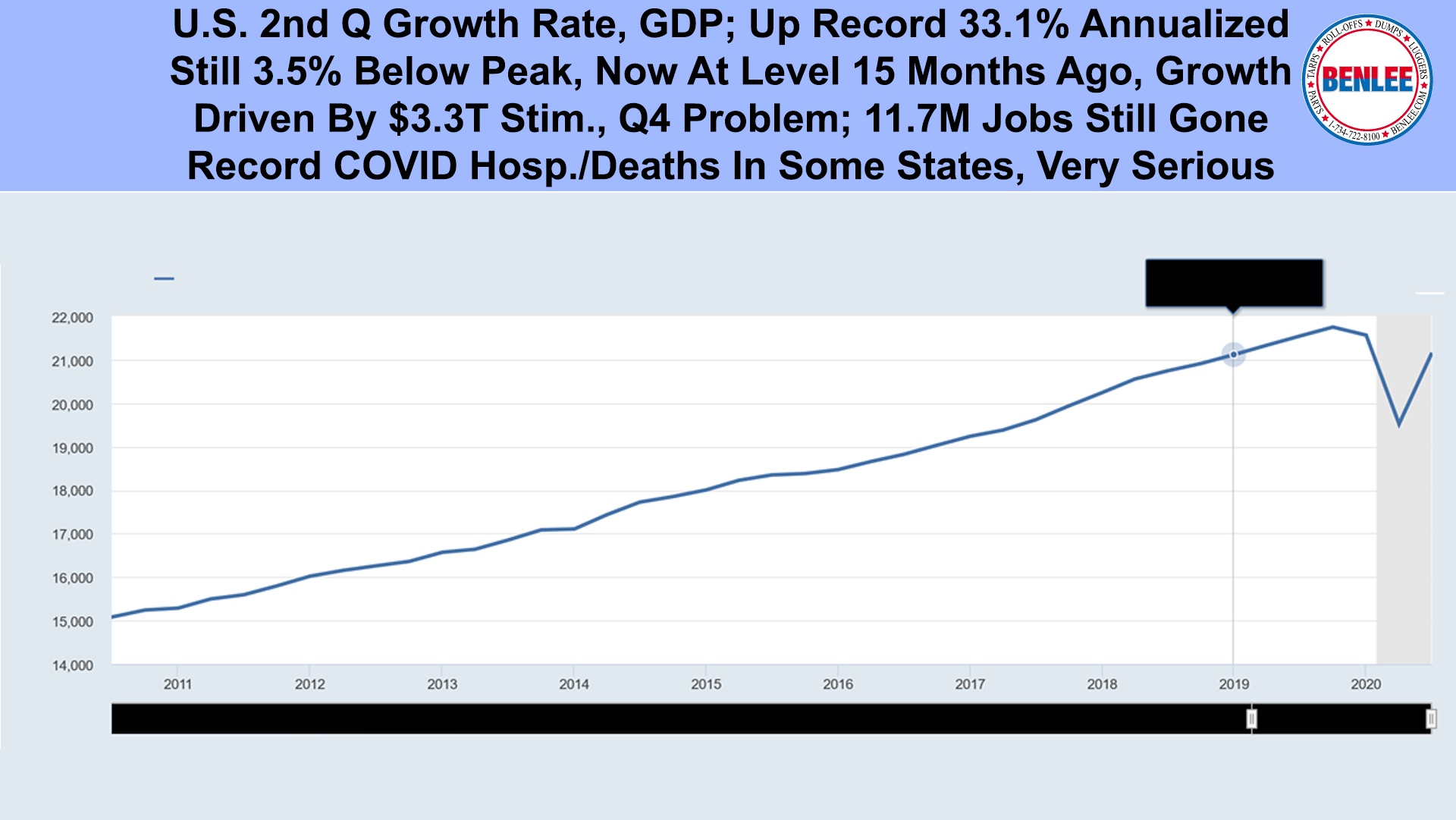

The U.S. 2nd Q growth rate, GDP was up a record 33.1% annualized, but is still 3.5% below the peak, so now at the level of 15 months ago. Growth was driven by the $3.3T stimulus. Q4 is a problem with 11.7M jobs still gone. Also record COVID hospitalizations and deaths in some state is very serious.

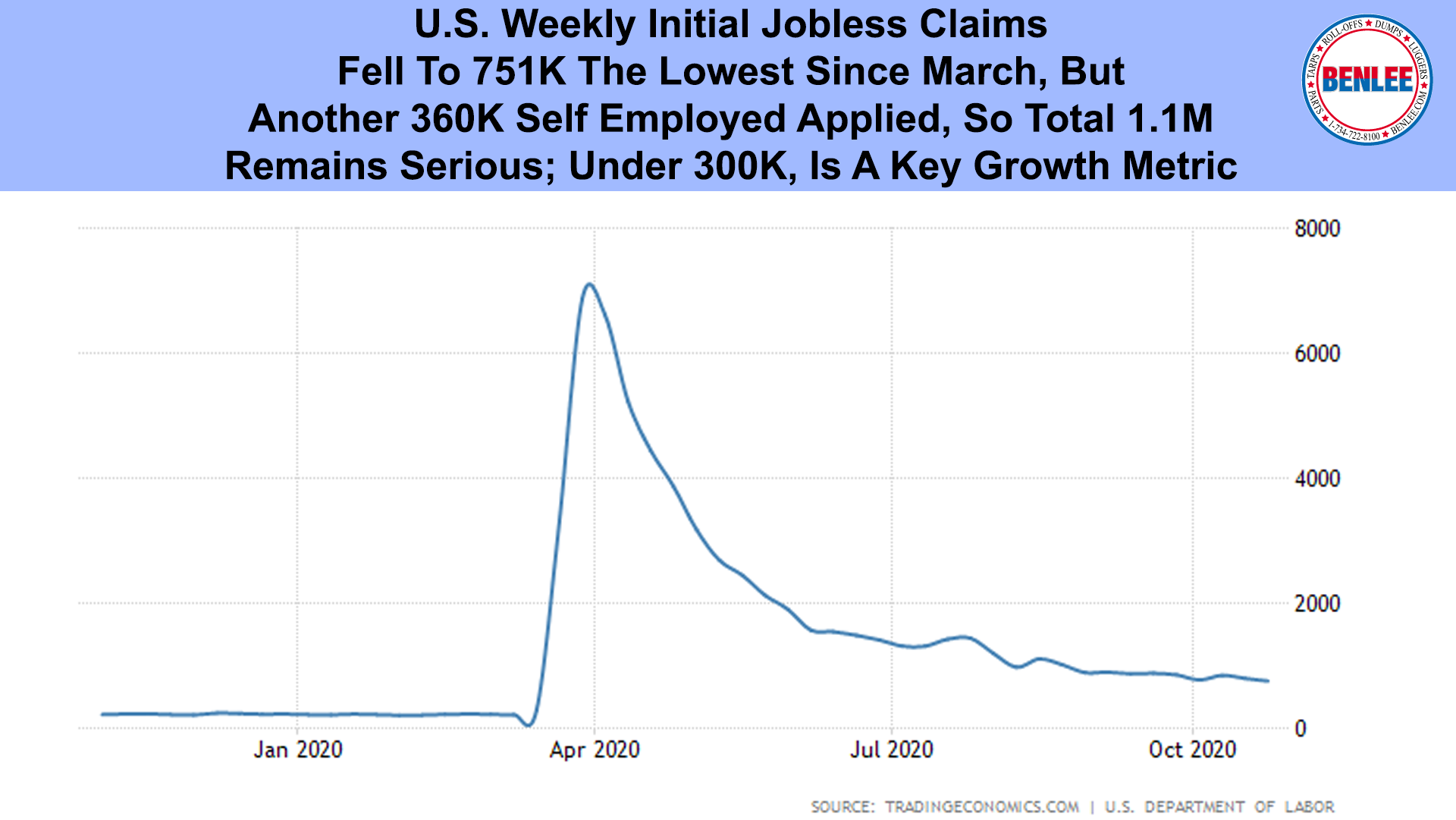

U.S. Weekly initial jobless claims fell to 751,000 the lowest since March, but another 360K self-employed people also applied, so the total was 1.1M. This remains serious in that under 300K is a key growth metric.

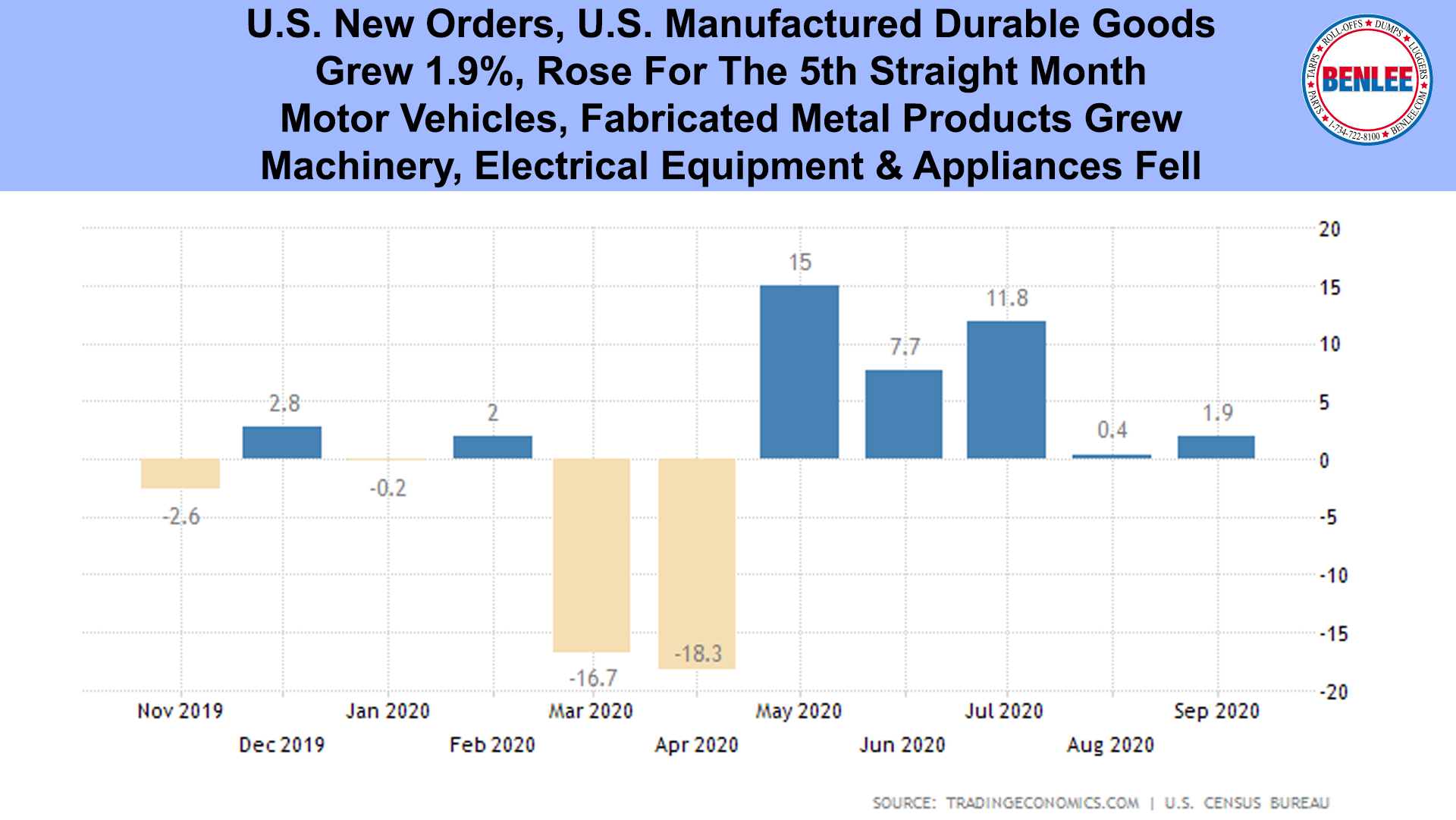

U.S. new orders for U.S. Manufactured durable goods for September grew 1.9% and rose for the 5th Straight month. Motor vehicles and fabricated metal products grew, as machinery, electrical equipment and appliances fell.

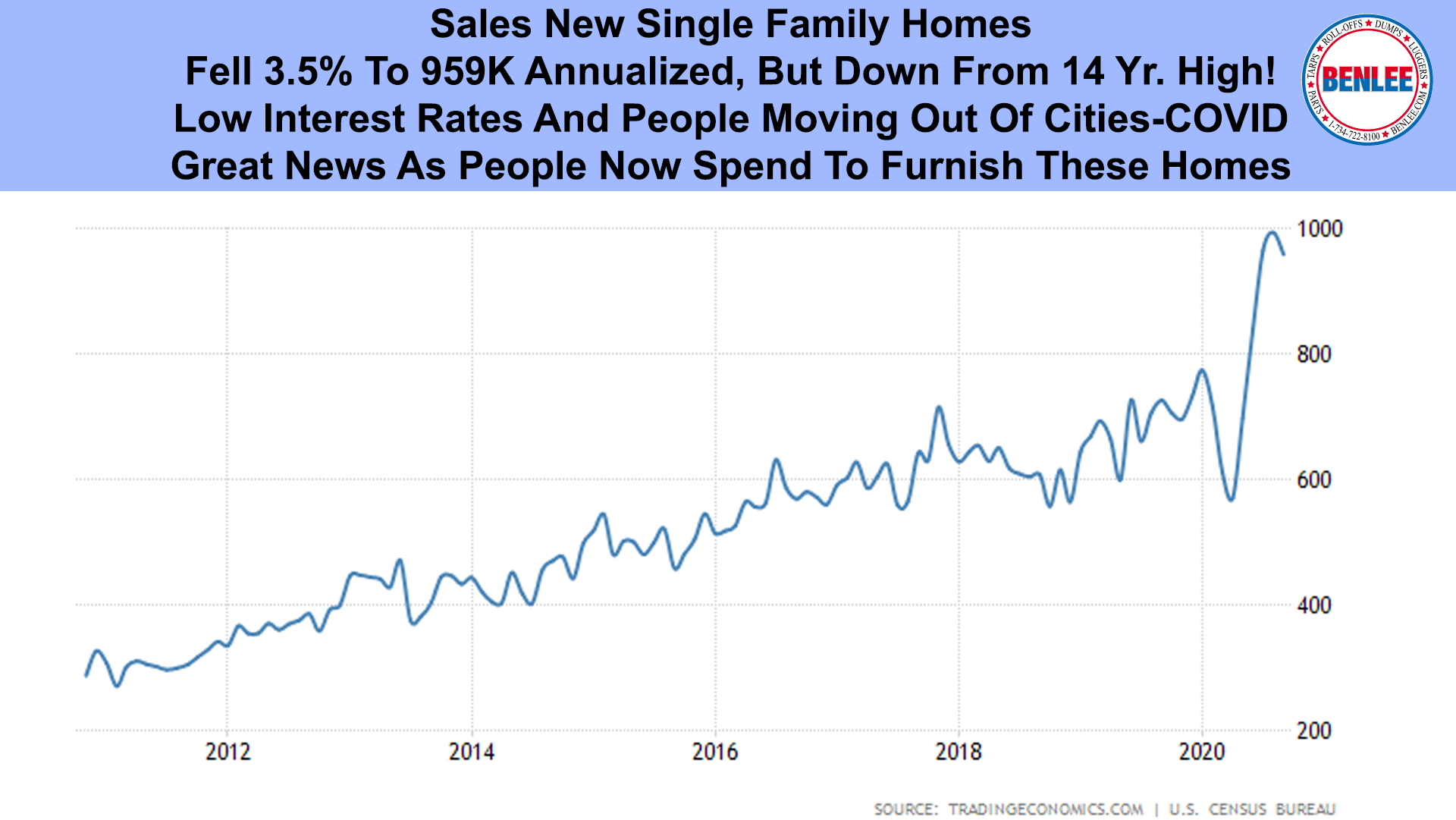

Sales of New Single-family homes for September fell 3.5% to 959,000 annualized, but down from a 14-year high. This is driven by record low interest rates and people moving out of cities due to COVID. This is great news as people will now spend to furnish these homes.

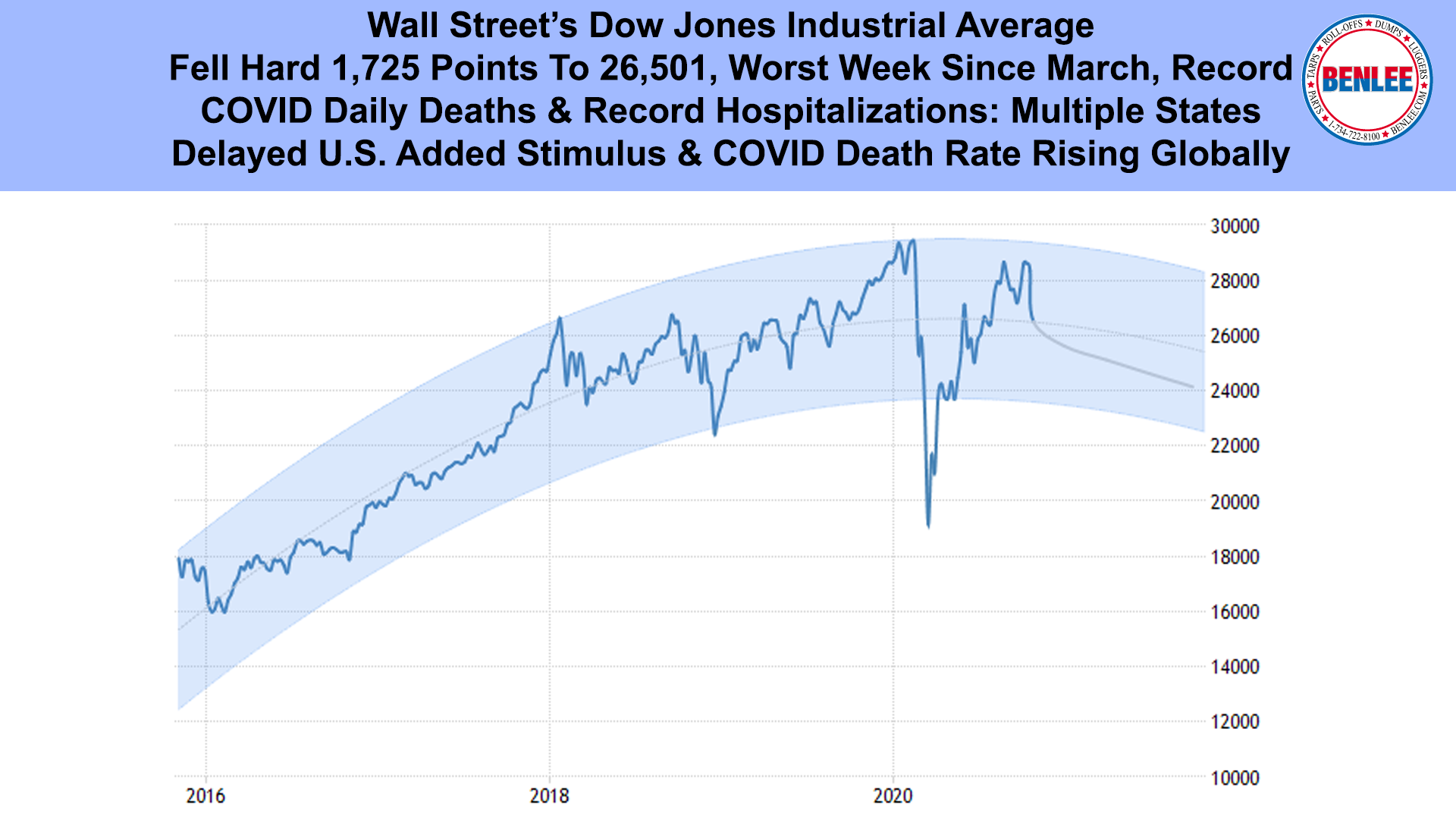

Wall Street’s Dow Jones Industrial Average fell a hard 1,725 points to 26,501 the worst week since March, on record COVID daily death rates and record hospitalizations in multiple states, as well as the delayed U.S. added stimulus and the COVID death rate rising globally.

Member

Member