Loading price data

This is the Global Economic, Commodities, Scrap Metal and Recycling Report, by our BENLEE Roll off Trailer and Gondola Trailer, March 8th, 2021.

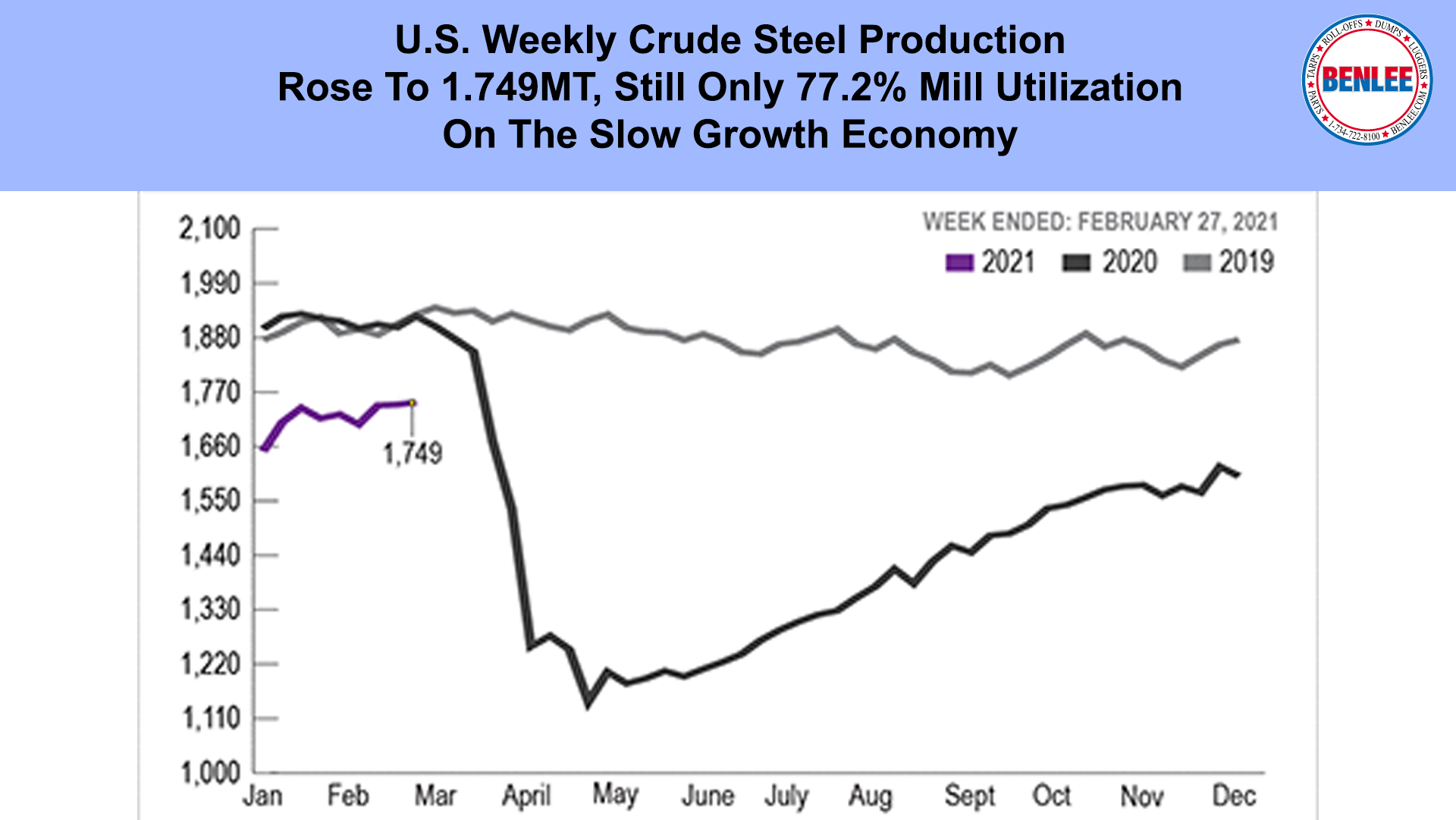

U.S. Weekly crude steel production rose to 1.749 MT, while still only 77.2% steel mill utilization, on the slow growth economy.

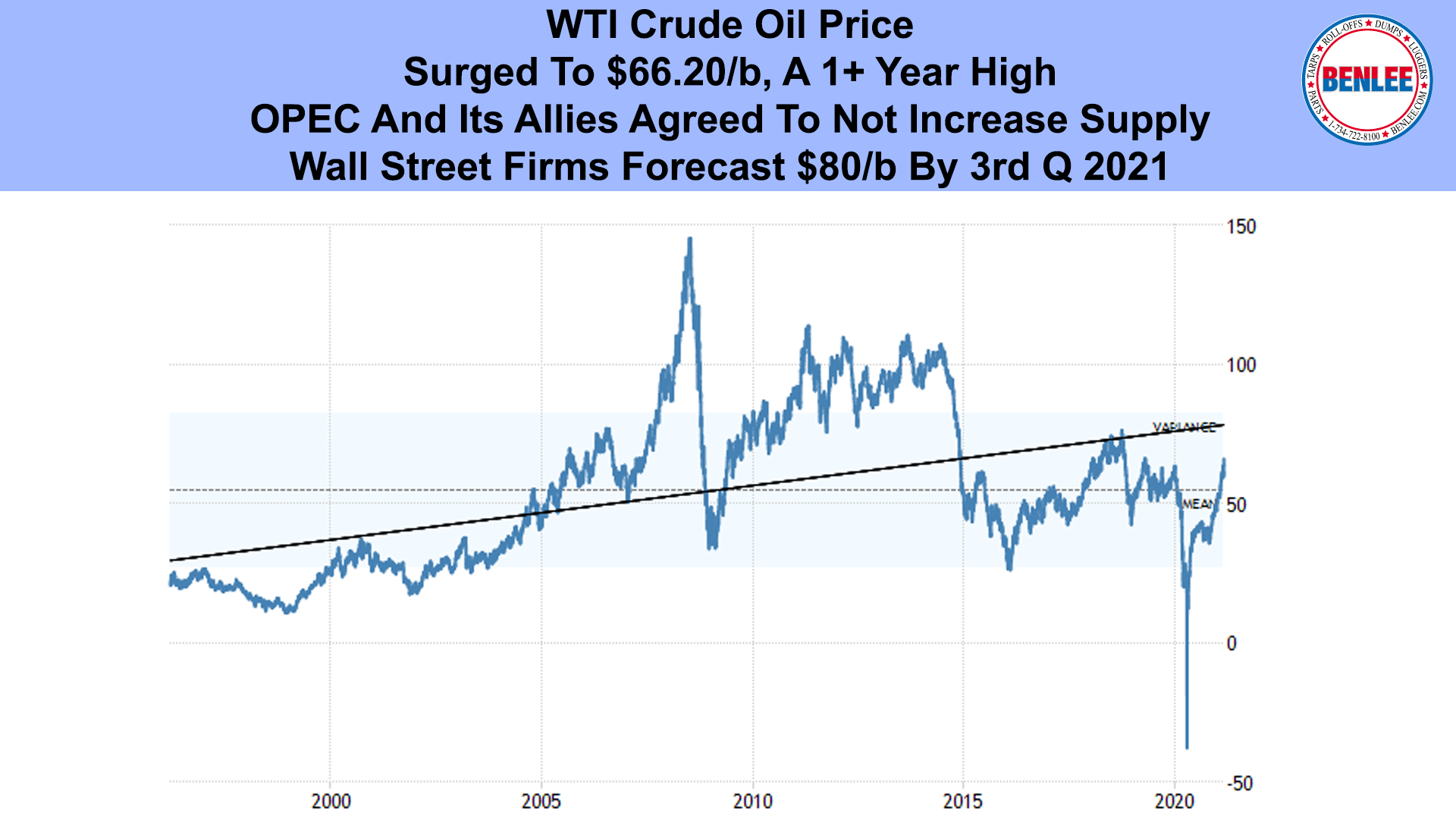

WTI Crude oil price surged to $66.20/b, a 1+ year high as OPEC and its allies agreed to not increase supply. Wall Street firms forecast $80/b by 3rd quarter 2021.

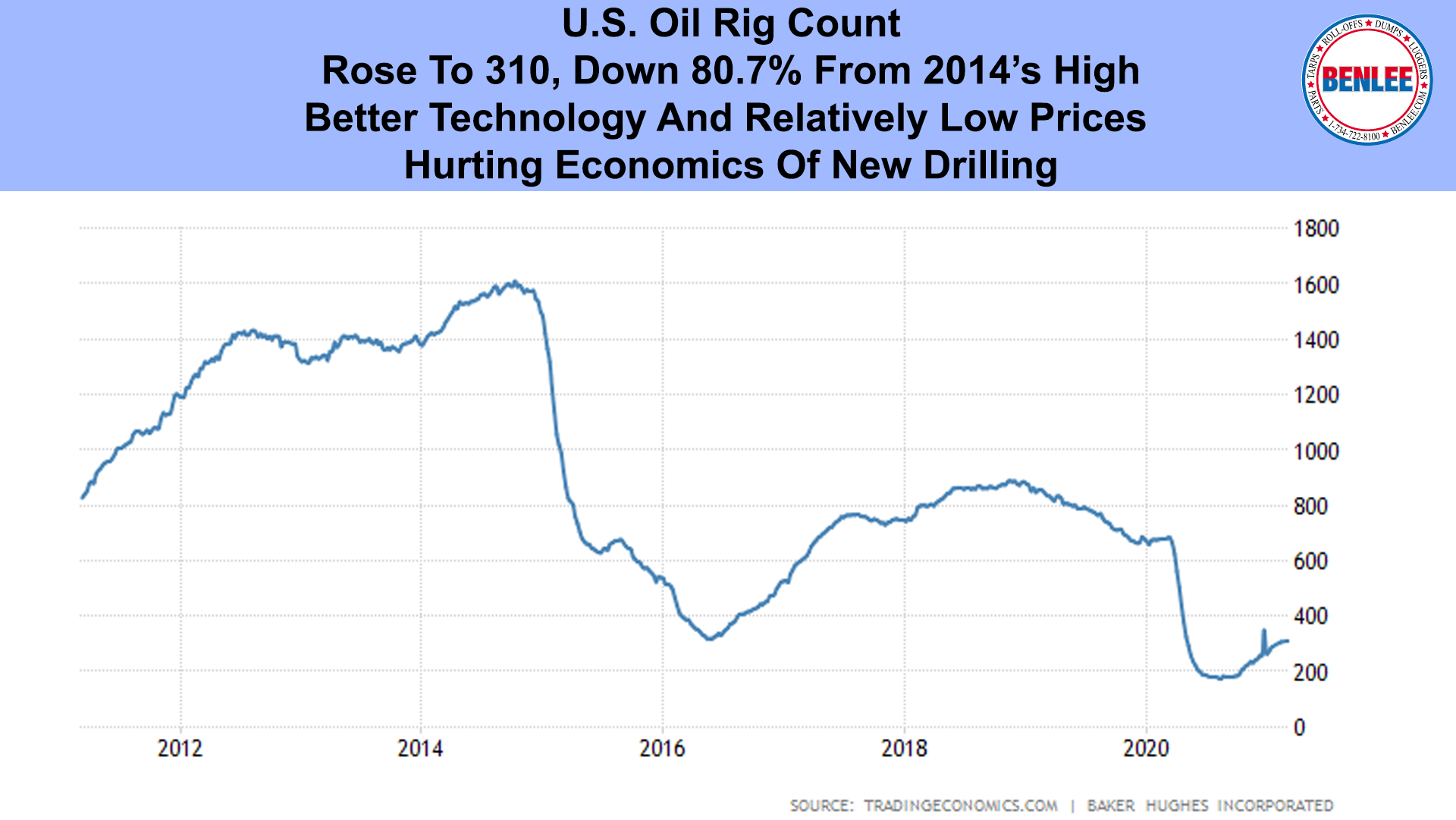

The U.S. Oil rig count rose to 310, down 80.7% from 2014’s high on better technology and low prices is hurting the economics of new drilling.

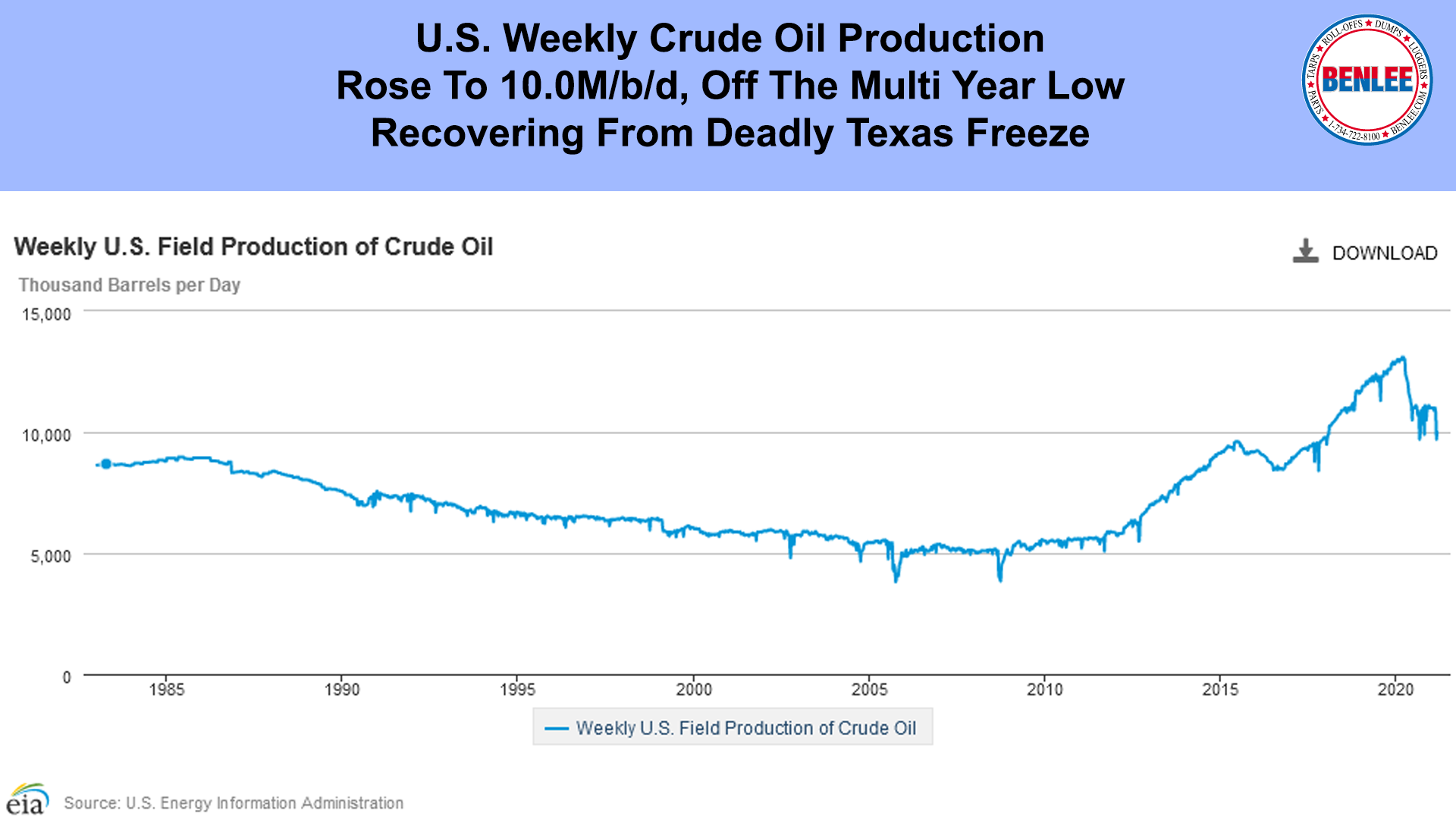

U.S. weekly crude oil production rose to 10.0M/b/d, off the multi-year low, recovering from the deadly Texas freeze.

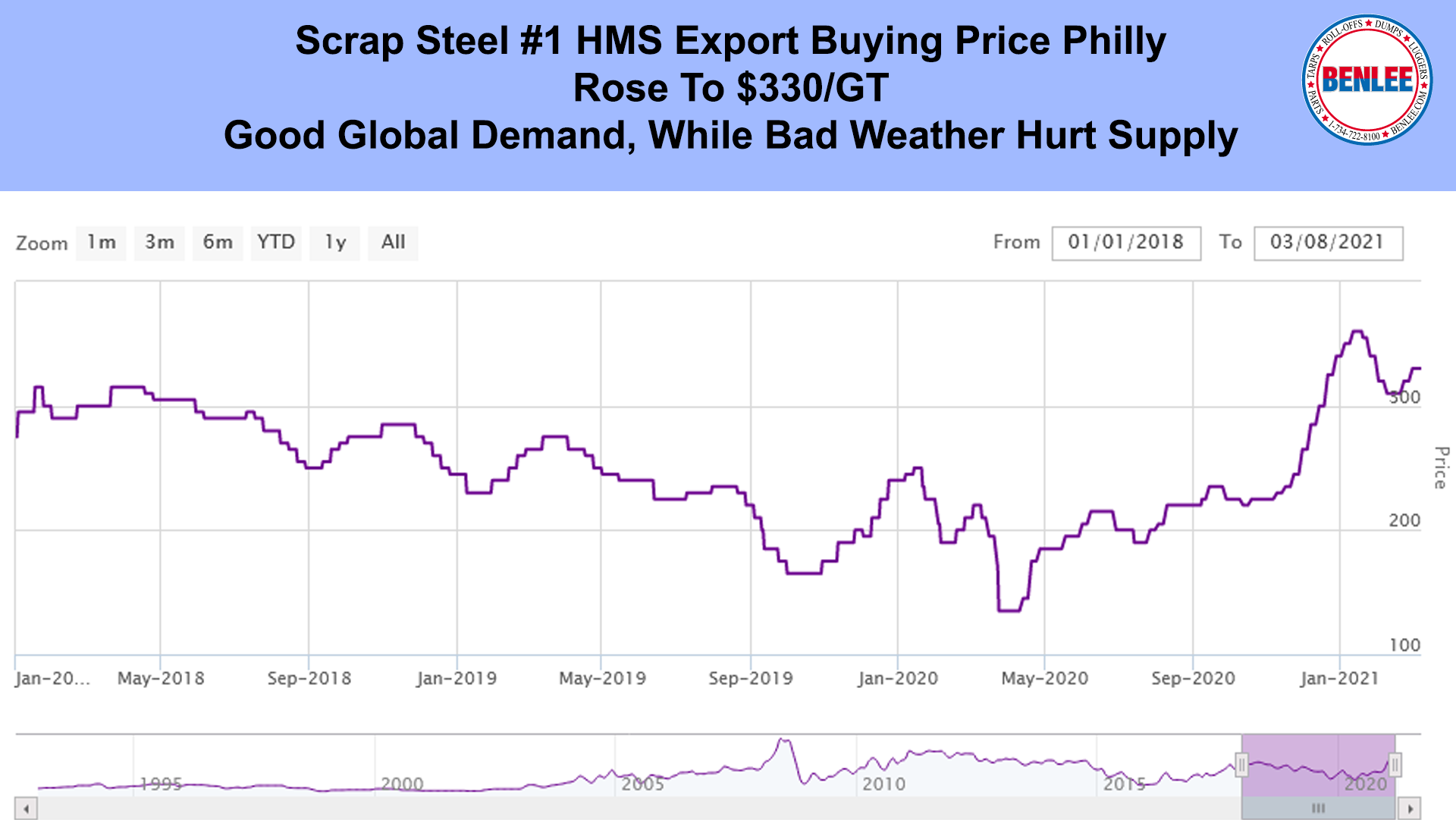

Scrap Steel #1 HMS export buying price Philly, rose to $330/GT on good global demand, while bad weather hurt supply.

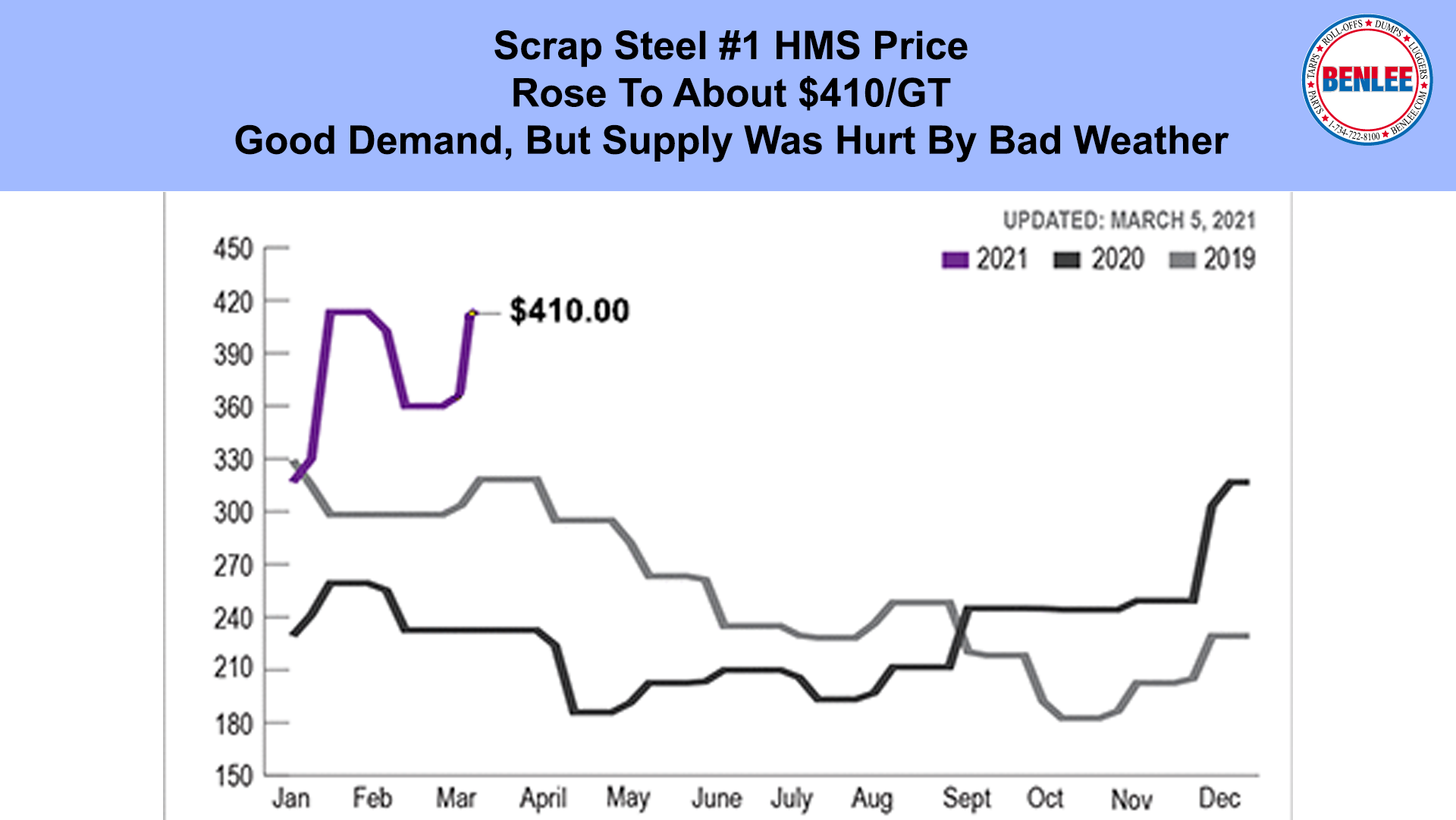

Scrap steel #1 HMS rose to about $410/GT on good demand, but again, supply was hurt by bad weather.

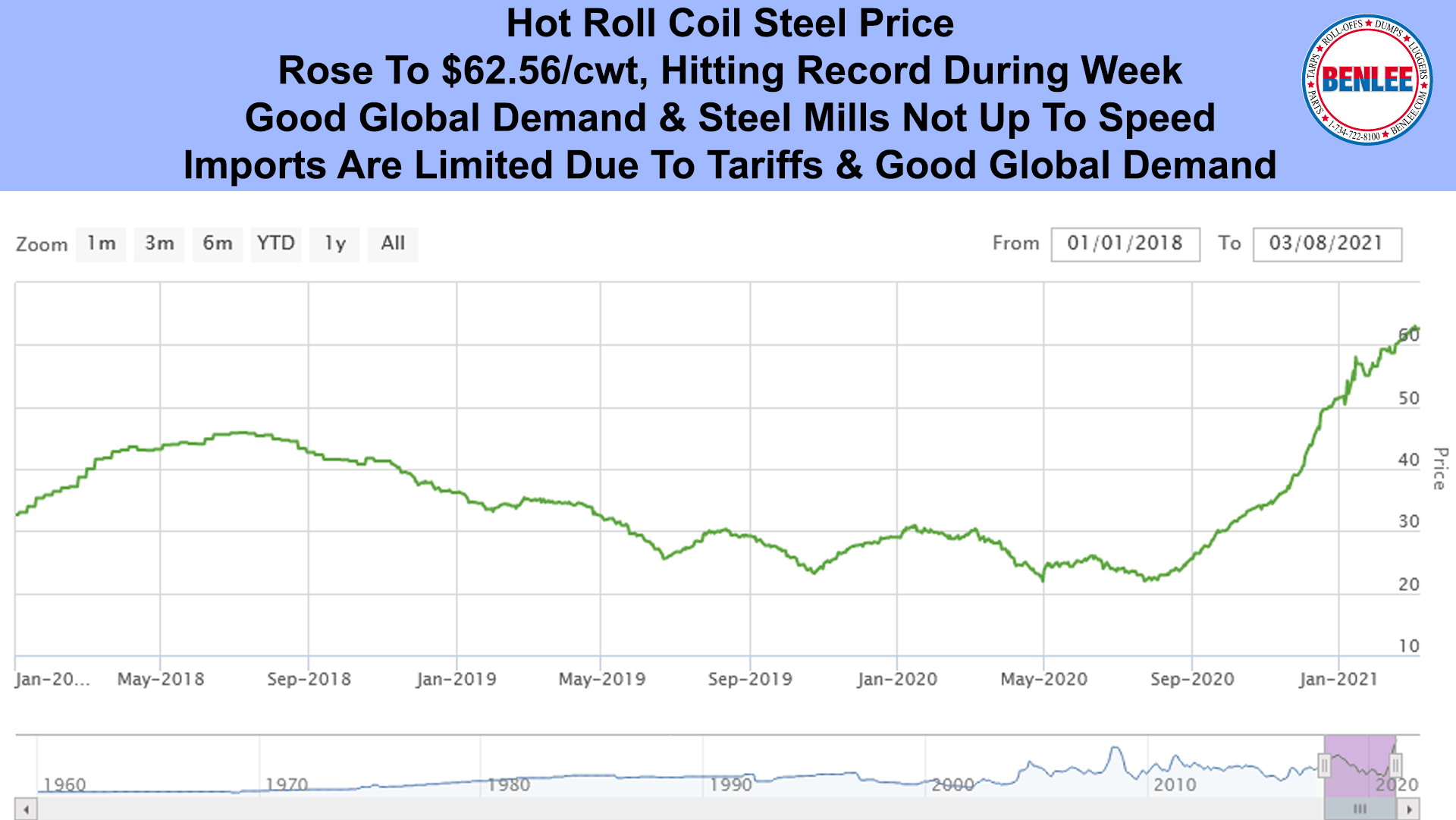

Hot roll coil steel rose to $62.56/cwt, hitting a record during the week, on good global demand and steel mills not up to speed. Imports are limited due to tariffs & good global demand.

Copper price was steady at $4.10/lb. Markets are nervous about too much government stimulus, which could lead to too fast growth, then could lead to higher interest rates, then to slower growth.

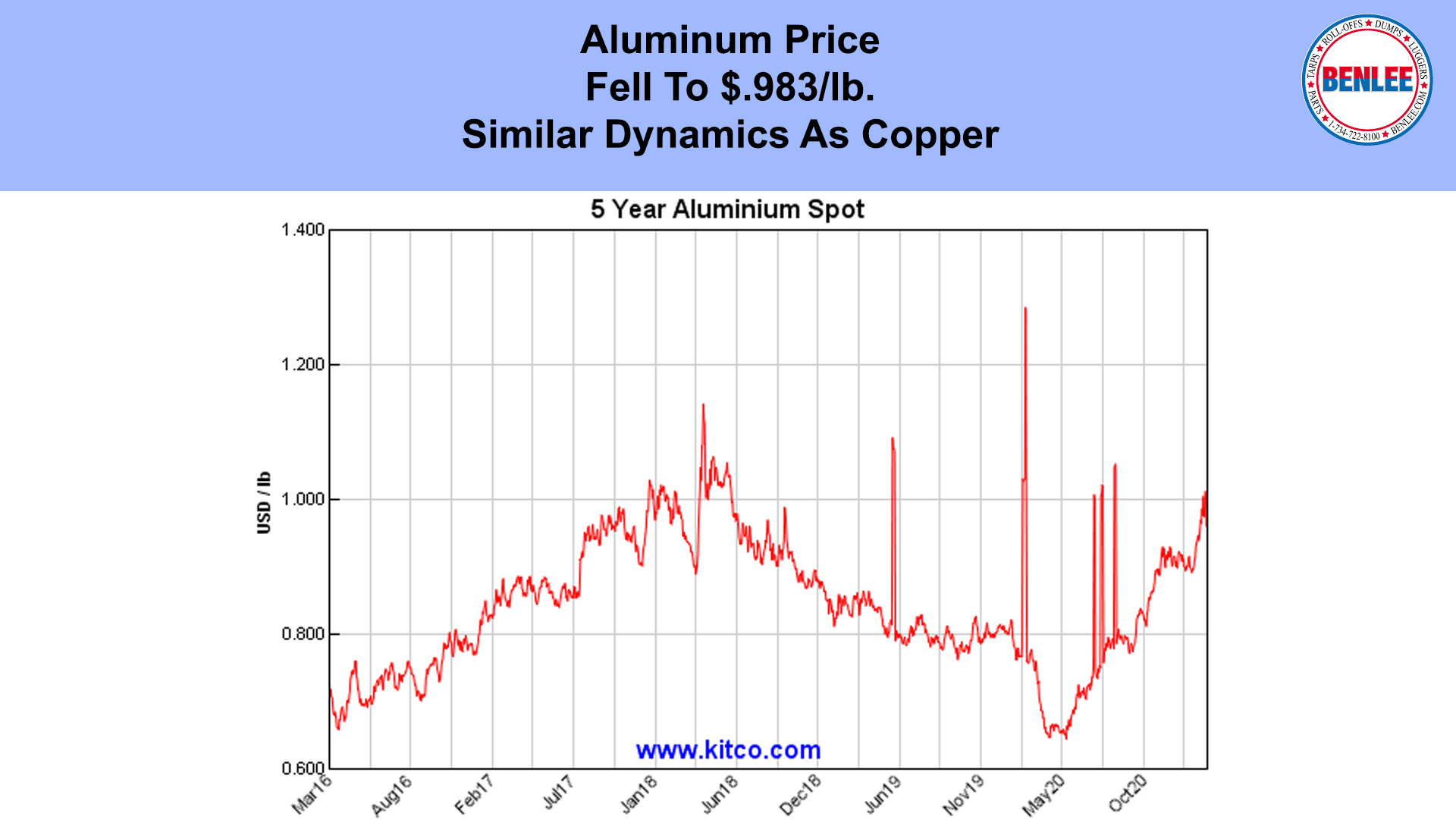

Aluminum price fell to 98.3 cents per pound, on similar dynamics as copper.

China Exports for January/February combined surged 60.6% over last year on soaring global demand. The U.S./China trade deficit DOUBLED, yes doubled to $51.26B, as Americans spent stimulus payments on Chinese made Electronics & Furniture.

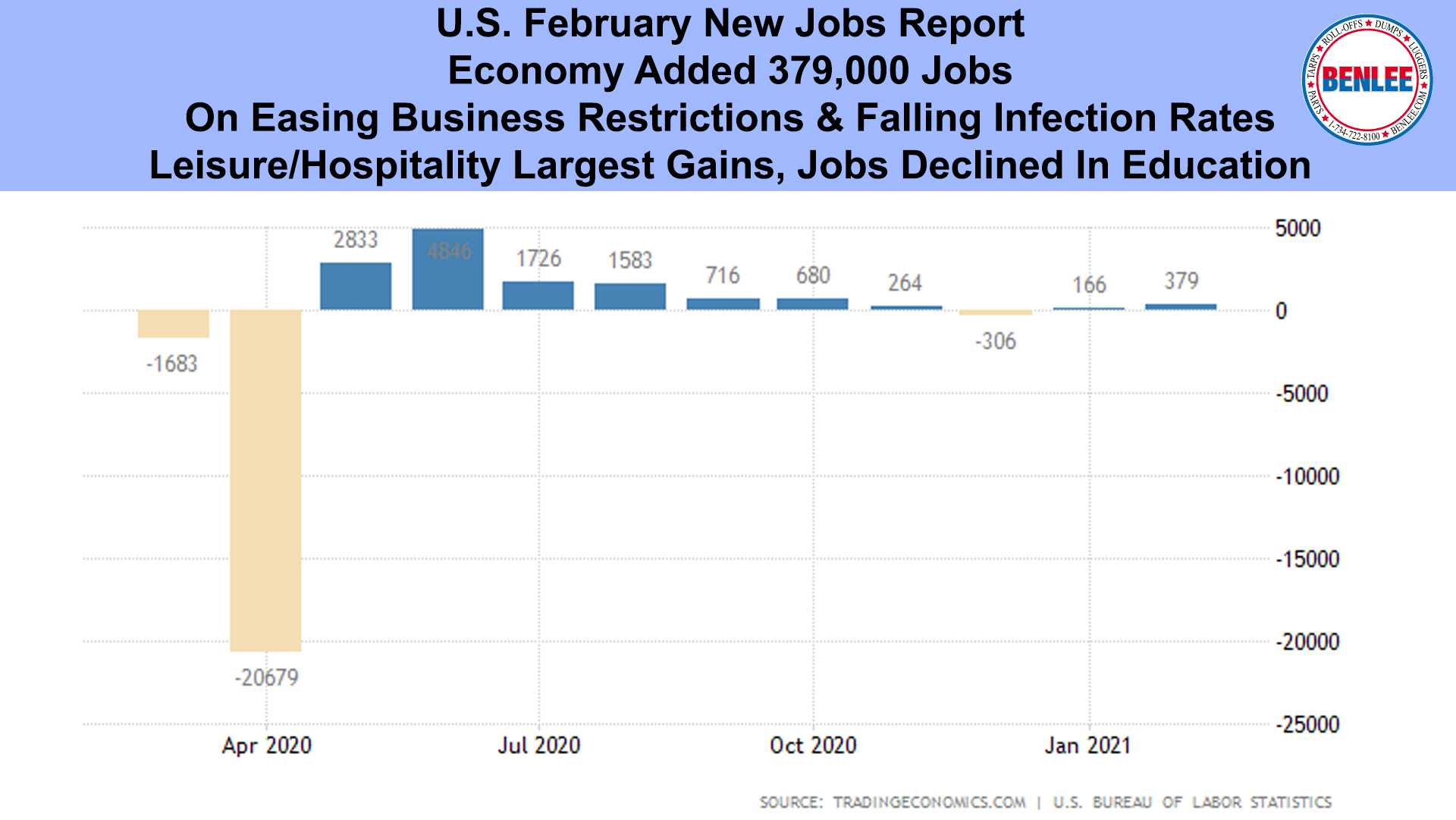

U.S. February new jobs report showed the economy added 379,000 jobs, on easing business restrictions and falling infection rates. Leisure and hospitality had the largest gains, while jobs declined in Education.

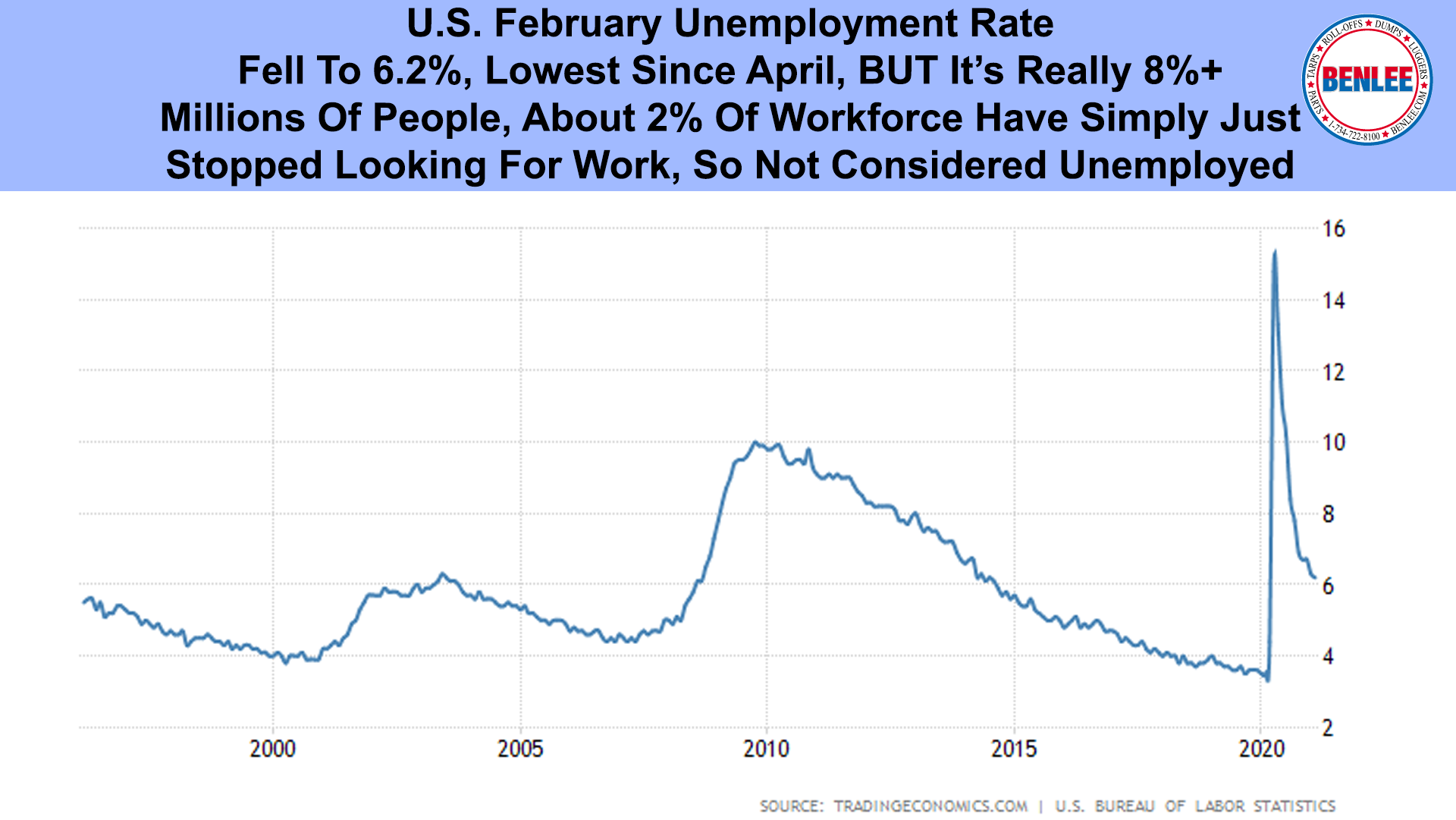

The U.S. February unemployment rate fell to 6.2%, the lowest since April, but it’s really about 8%+. Millions of people, about 2% of the workforce, have simply just stopped looking for work, so they are not considered unemployed.

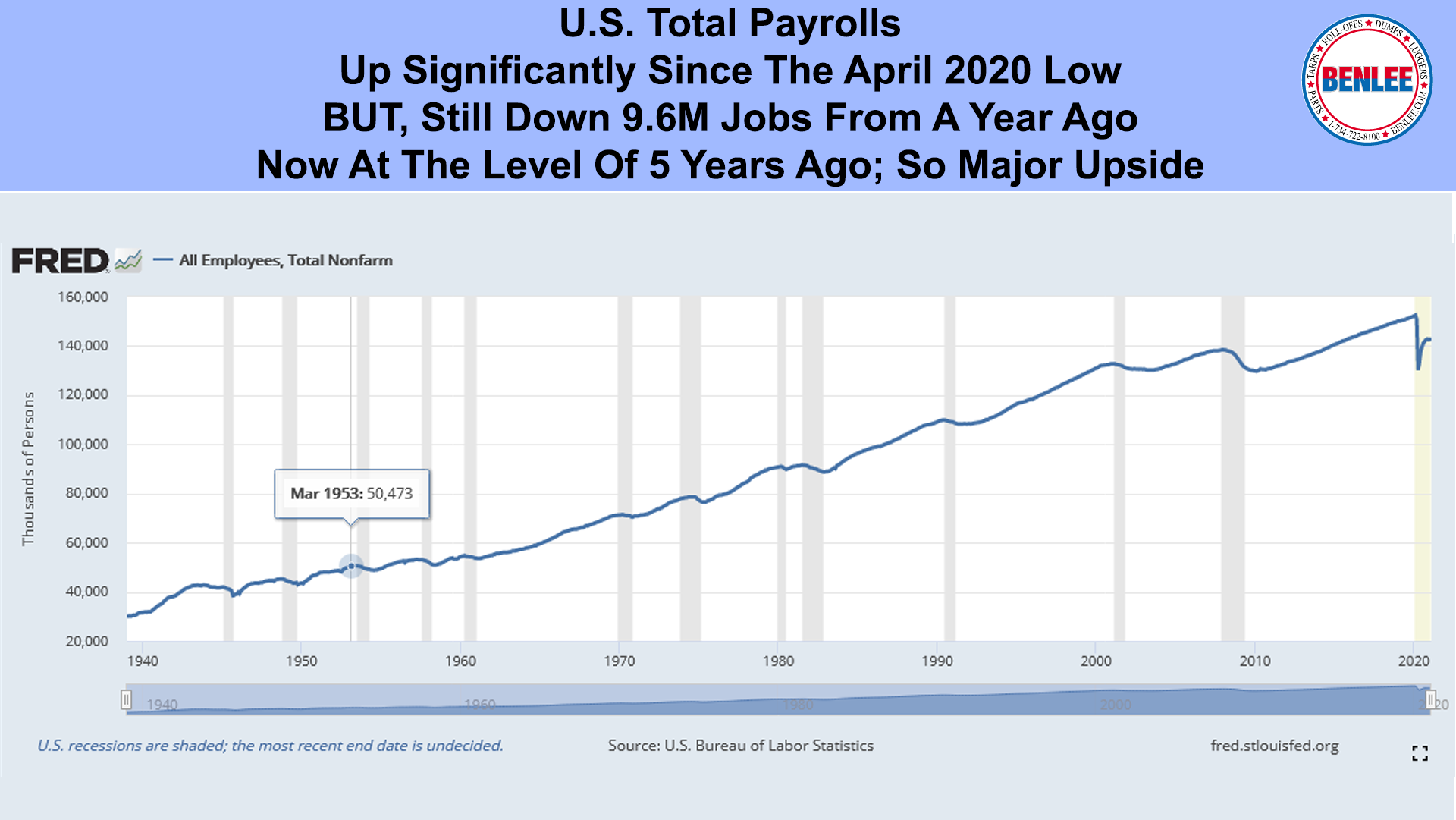

U.S. total payrolls are up significantly since the April 2020 low, but are still down 9.6M jobs from a year ago. We are now at the level of 5 years ago, so there is major upside.

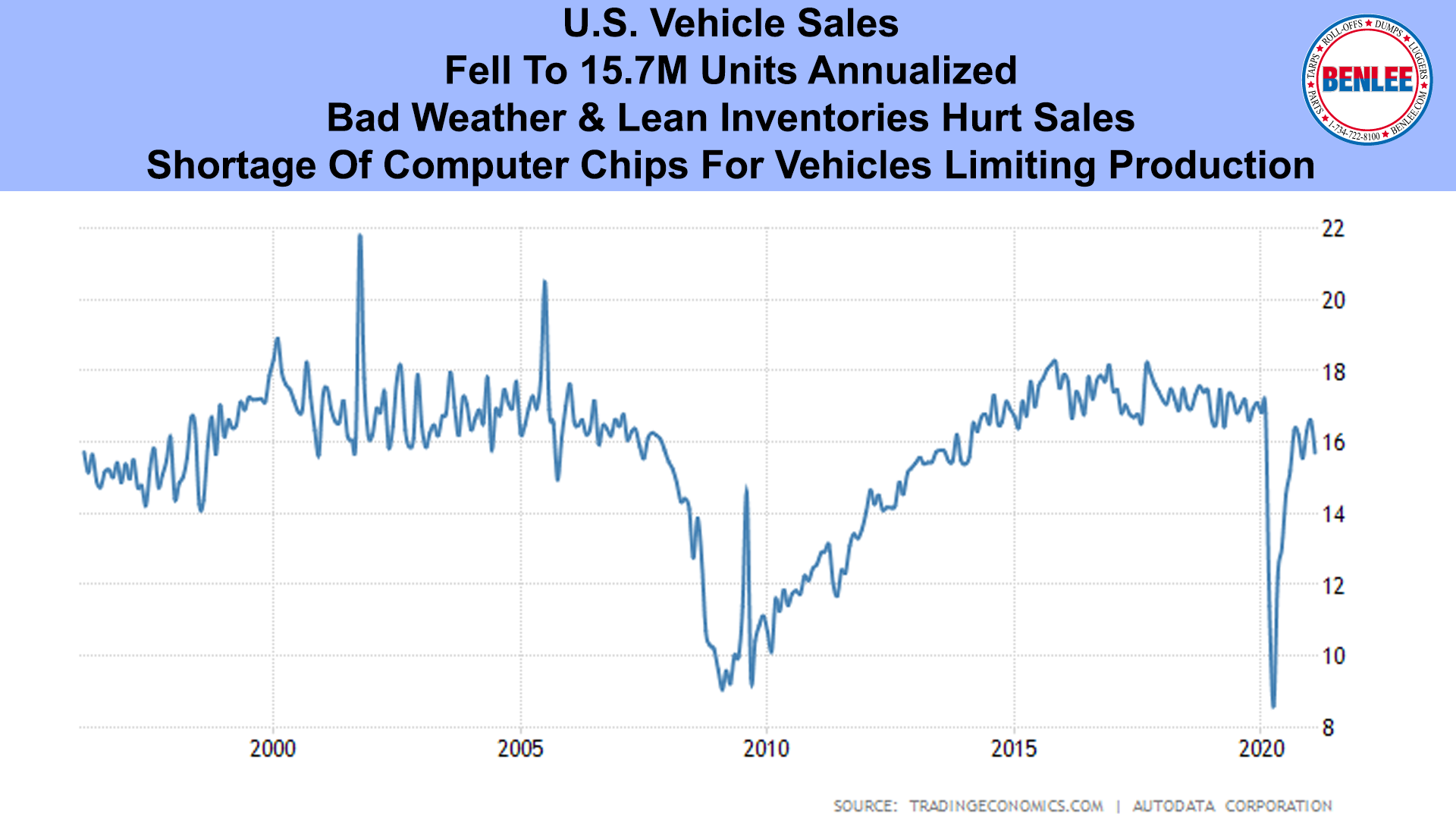

U.S. vehicle sales fell to 15.7M units annualized. Bad weather and lean inventories hurt sales. The shortage of computer chips for vehicles is limiting production.

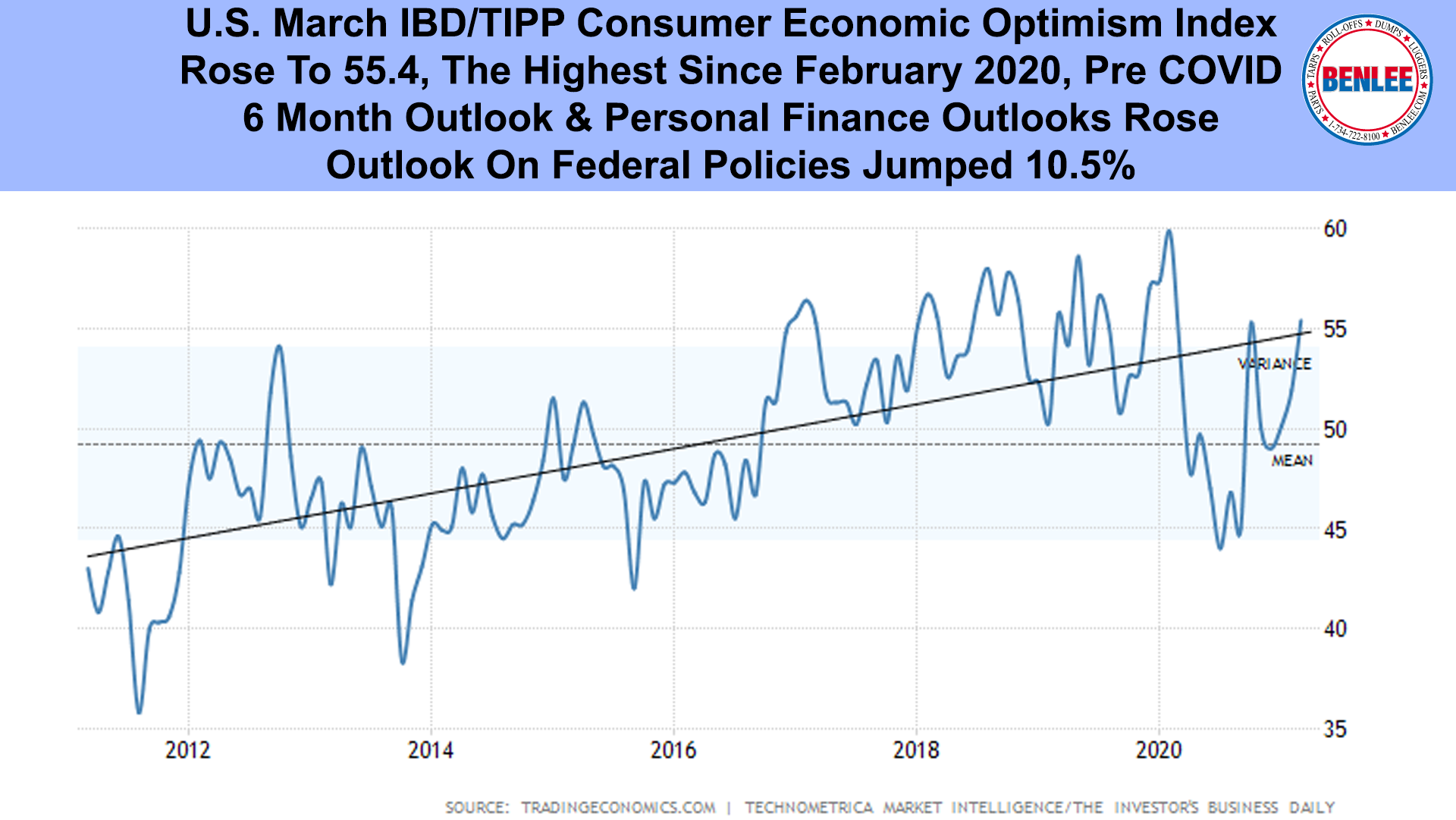

U.S. March IBD/TIPP consumer economic optimism index rose to 55.4 the highest since February 2020, pre COVID. The 6-month outlook and personal finance outlook rose. The outlook on Federal policies jumped 10.5%.

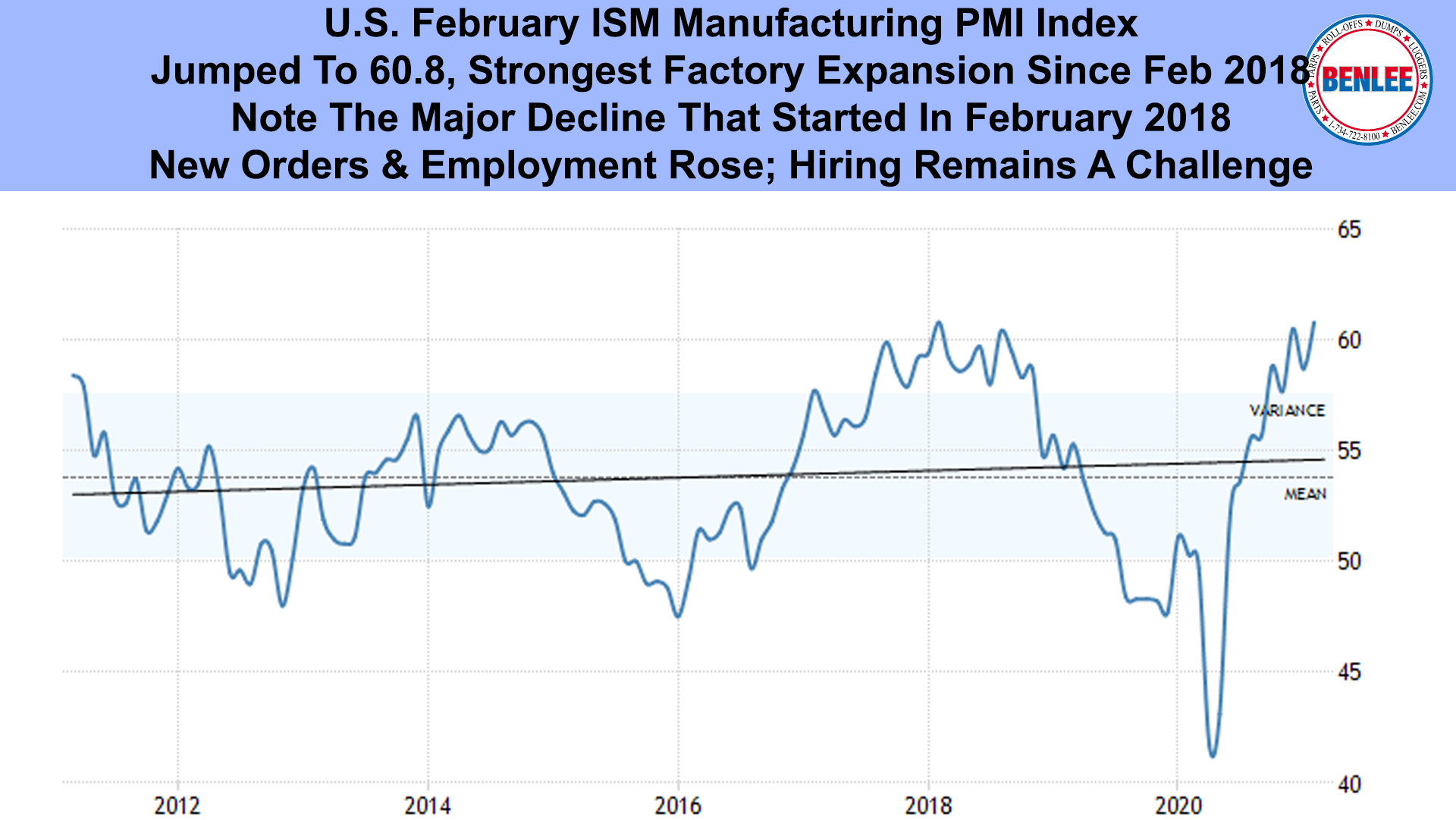

The U.S. February ISM manufacturing PMI index jumped to 60.8 with the strongest factory expansion since February 2018. Note the major decline that started in February 2018. New Orders & employment rose while hiring remains a challenge.

Wall Street’s Dow Jones Industrial average rose 564 points to 31,496, on the better-than-expected jobs report. But higher interest rates remain a concern as the massive new government stimulus could make growth too fast.

Member

Member