Loading price data

This is the Global Economic, Commodities, Scrap Metal and Recycling Report, by our BENLEE Roll off Trailer and Gondola Trailer, March 29th, 2021.

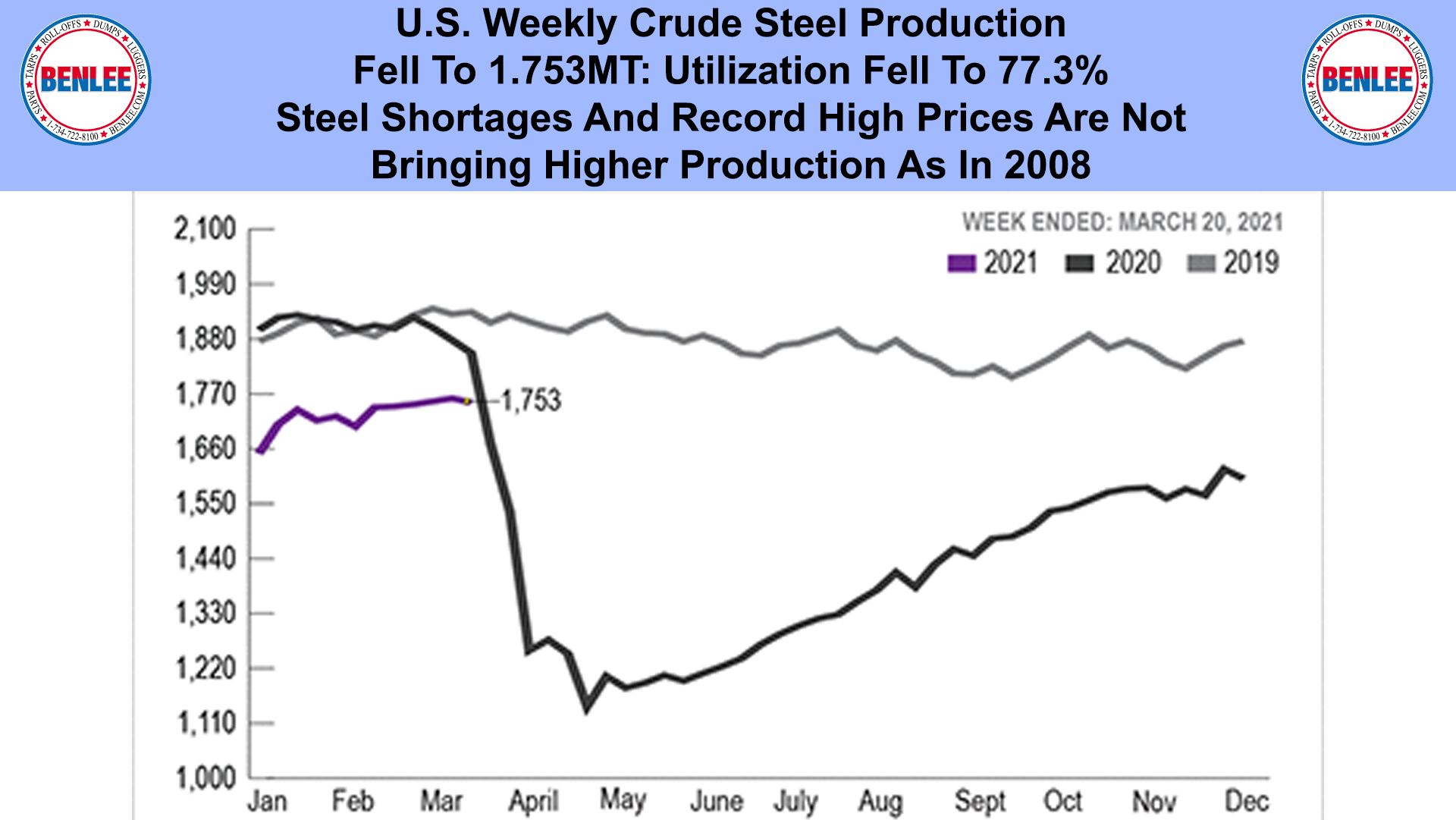

U.S. Weekly crude steel production fell to 1.753MT. Utilization fell to 77.3%. Steel shortages and record high prices are not bringing higher production as in 2008.

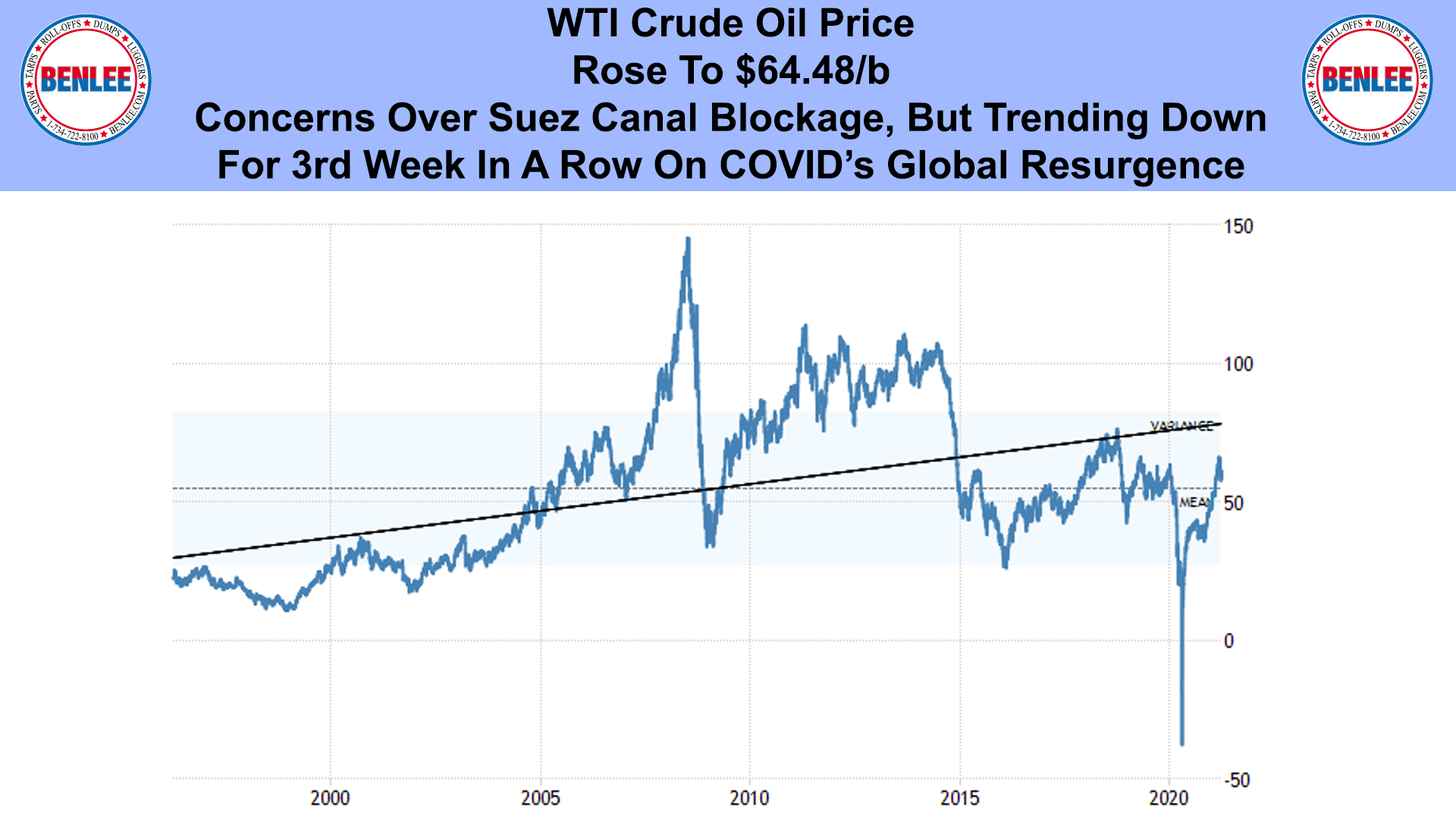

WTI Crude oil price rose to $64.48/b on concerns over the Suez Canal blockage, but trending down for a 3rd week in a row on COVID’s global resurgence.

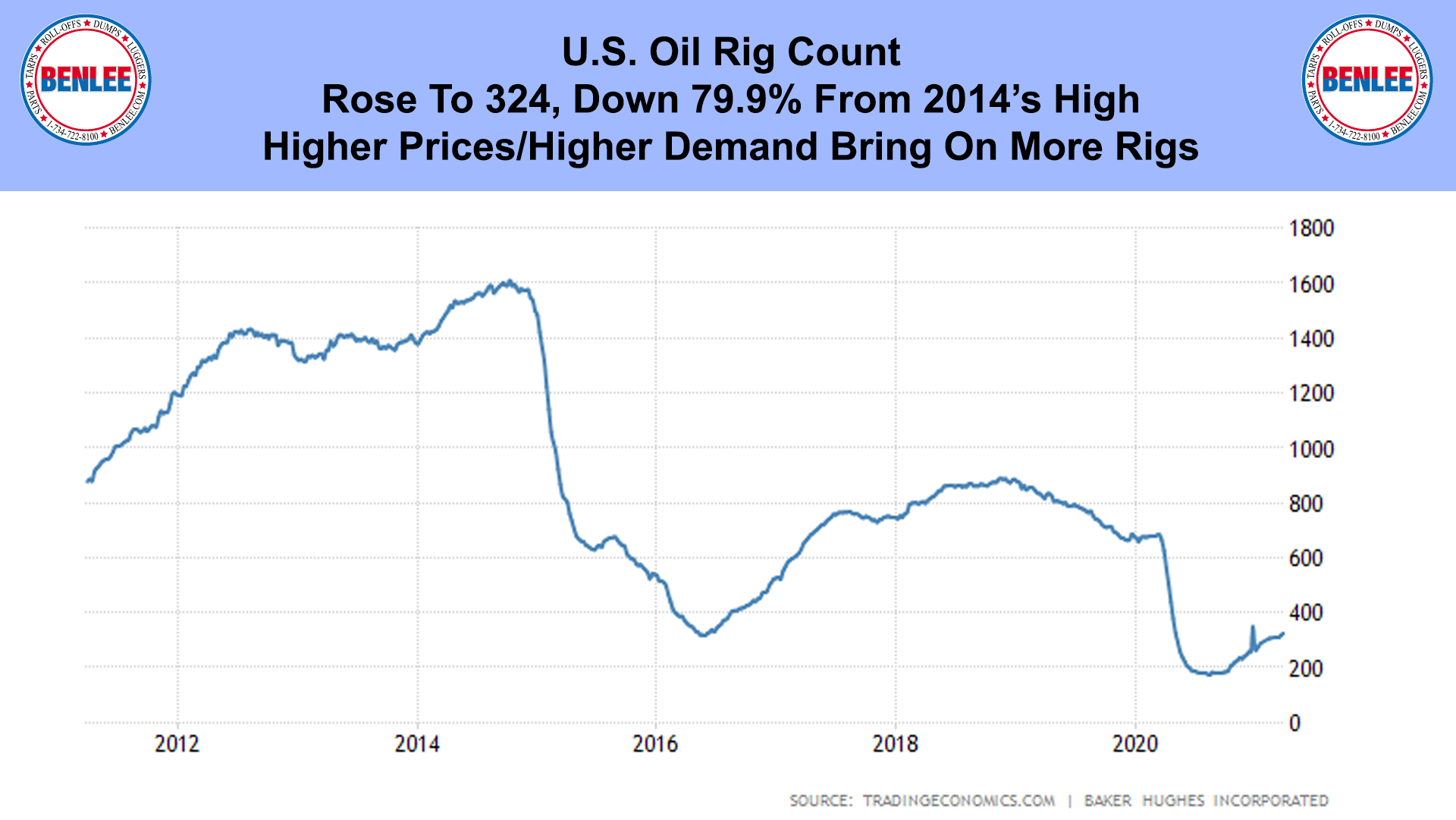

The U.S. Oil rig count rose to 324 down 79.9% from 2014’s high as higher prices and higher demand bring on more rigs.

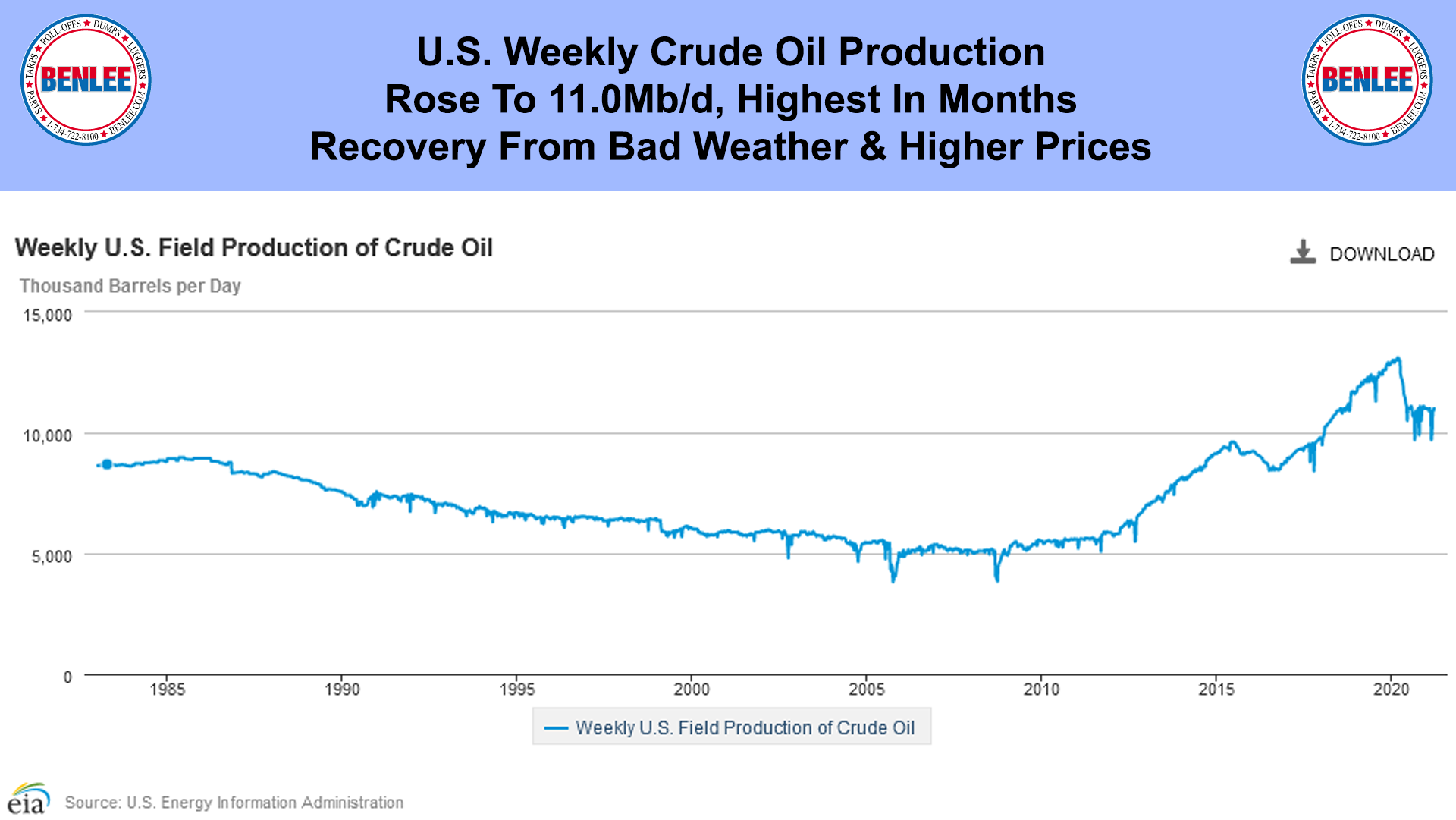

U.S. weekly crude oil production rose to 11.0Mb/d, the highest in months on the recovery from bad weather and higher prices.

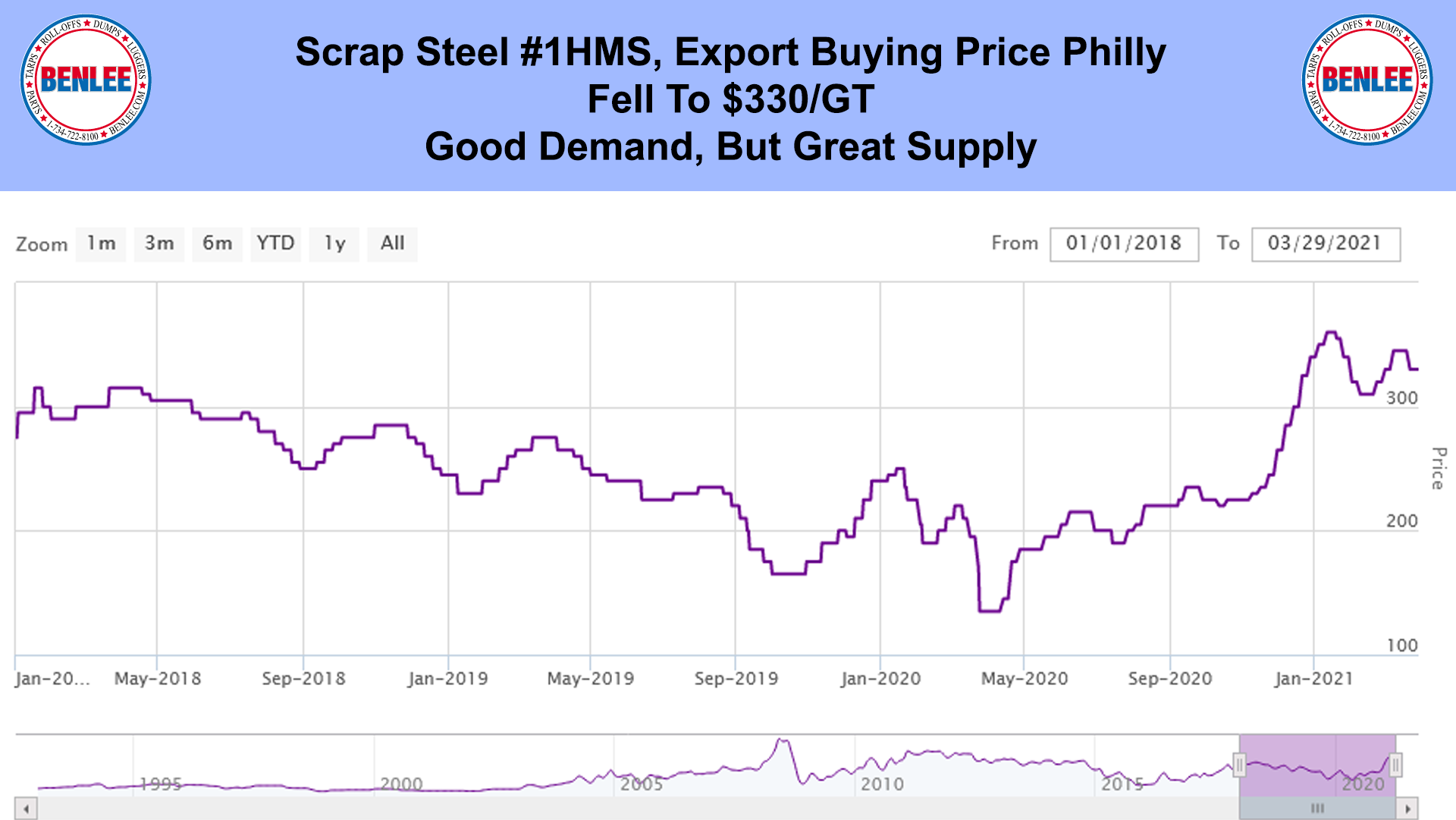

Scrap Steel #1 HMS export buying price Philly, fell to $330/GT on good demand, but great supply.

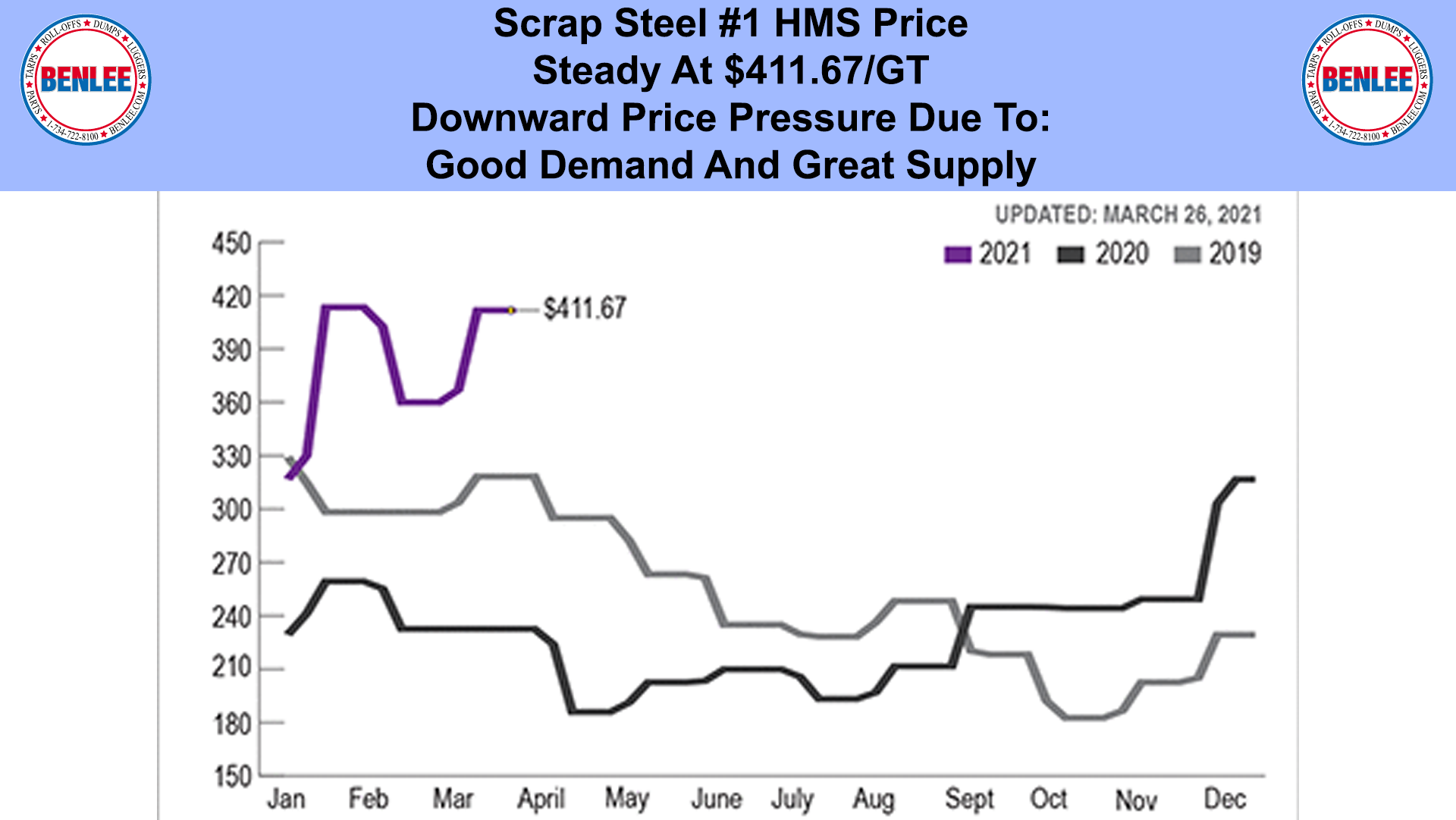

Scrap steel #1 HMS was steady at $411.67/GT, with downward price pressure due to good demand and great supply.

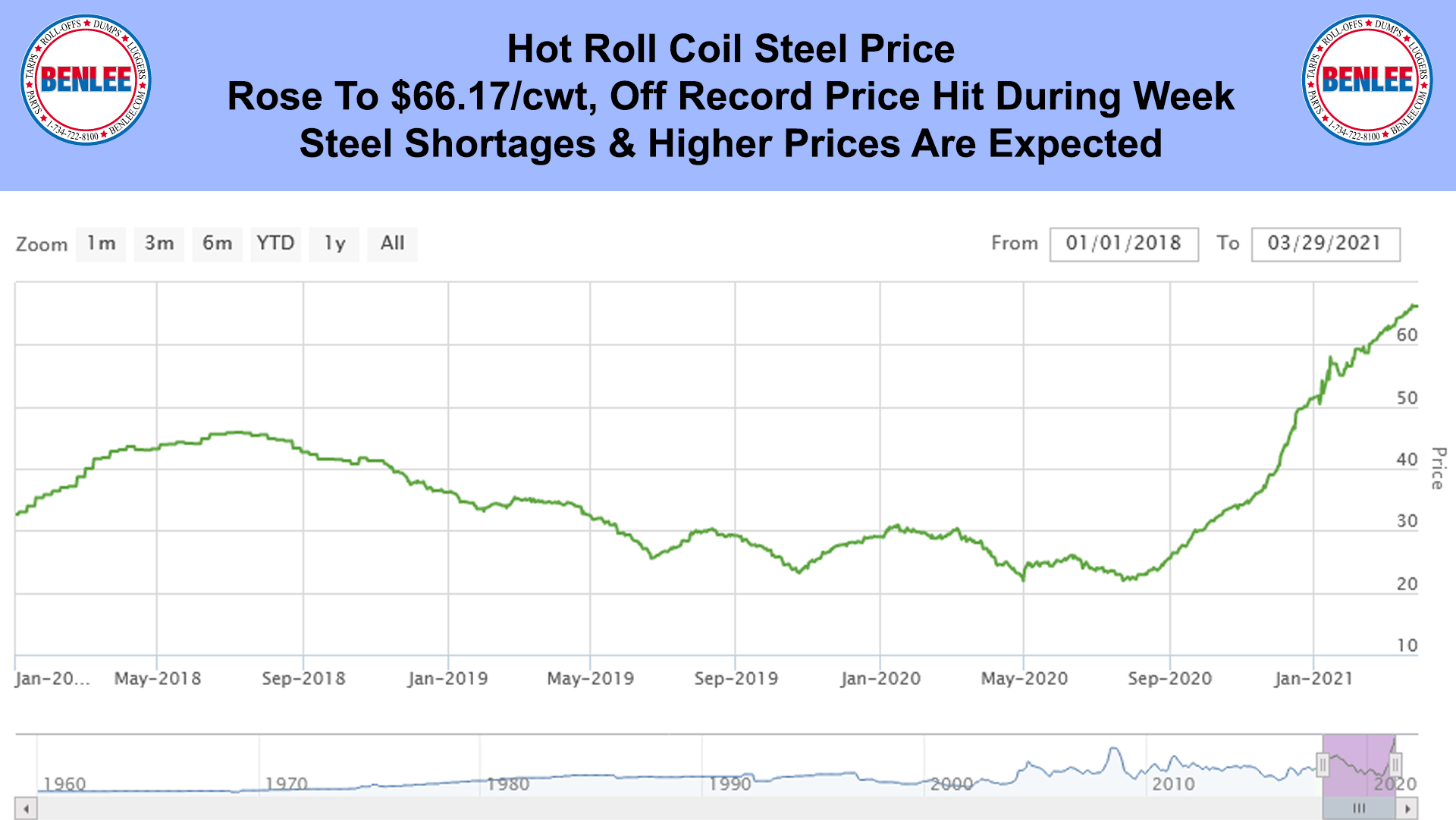

Hot roll coil steel rose to $66.17/cwt, off the record price hit during the week on steel shortages. Higher prices are expected.

Copper price fell to $4.08/lb. remaining high. It was lower on U.S./China political concerns, but high on China’s major growth.

Aluminum price rose to $1.02/lb., a multiyear high on supply concerns and as China considers release of government stockpiles to lower prices.

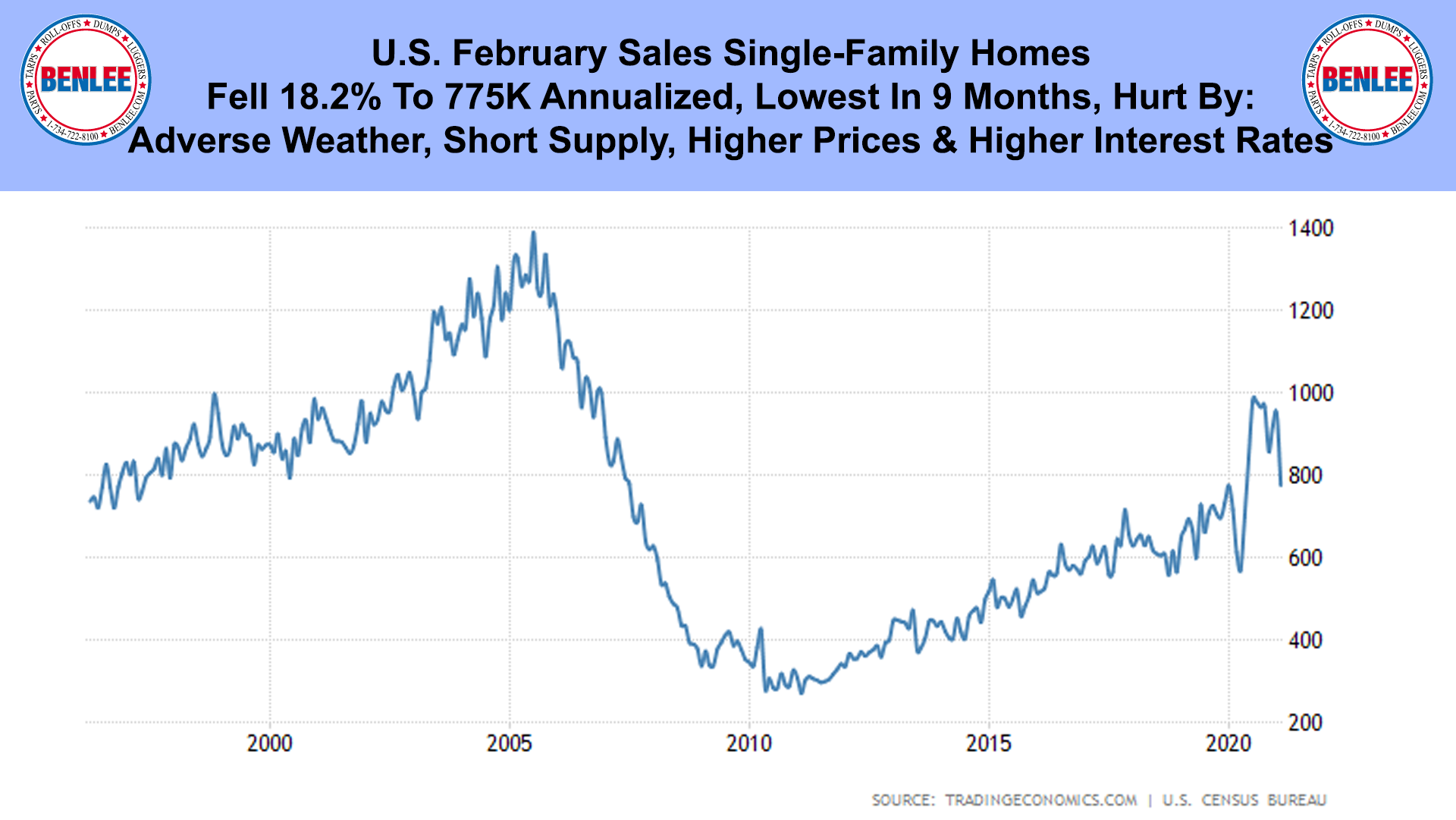

U.S. February Sales of single-family homes fell 18.2% to 775k annualized the lowest in 9 months. They were hurt by adverse weather, short supply, higher prices and higher interest rates.

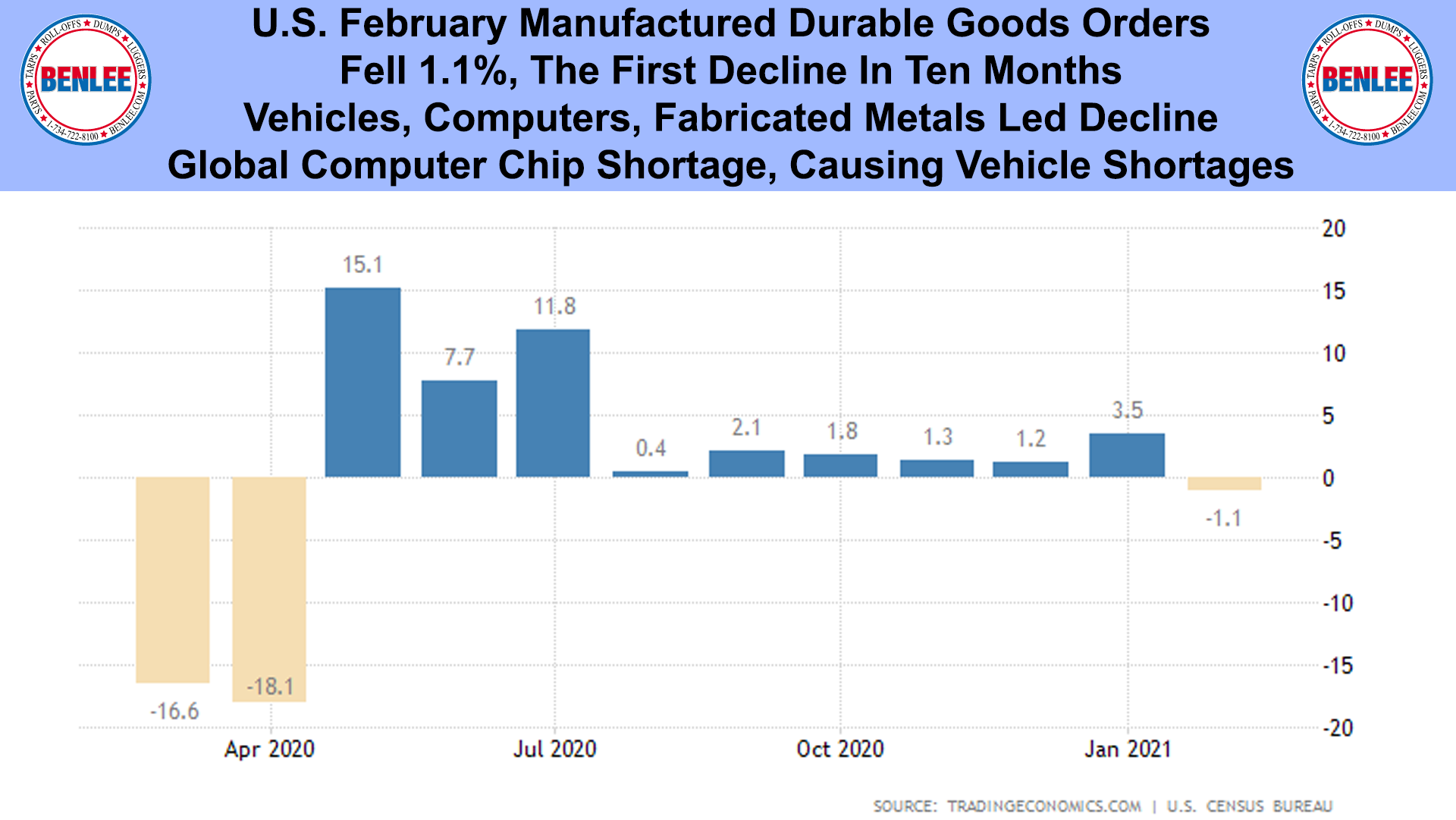

U.S. February manufactured durable goods orders fell 1.1%, the first decline in 10 months as vehicles, computers, fabricated metals led the decline. The global computer chip shortage in causing vehicle shortages.

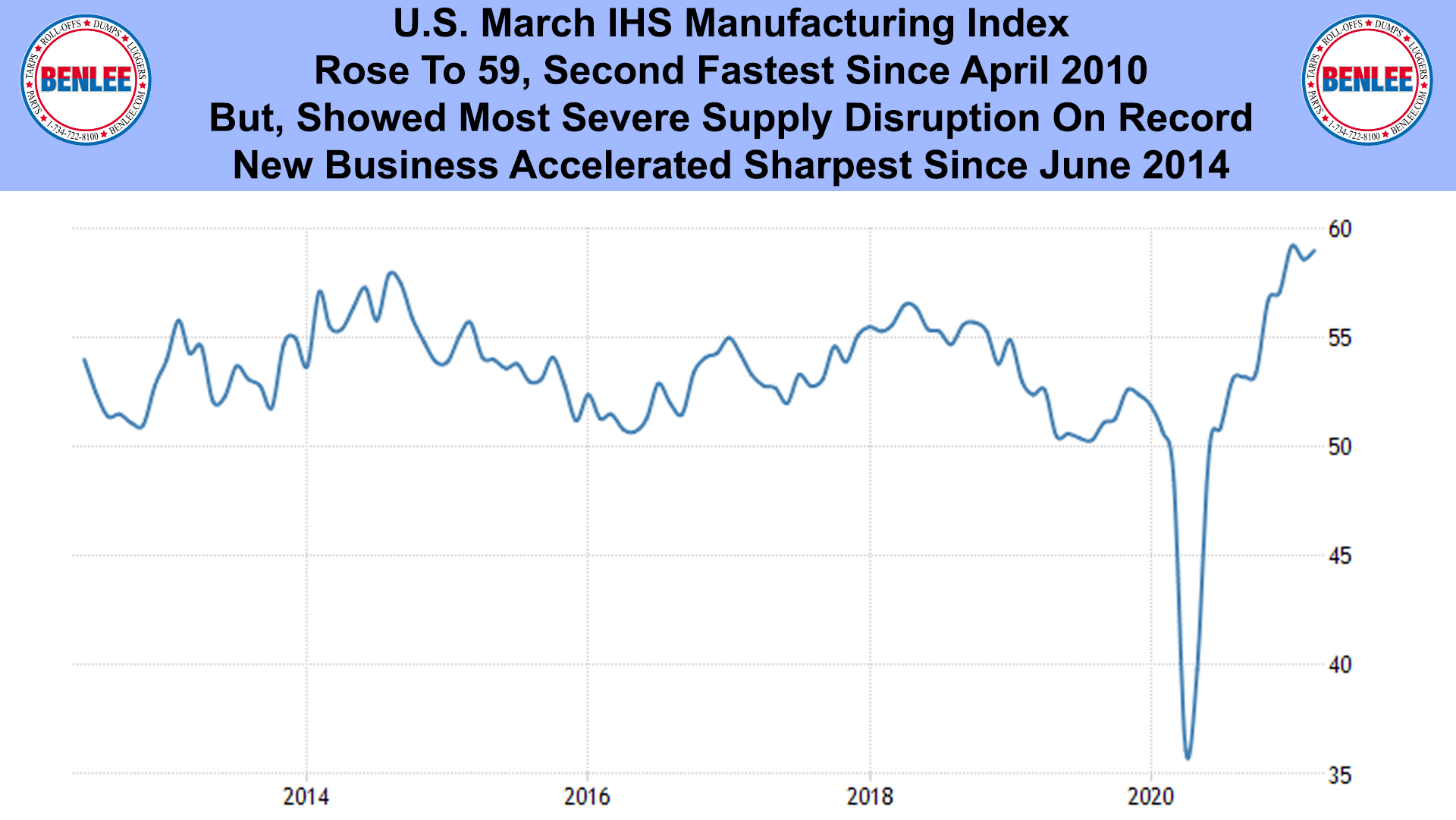

U.S. March IHS Manufacturing index rose to 59, the second fastest since April 2010, but showed the most severe disruptions on record. New business accelerated the sharpest since June 2014.

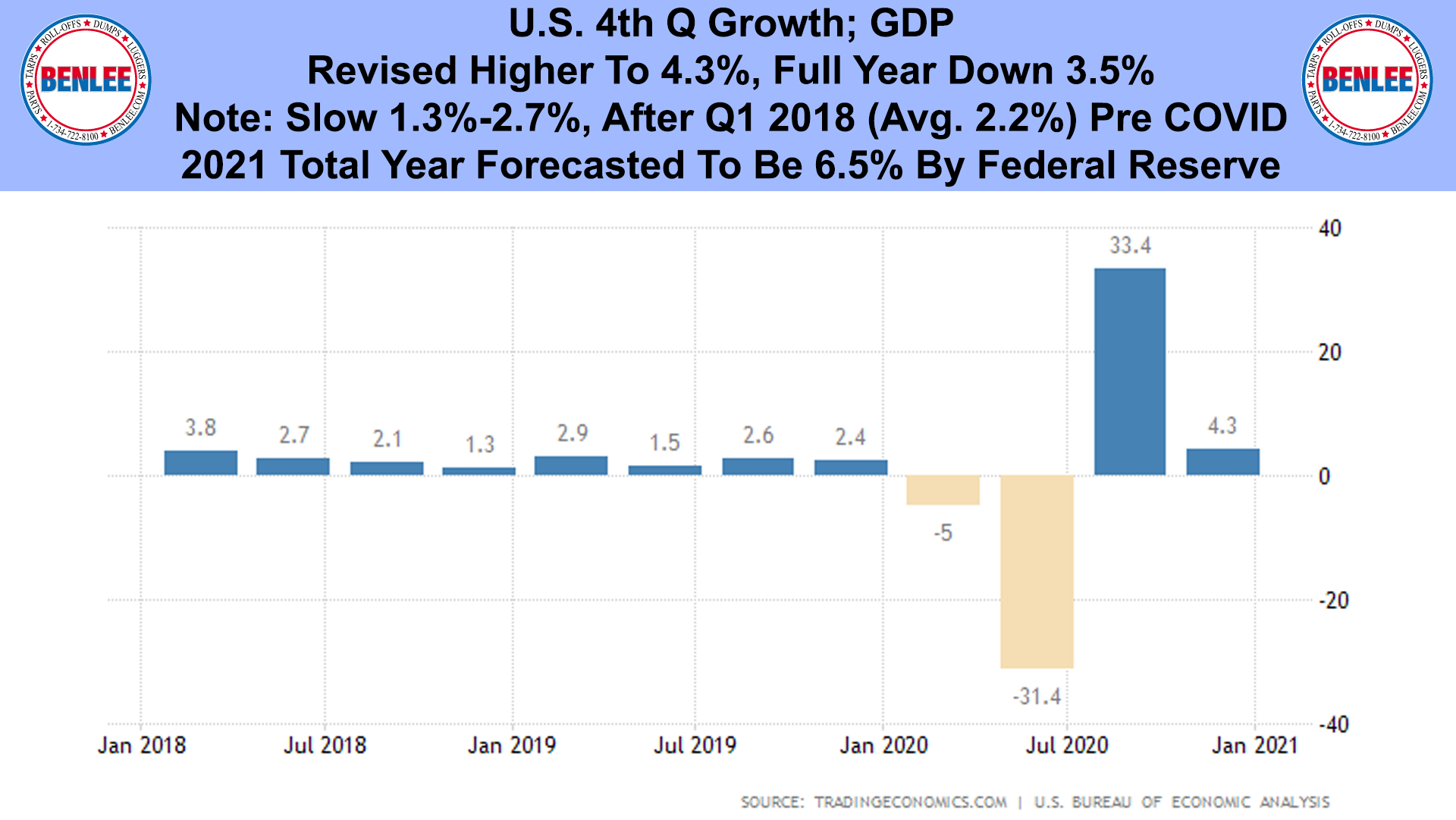

U.S. 4th Q Growth, GDP, was revised higher to 4.3%, with the full year down 3.5%. Note the slow 1.3-2.7% growth after Q1 2018 (average of 2.2%) pre COVID. 2021 total year is forecasted to be 6.5%, by the Federal Reserve.

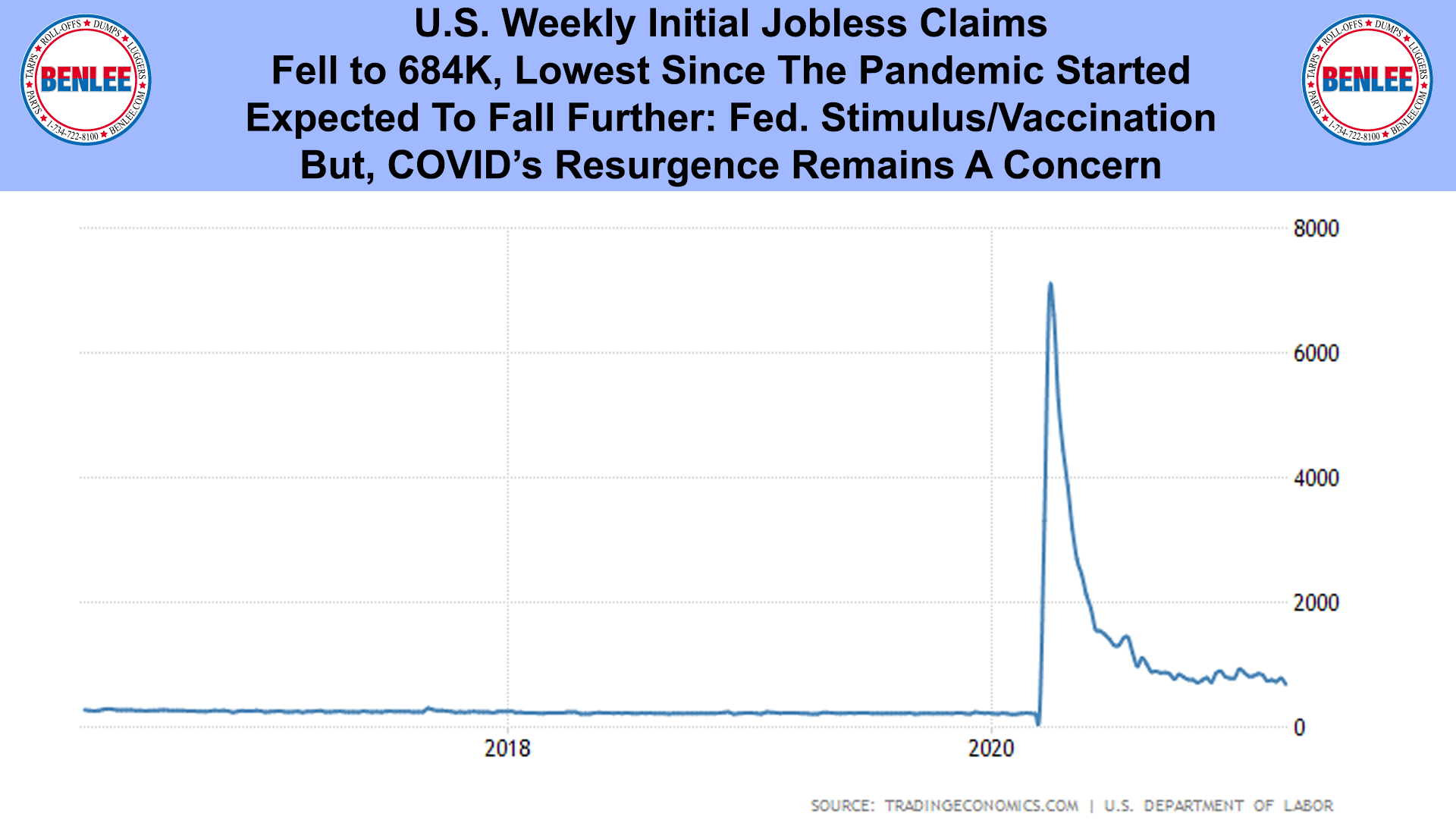

U.S. Weekly initial jobless claims fell to 684K, the lowest since the pandemic started. Claims are expected to fall further on Federal Stimulus and vaccinations, but COVID’s resurgence remains a concern.

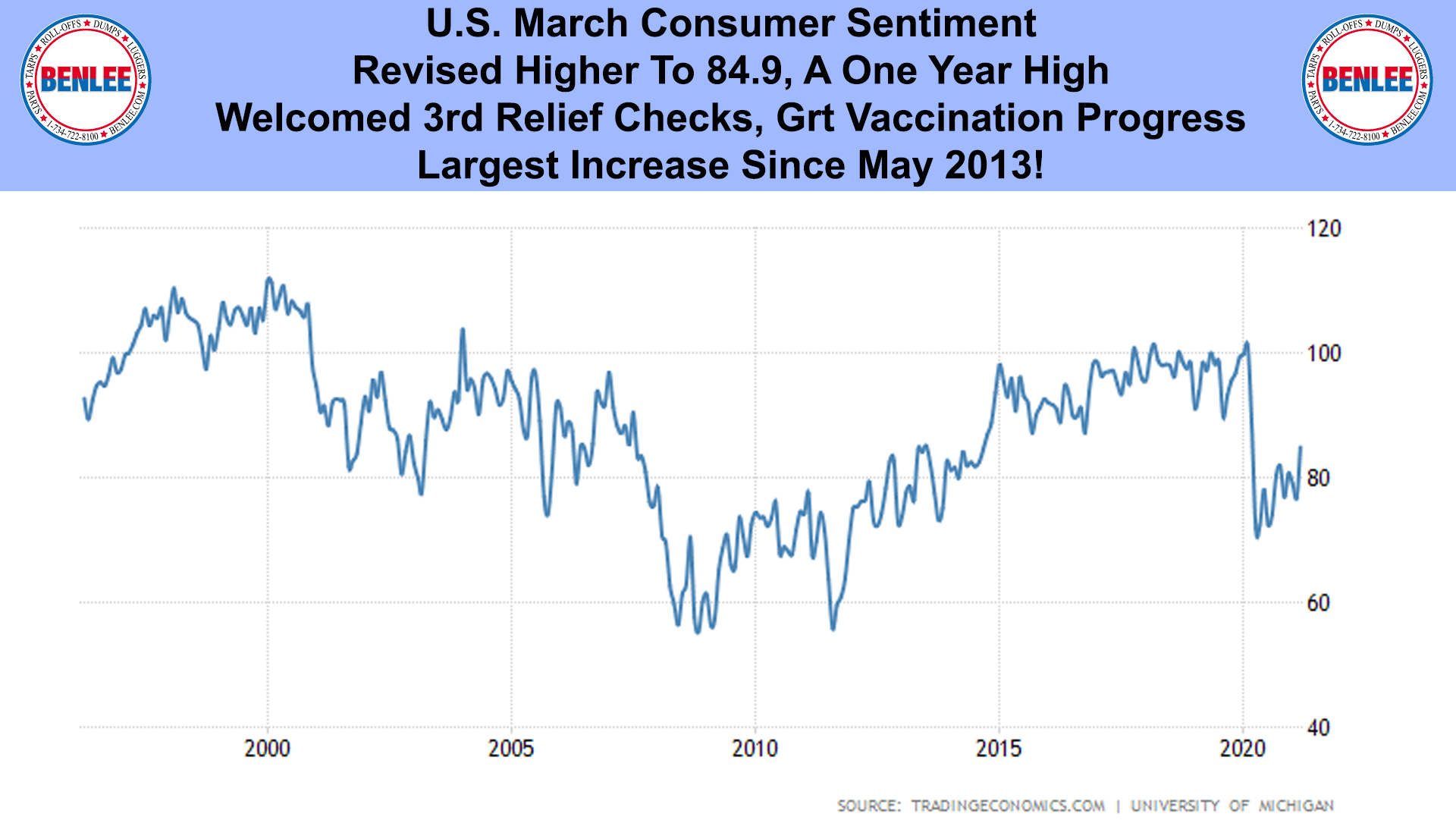

U.S. March Consumer Sentiment was revised higher to 84.9 a one year high. People welcomed the 3rd relief checks and great vaccination progress. This the largest increase since May 2013.

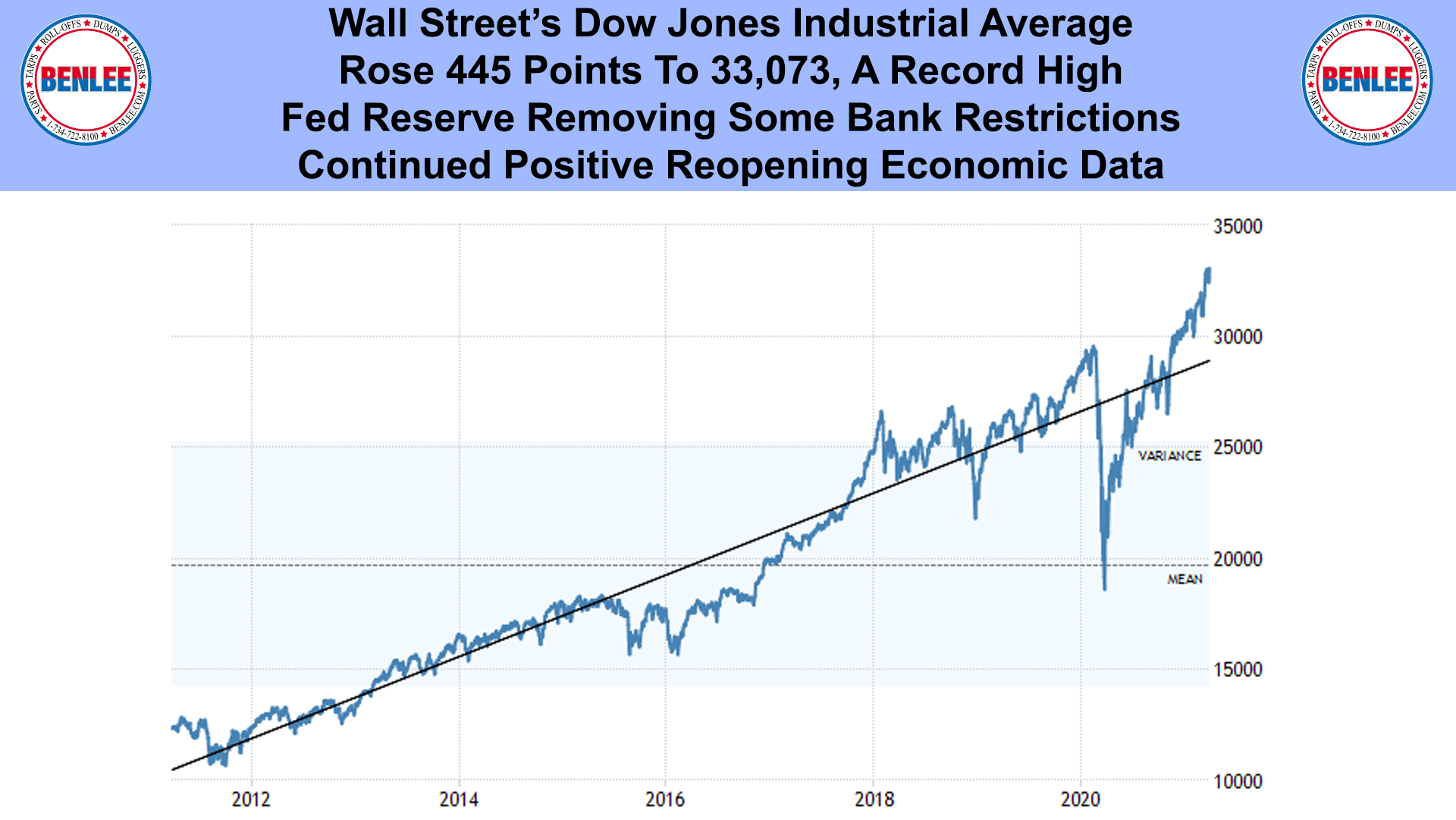

Wall Street’s Dow Jones Industrial Average rose 445 points to 33,073 a record high on the Federal Reserve removing some bank restrictions and on continued positive reopening economic data.

Member

Member