Loading price data

This is the Global Economic, Commodities, Scrap Metal and Recycling Report, by our BENLEE Roll off Trailer and Lugger Truck, July 13th, 2020.

Covid-19 Update. Forecasted U.S. were raised dramatically to a horrific 208,255 through Nov 1st with a mind numbing 135,174 Americans dead in the last 18 wks. Bad news is hospitalizations are now at record levels in multiples states and the number of people testing positive which is about 1% in NY, is a record 33.5% in Miami-Dade County. Worse is that the U.S. daily death count is up dramically after months of decline. As for Good news-There were zero COVID deaths in NYC Saturday, from a high of 799 a couple of months ago.

U.S. weekly steel production rose to 1.268M Tons. U.S. manufacturing is opening slowly.

Oil price rose to $40.55/b, a multi month high on a slow demand increase and as massive production cuts remain in place.

The U.S. Oil rig count fell to 181, a 10+ year low, down a staggering 88.8% from the high, as low prices and U.S./OPEC commitment to cut production remain in place.

U.S. oil production was steady at 11.0M/b/d, as the same low prices and U.S./OPEC commitment to cut production remain in place.

Iron ore rose to $107/ton, near a 1 year high, as Chinese steel mills are ramping up on a Chinese government commitment to infrastructure investment.

Scrap #1 HMS Export Buying price Philly, fell to $200/GT on good supply and moderate export demand.

Scrap steel #1 HMS fell to $205.83/GT. U.S. and global demand remain fair, while supply remains good.

Hot Roll Coil steel fell to $23.25 per hundred on a small demand increase, but more supply in the market and lower scrap prices.

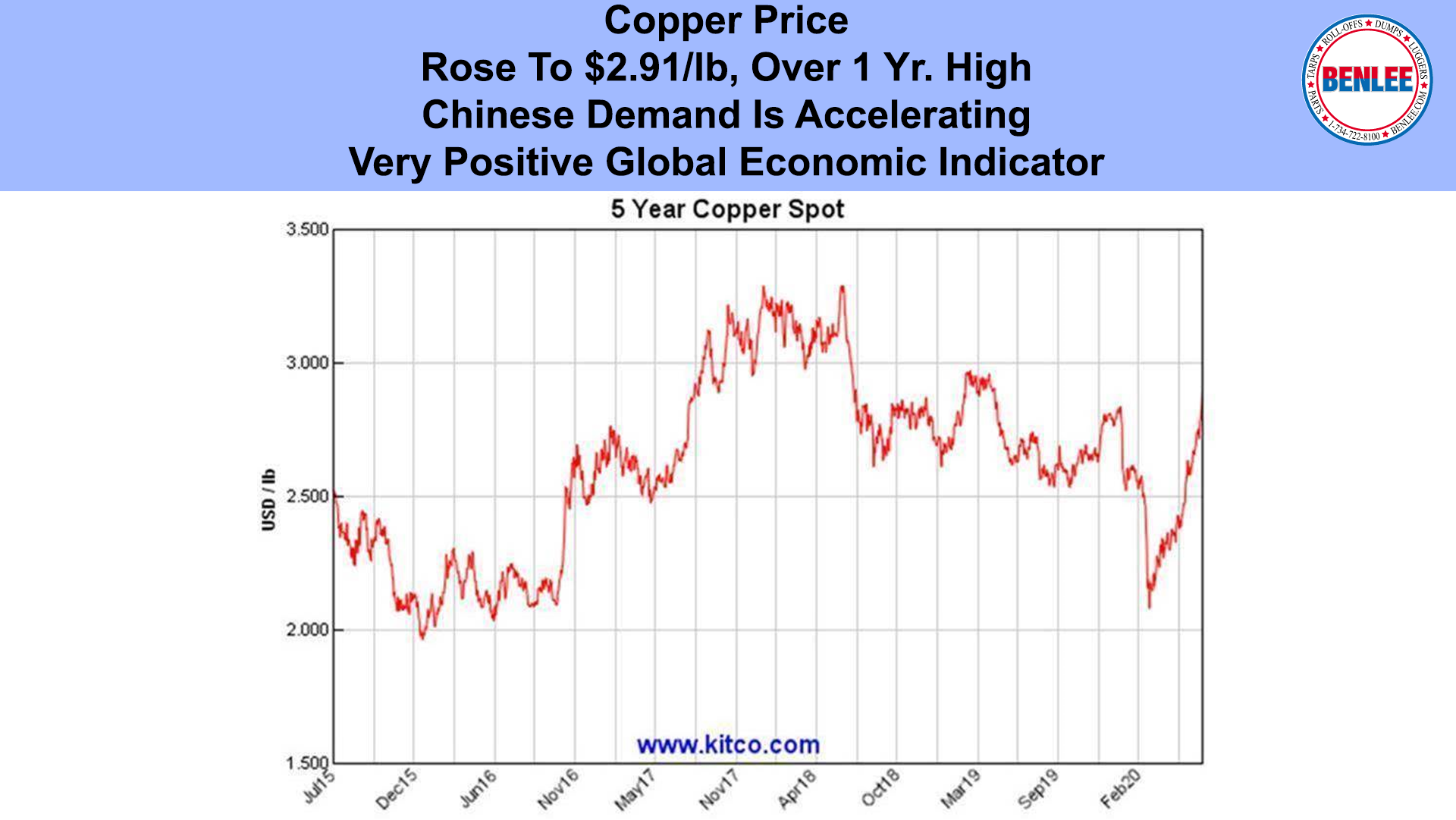

Copper rose to $2.91 per pound, over a 1 year high, as Chinese demand is accelerating. This is a very positive global economic indicator.

Aluminum rose to 75.21 cents a multi month high on increasing global demand.

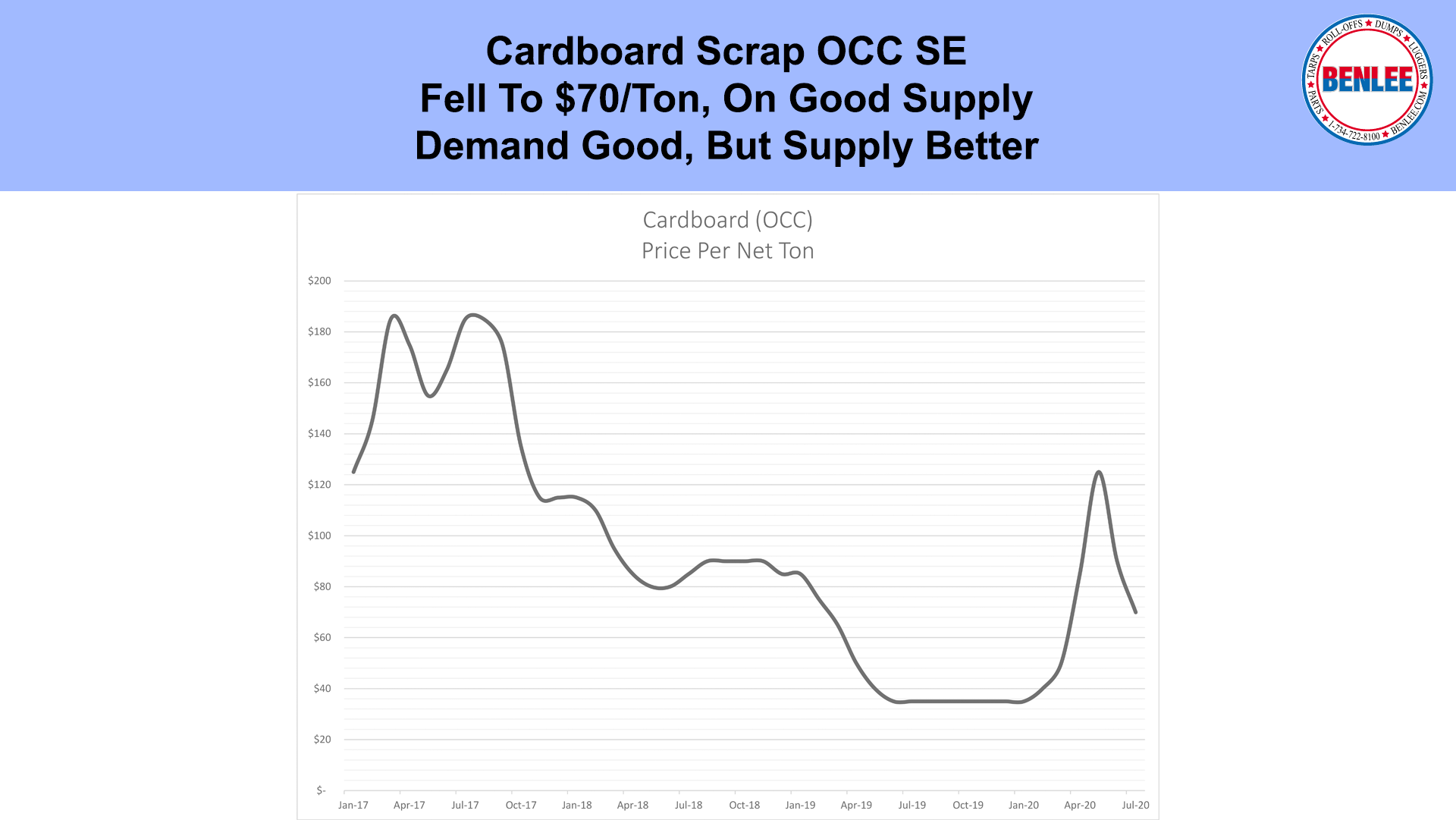

July’s Cardboard Scrap OCC SE fell to $70 per ton, on good supply. Demand has been good, but supply has been better.

JP Morgan’s Global economic index rose to 47.7, but below 50 is contraction, so the global economy is contracting slower. This is a good sign as much of the world reopens.

June’s U.S. Vehicle sales rose to 13 million annualized. There is no forecast that gets back to the 2017 rate of 18M plus.

July’s IBD/TIPP U.S. Economic optimism index fell to 44, the lowest since September 2015, on the concern over surging COVID cases, as the number of states began reversing their reopening and American deaths per day is now escalating.

June’s U.S. Composite Purchasing Manager’s Index rose to 47.9, well above May’s 37, but as below 50 is contraction, it is contracting less, so there is some optimism. The trend though remains down from mid-2018 high, brought by the tax cut.

Wall Street’s Dow Jones Average rose 248 points to 26,075 as governments remain pumping up the economy around the world, but COVID’s resurgence is creating nervous investors.

Member

Member