Loading price data

This is the Global Economic, Commodities, Scrap Metal and Recycling Report, by our BENLEE Roll off Trailer and Open Top Trailer, September 21st, 2020.

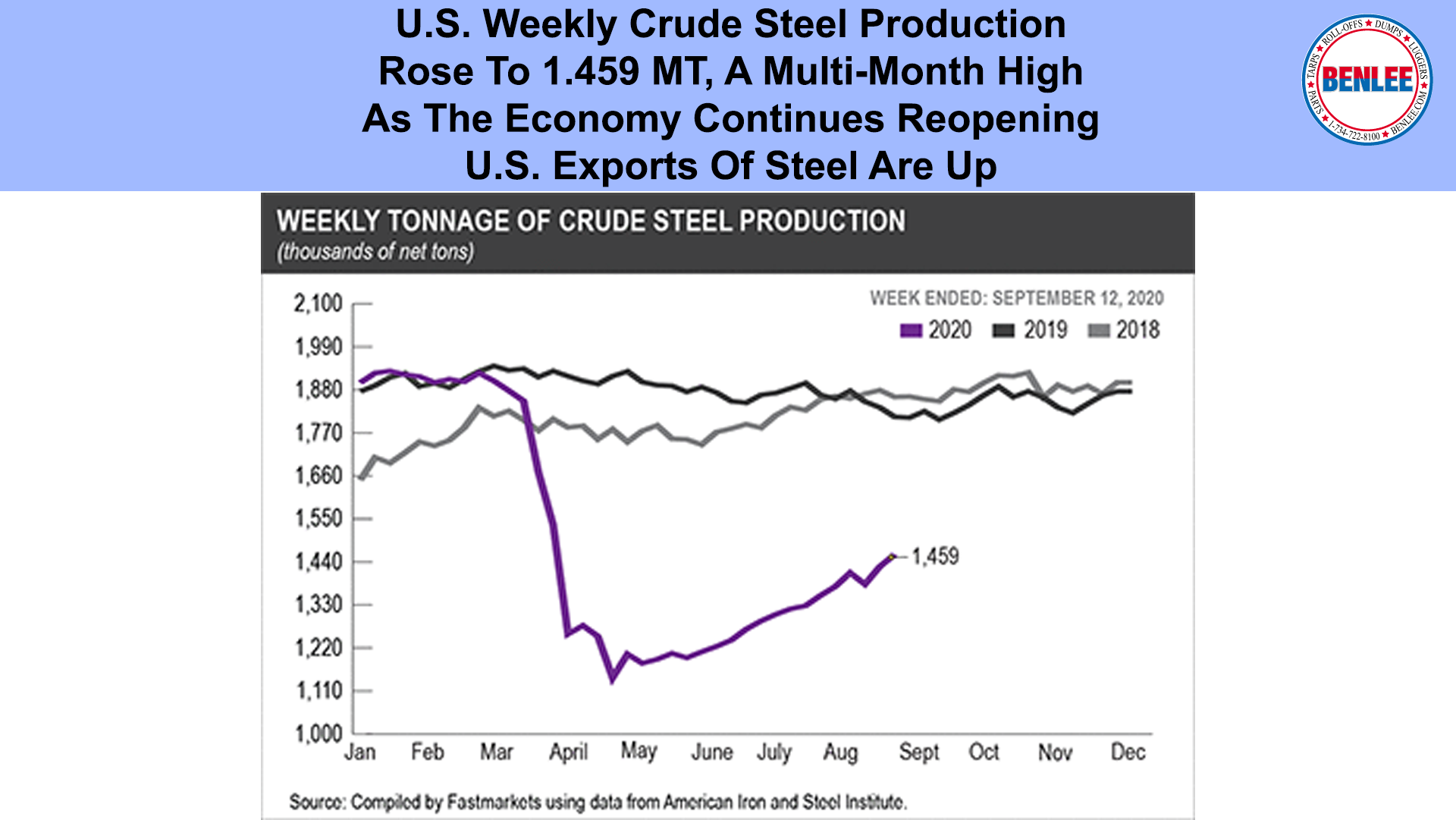

U.S. Weekly crude steel production rose to 1.459 MT, a multi month high as the economy continues reopening and as U.S. exports of steel are up.

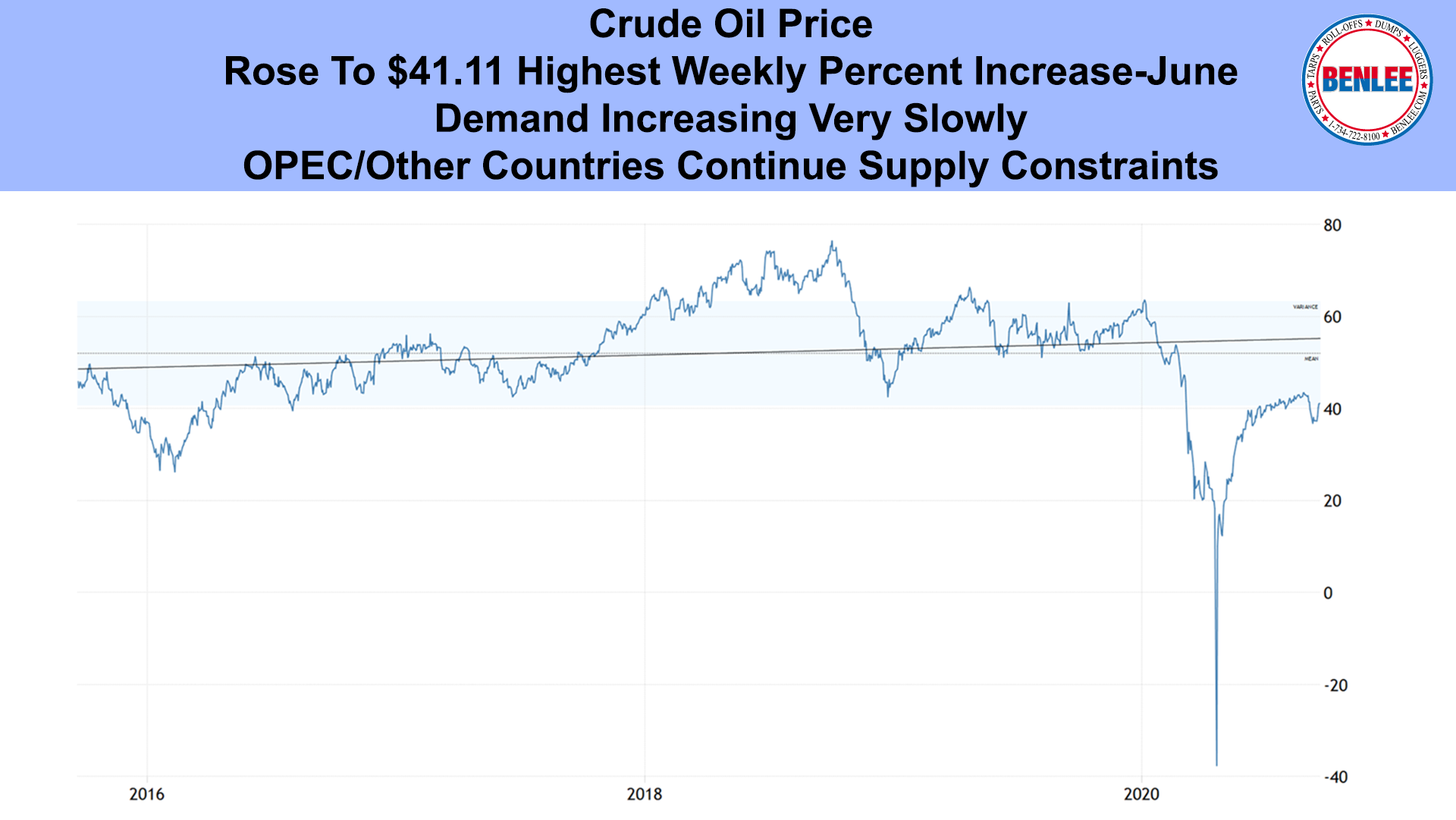

Crude Oil price rose to $41.11/b, with the highest weekly percent increase since June, as demand is increasing very slowly and OPEC and other countries, continue supply constraints.

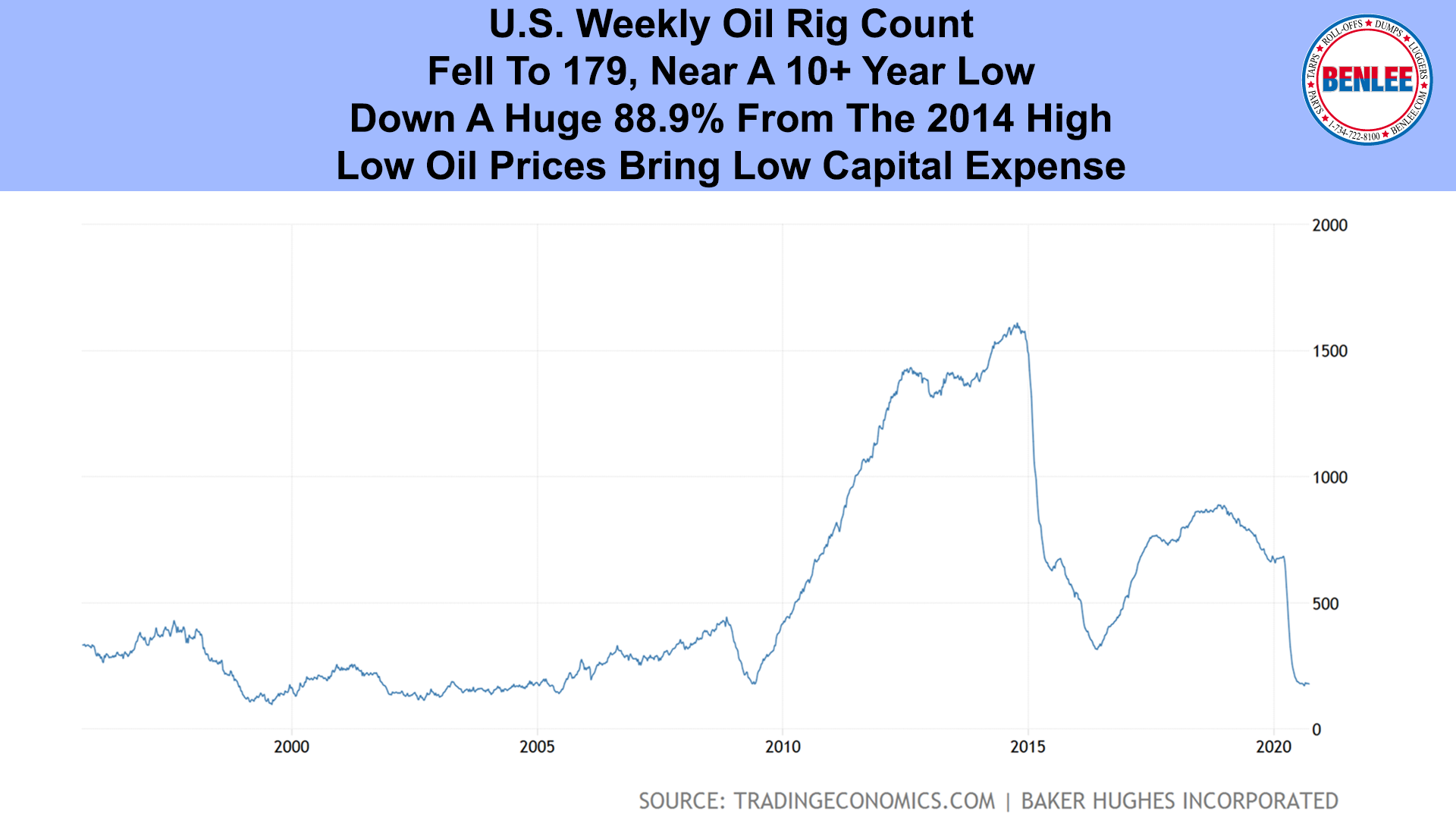

The U.S. Oil rig count fell to 179, near a 10 plus year low, down a huge 88.9% from the 2014 high. Low oil prices bring low capital expense.

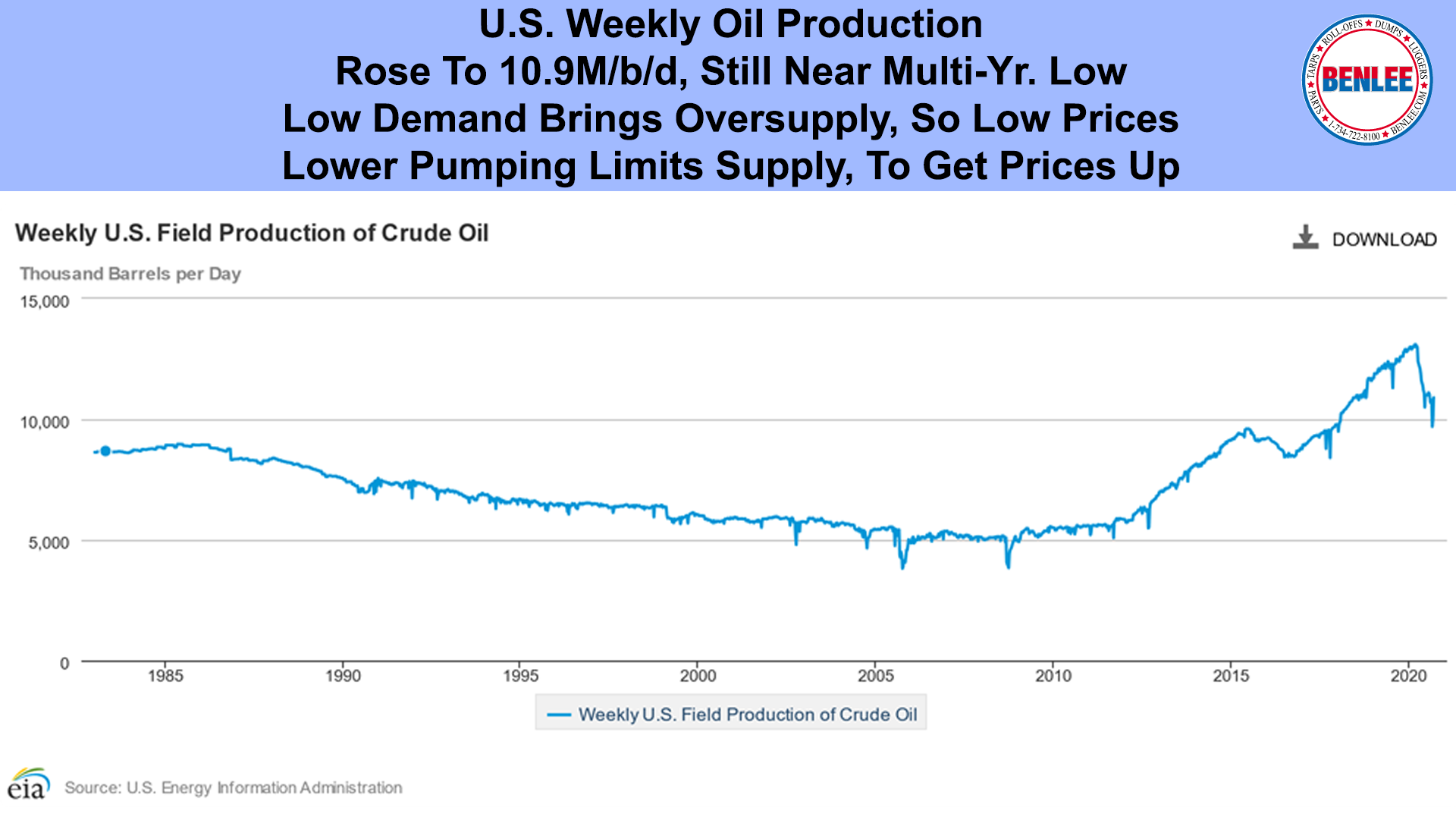

U.S. weekly oil production rose to 10.9M/b/d, still near a multi-year low. Low demand brings oversupply, so low prices. Lower pumping limits supply, to get prices up.

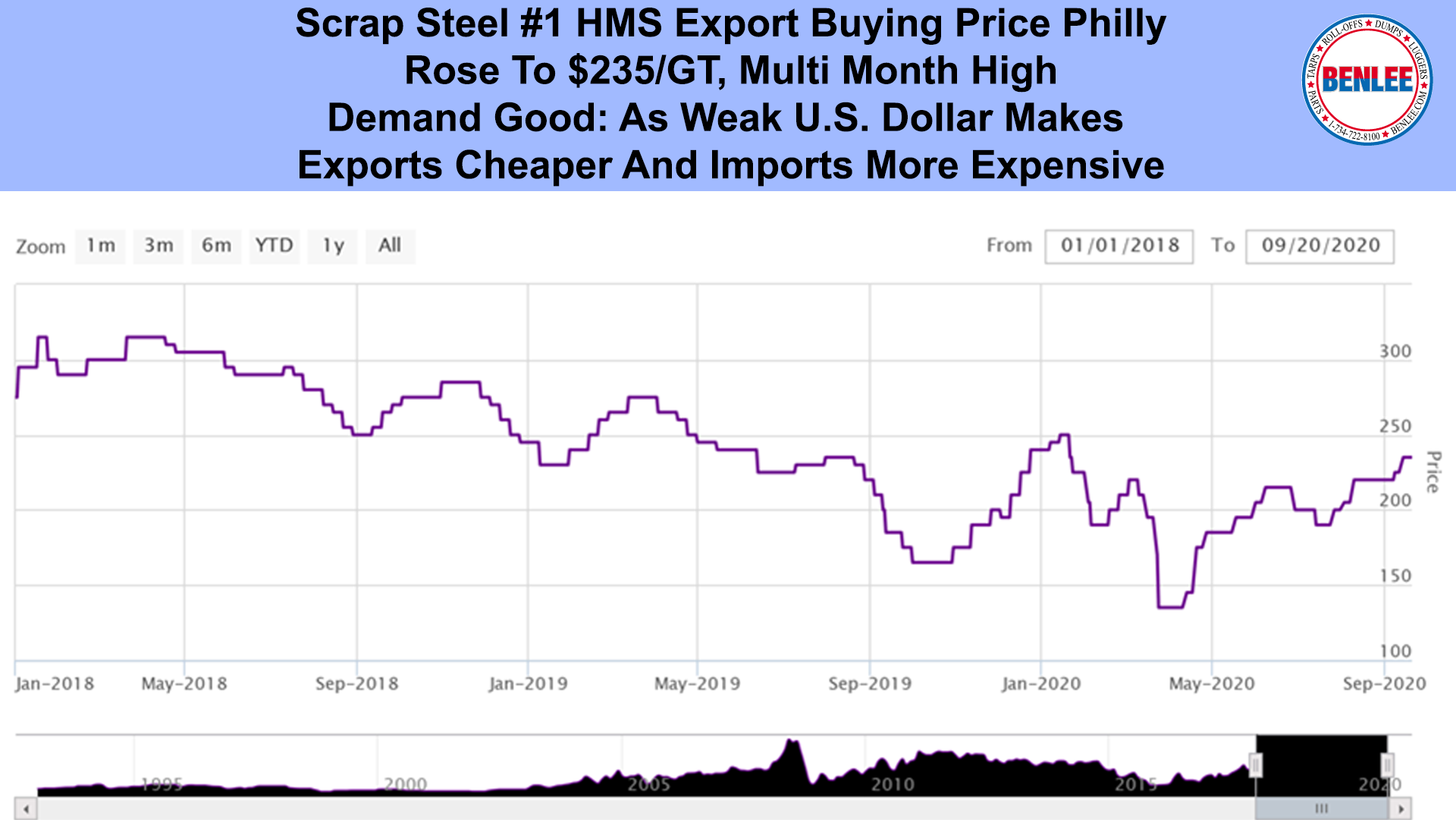

Scrap Steel #1 HMS Export buying price Philly, rose to $235/GT a multi month high. Demand is good, as a weak U.S. Dollar makes exports cheaper and imports more expensive.

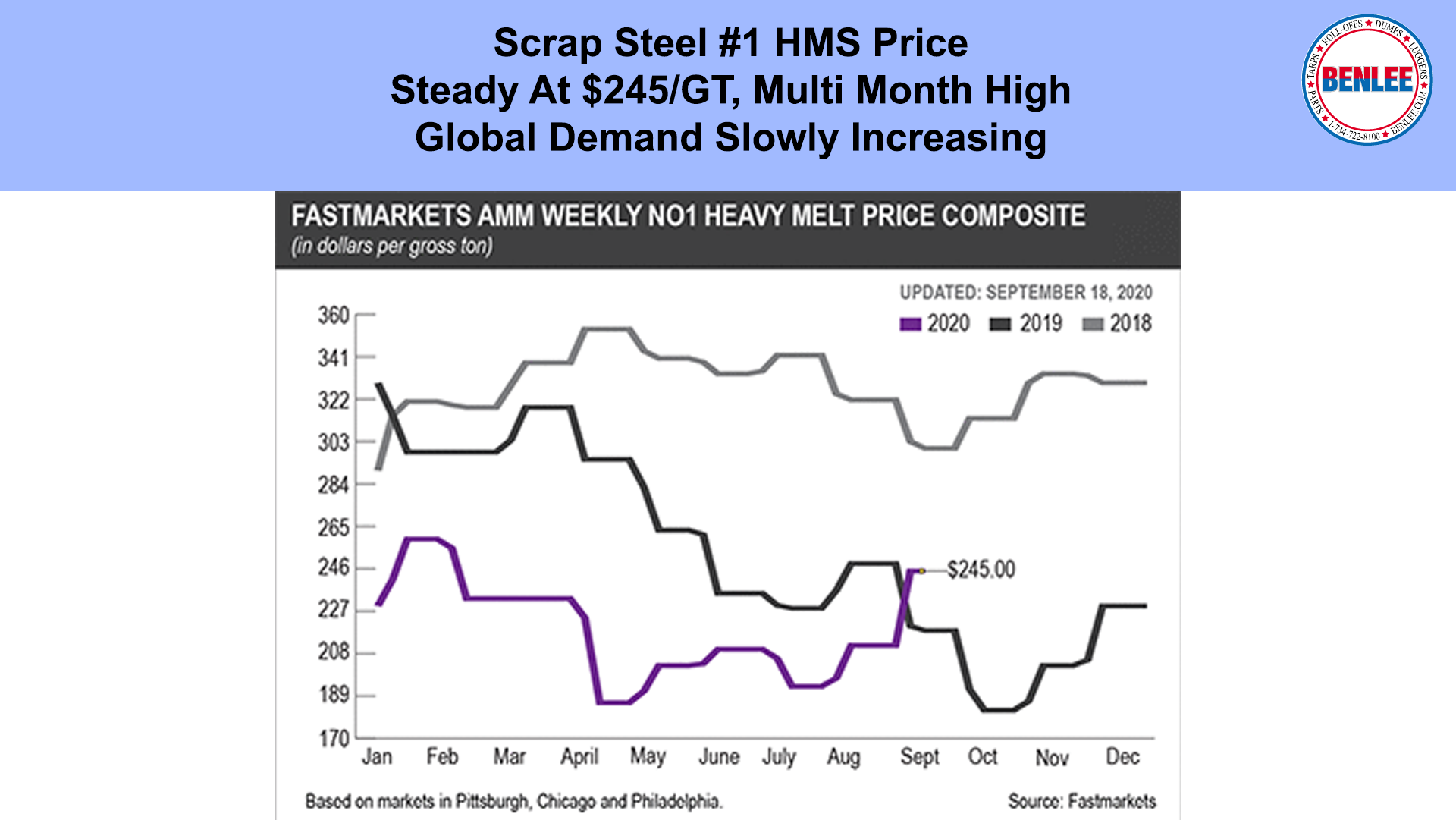

Scrap steel #1 HMS price was steady at $245/GT, a multi month high as global demand is slowly increasing.

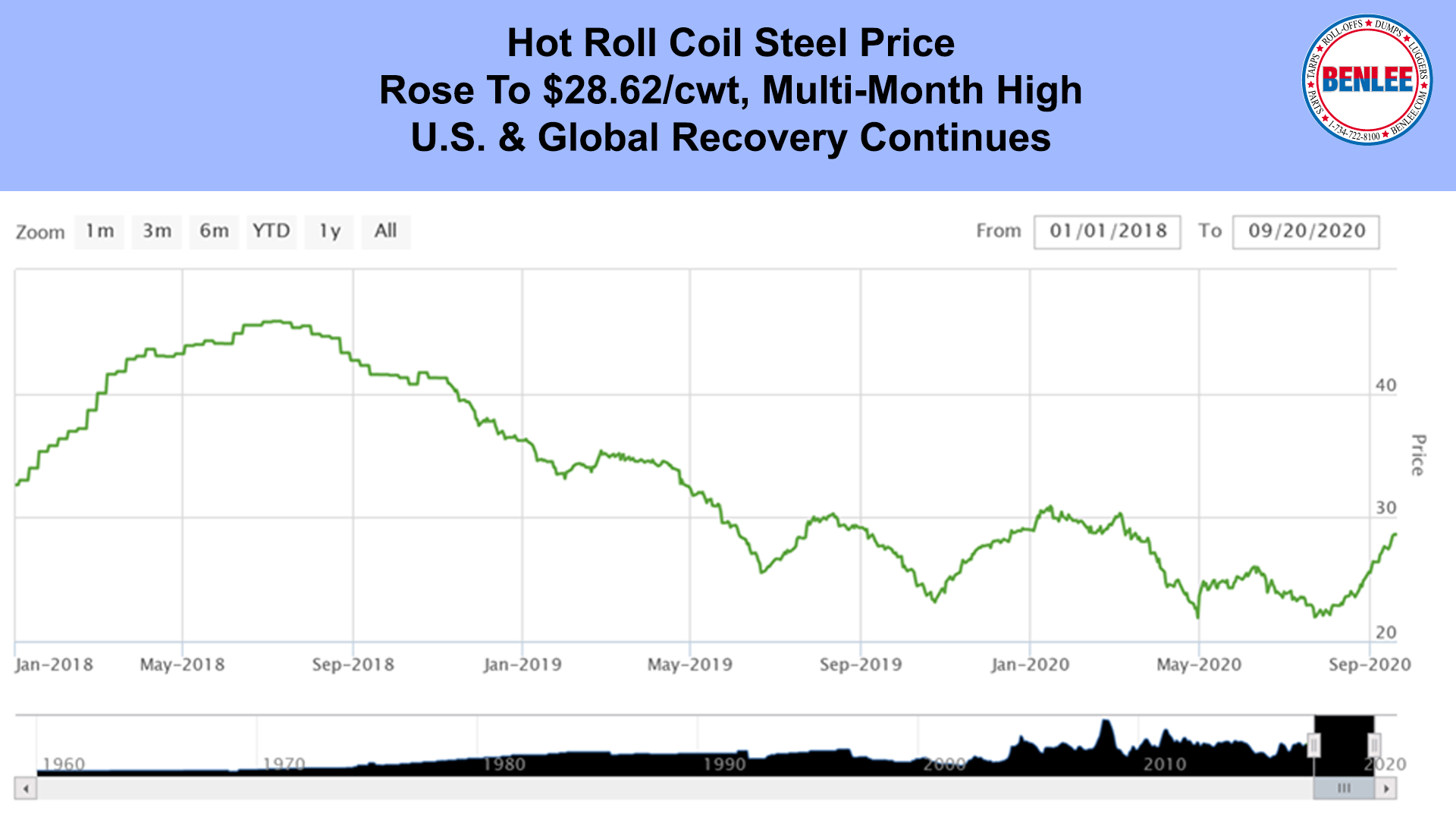

Hot Roll Coil steel rose to $28.62/cwt, a multi month high as the U.S. & global recovery continues.

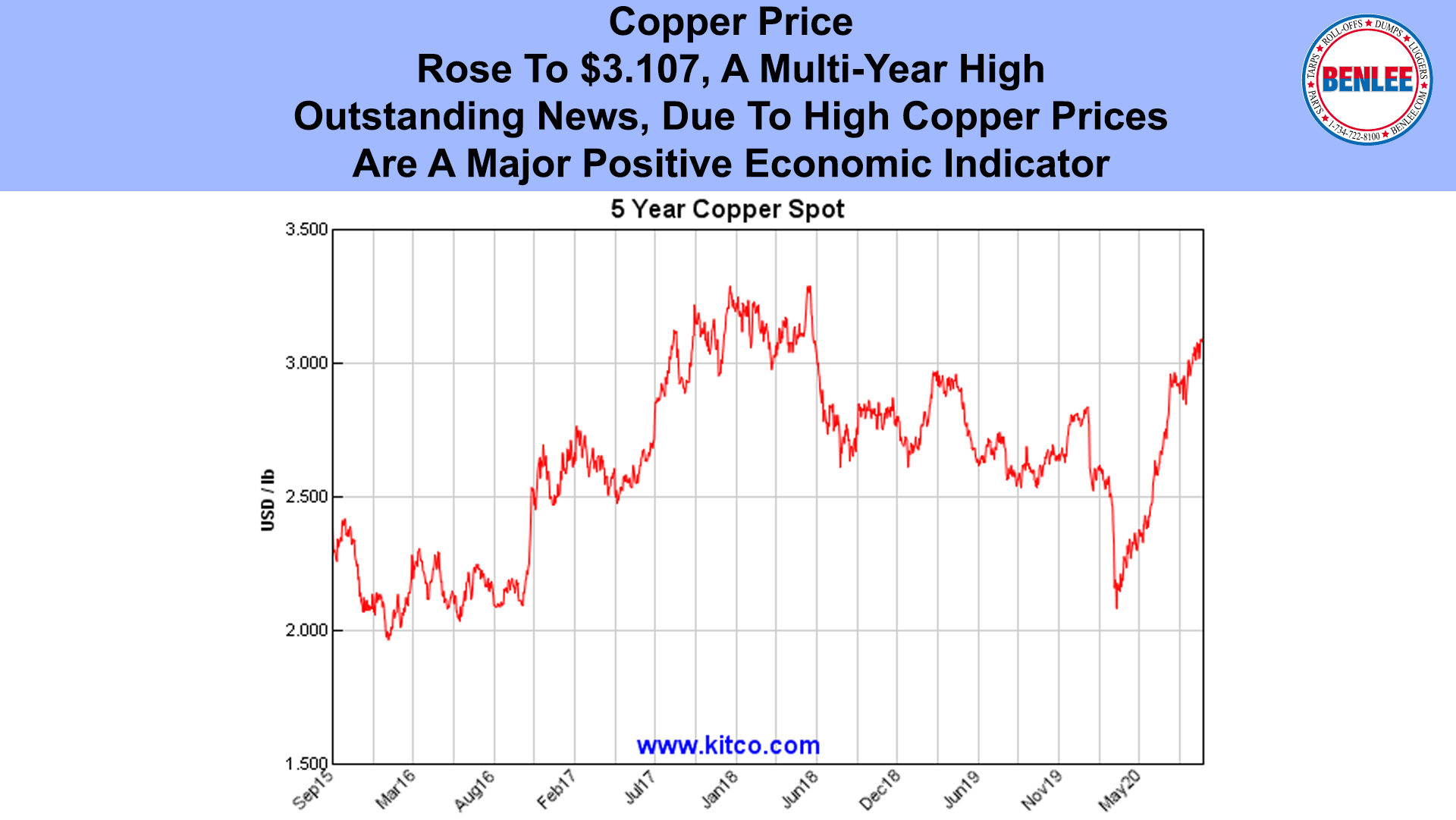

Copper Price rose to $3.107/lb. a multi-year high. This is outstanding news, due to high copper prices are a major positive economic indicator.

Aluminum price rose to $.795/lb. near a multi-year high as slow growth continues and there is a good balance of supply and demand.

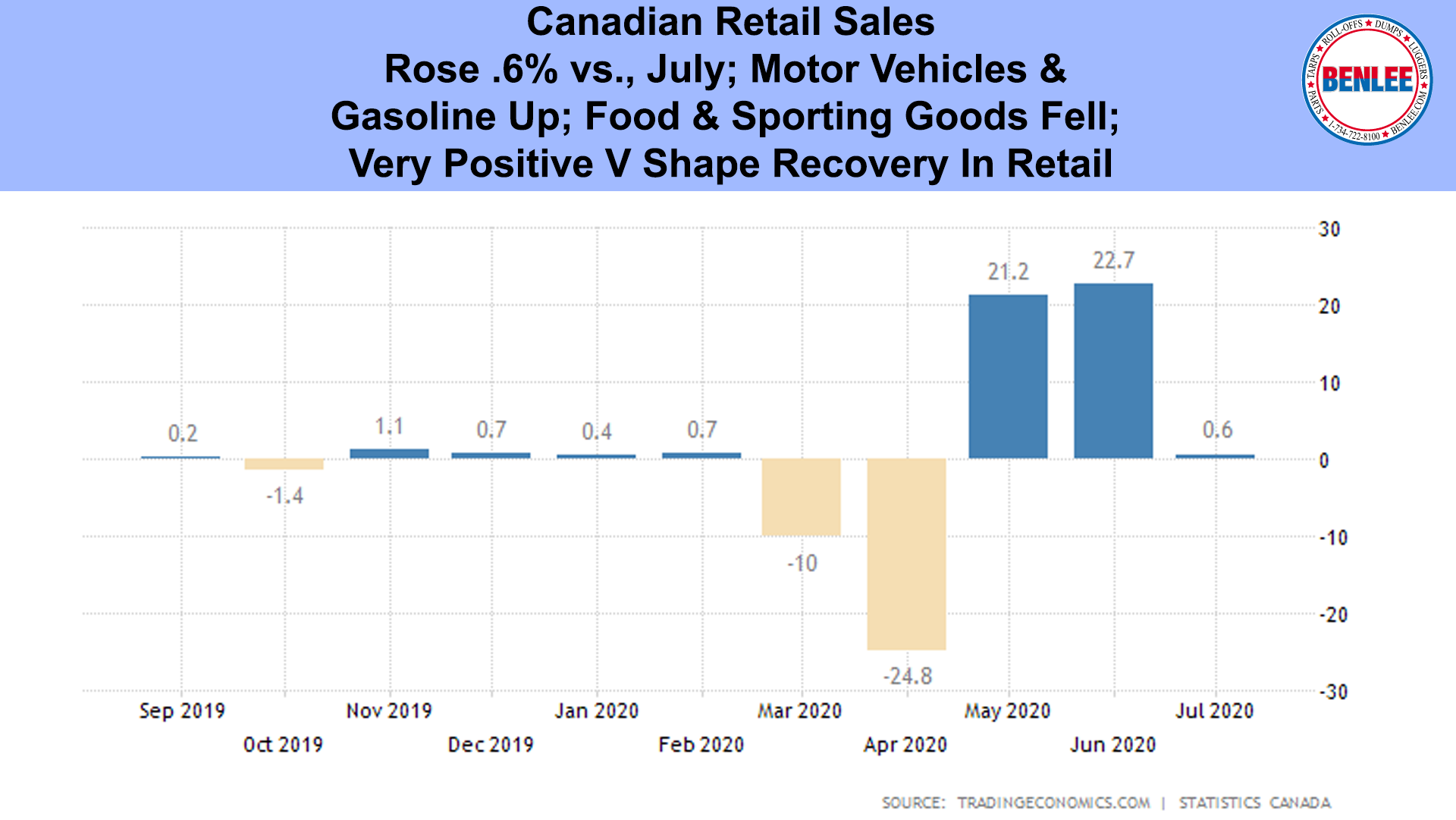

Canadian retail sales rose .6% vs. July, as motor vehicles and gasoline were up and food and sporting goods fell. This is a very positive v shape recovery in retail.

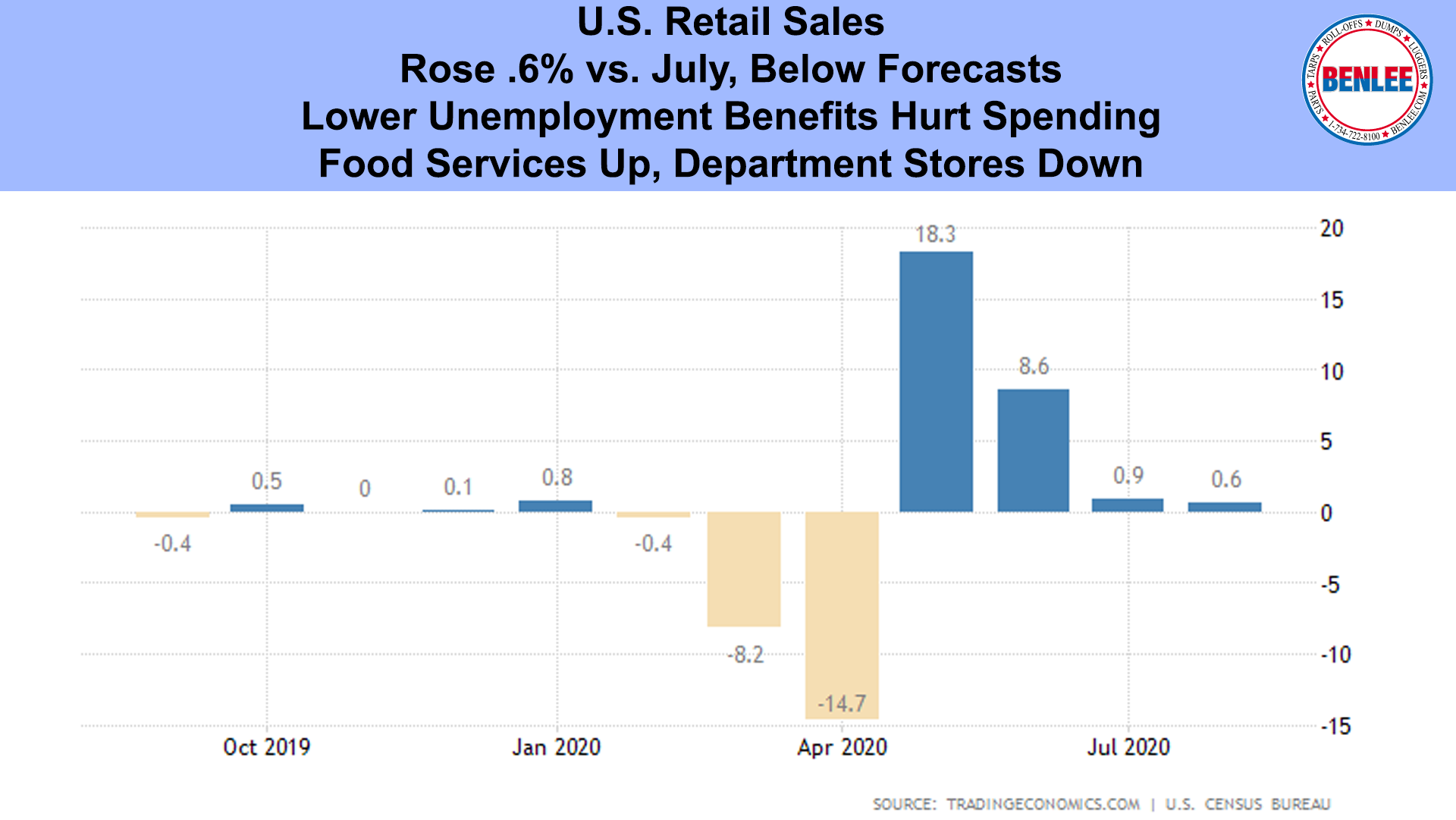

U.S. retail sales rose .6% vs. July, which was below forecast. Lower unemployment benefits hurt spending. Food services were up and department stores were down.

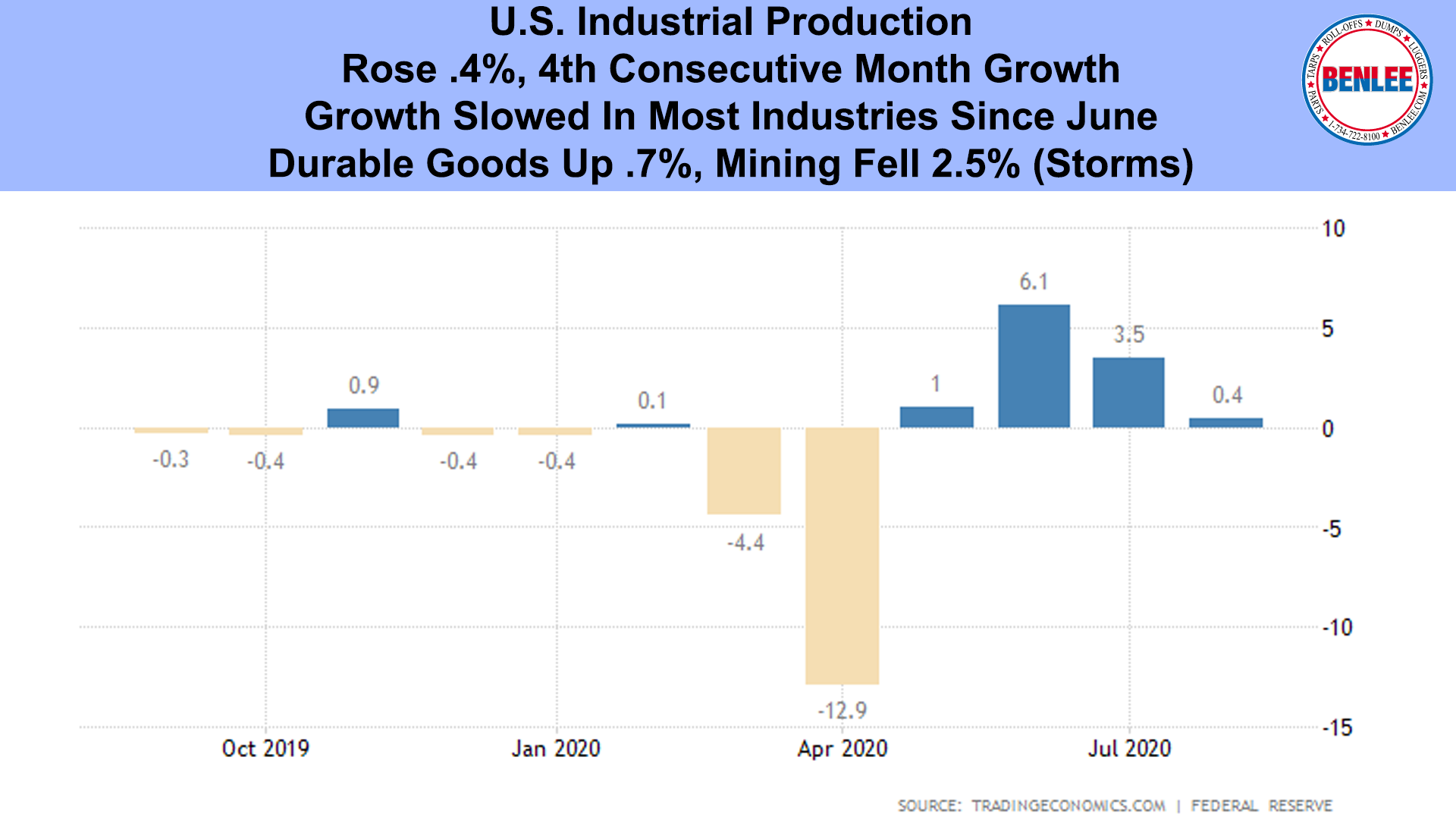

U.S. industrial production rose .4%, the 4th consecutive month of growth. Growth slowed in most industries since June. Durable goods were up .7% and mining fell 2.5%, mostly due to the recent hurricanes.

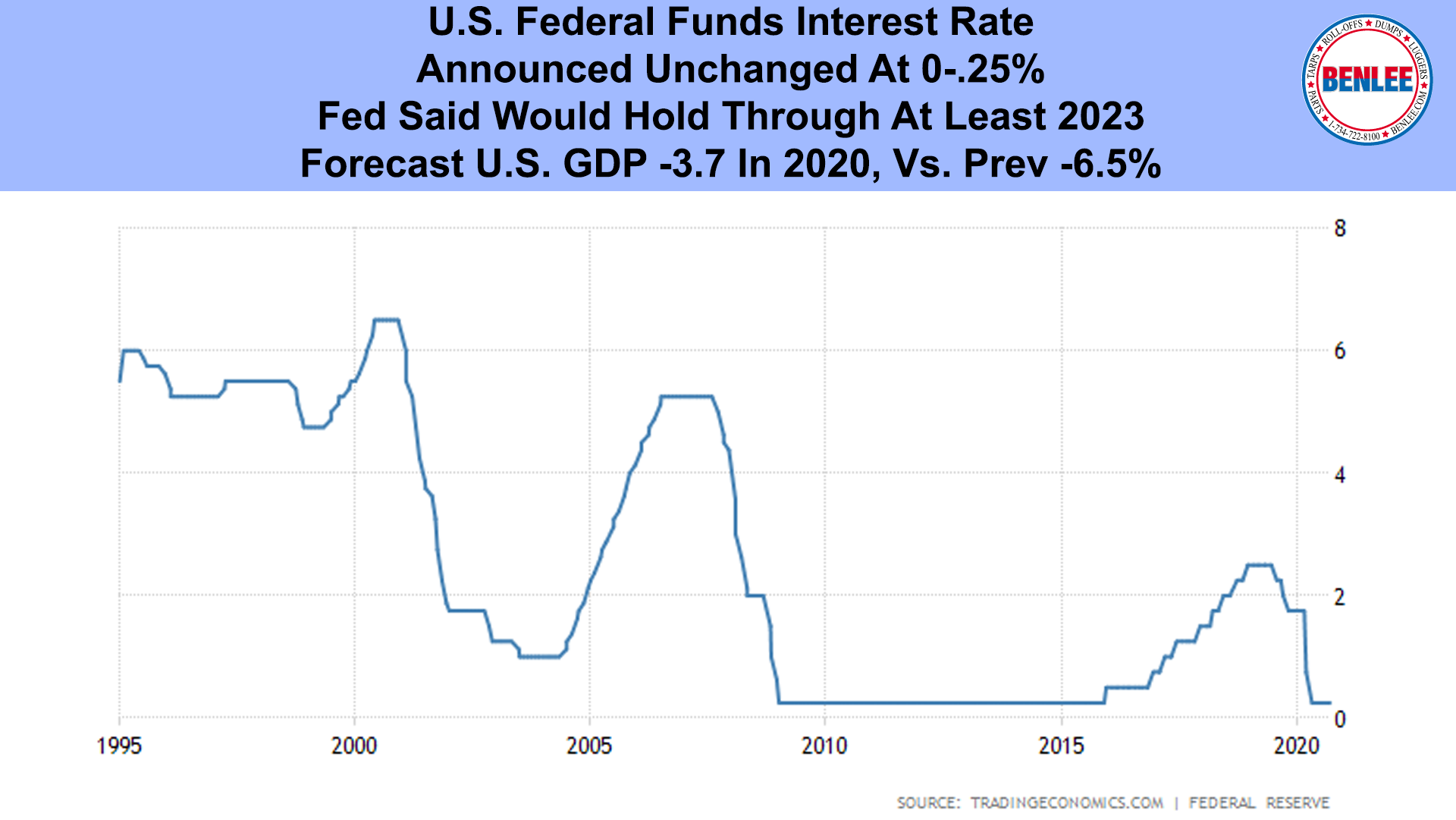

The U.S. Federal Funds interest rate was announced to be unchanged at 0 to .25%. The Fed said they would hold this through at least 2023. They also said, they forecast U.S. GDP would be negative 3.7% in 2020 vs. their previous forecast of -6.5%.

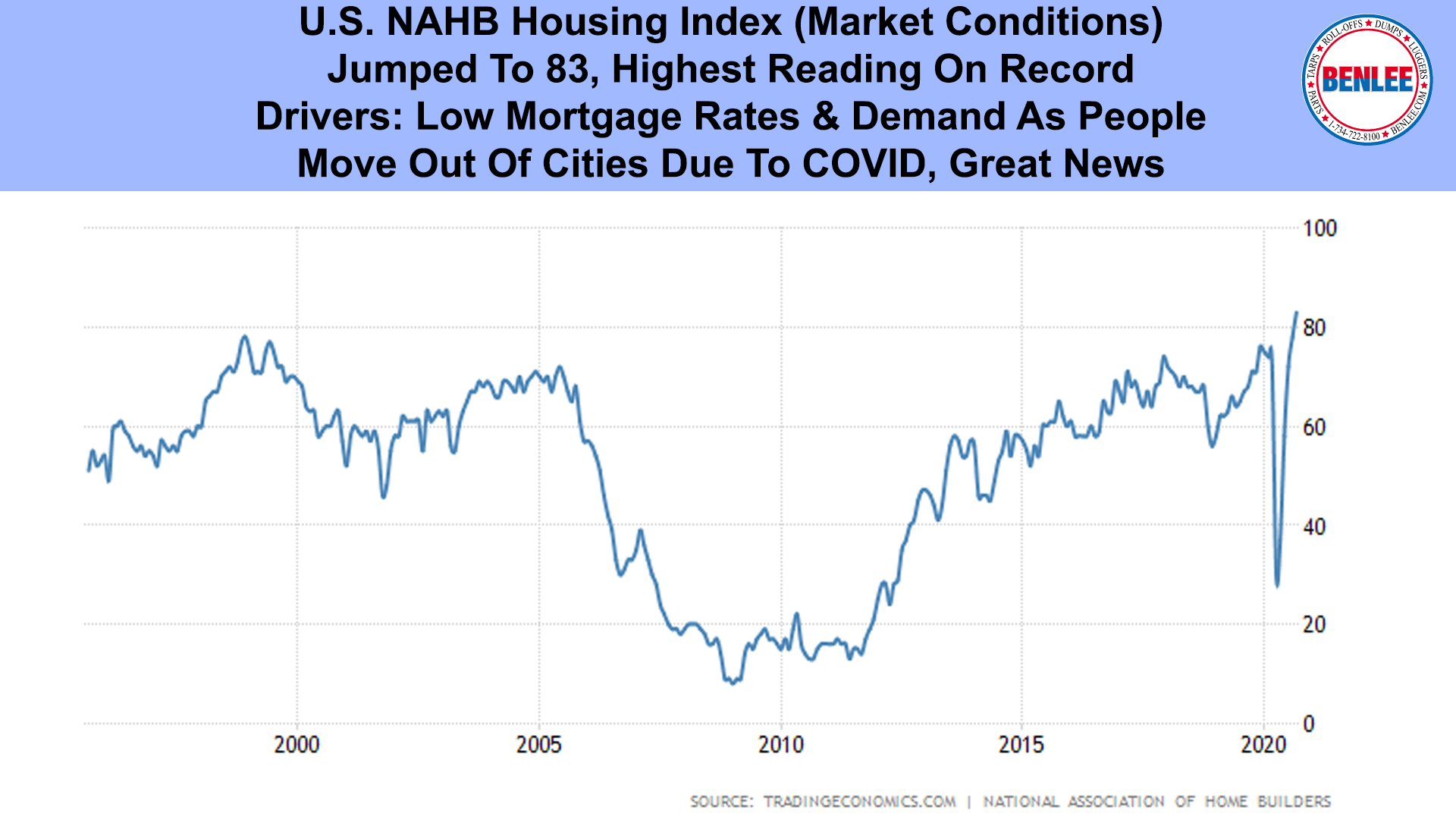

The U.S. NAHB housing index which indicates market conditions jumped to 83, the highest on record. Drivers were low mortgage rates and demand, as people move out of the cities due to COVID. This is great news.

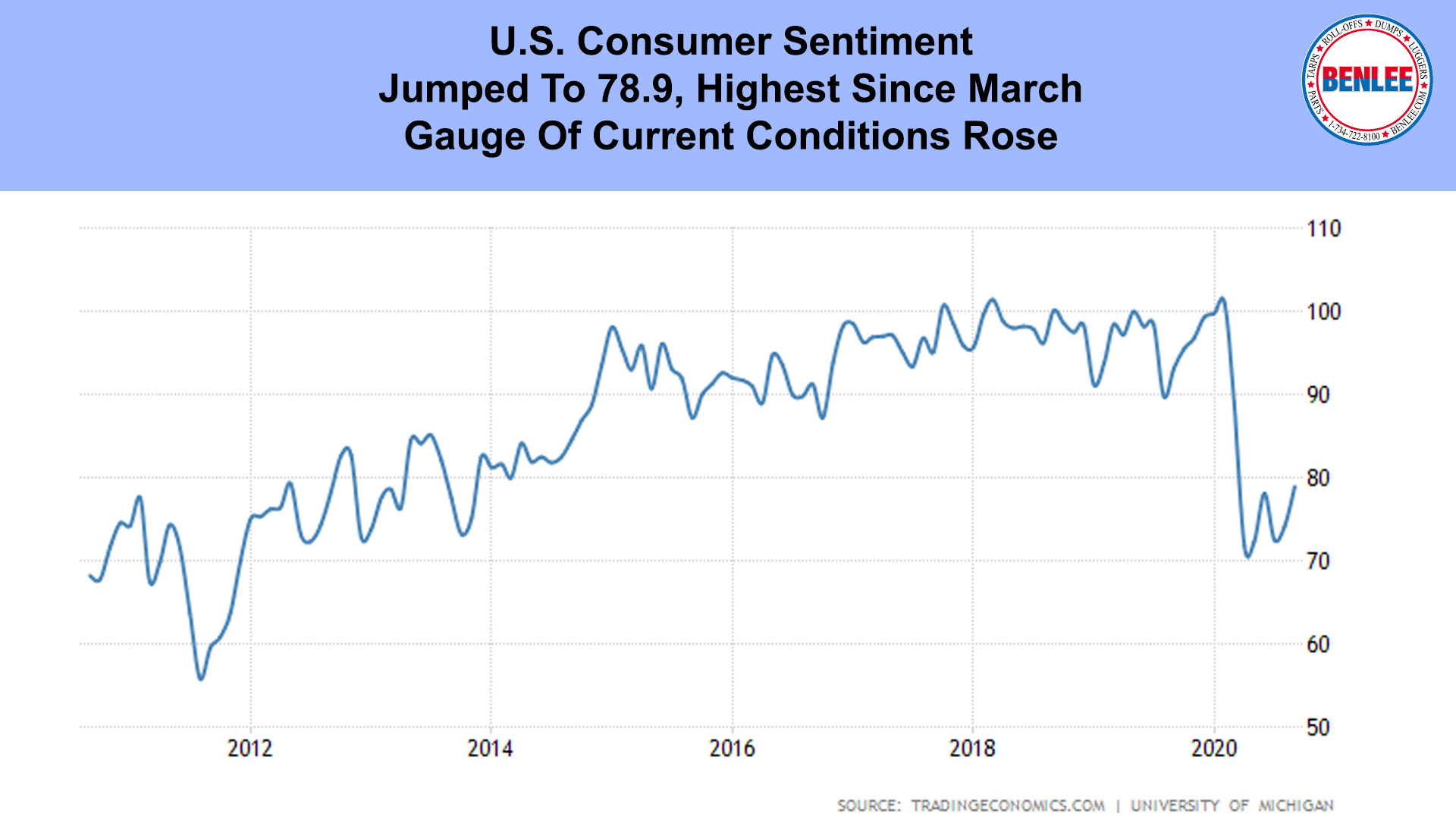

U.S. Consumer Sentiment, jumped to 78.9, the highest since March. The gauge of current conditions rose.

U.S. Initial unemployment claims fell to 860K, the third month under 1M, which is good news, but it remains well above 665,000 which was the peak of the great recession in 2009.

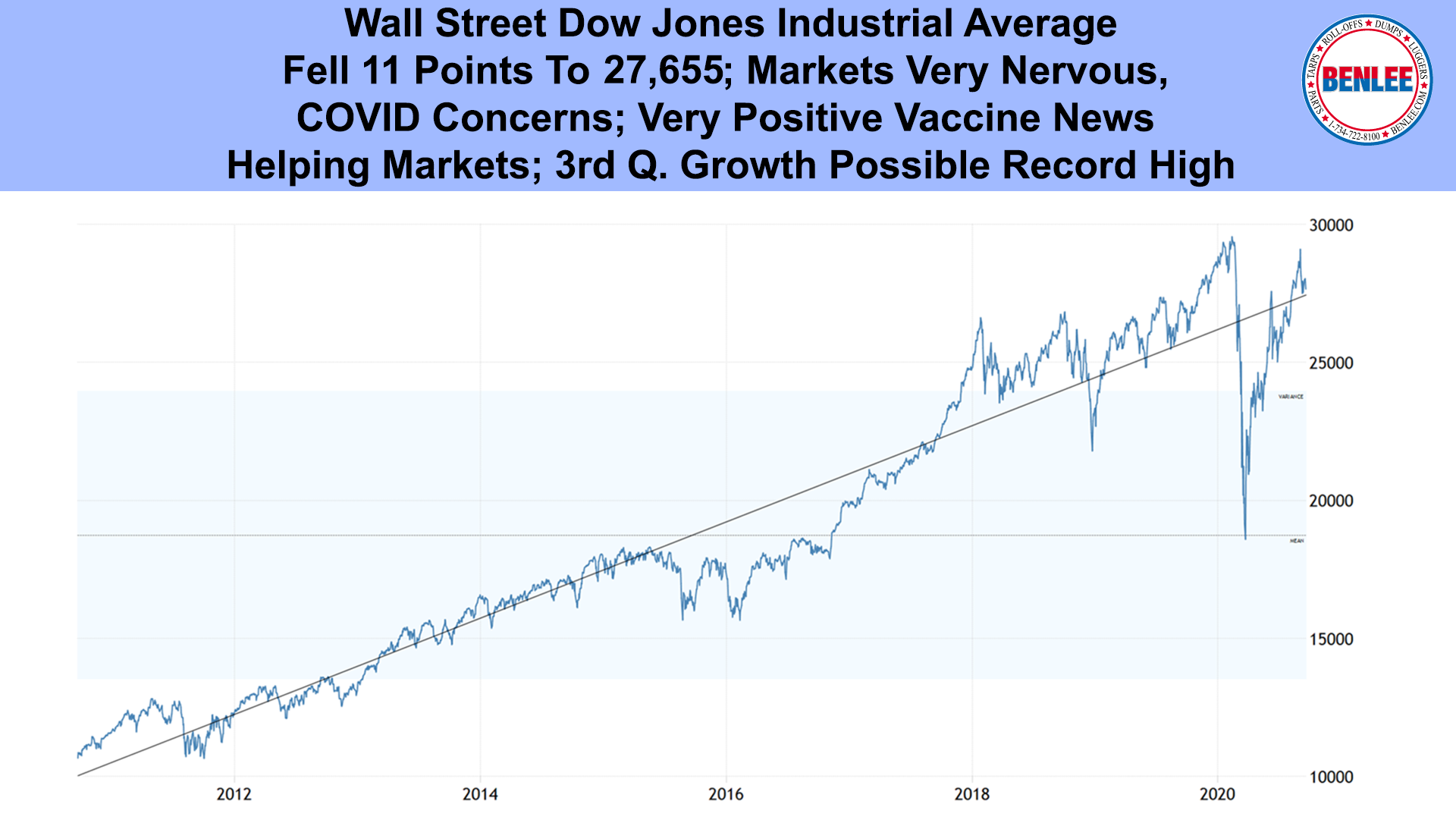

Wall Street’s Dow Jones Industrial Average fell 11 points to 27,655 as markets are very nervous over COVID concerns. There has been very positive vaccine news which is helping the markets. Importantly, 3rd quarter growth could be a record high.

Member

Member