Loading price data

This is the Global Economic, Commodities, Scrap Metal and Recycling Report, by BENLEE Roll off Trailers and Open Top Gondola Trailers, May 4th, 2020.

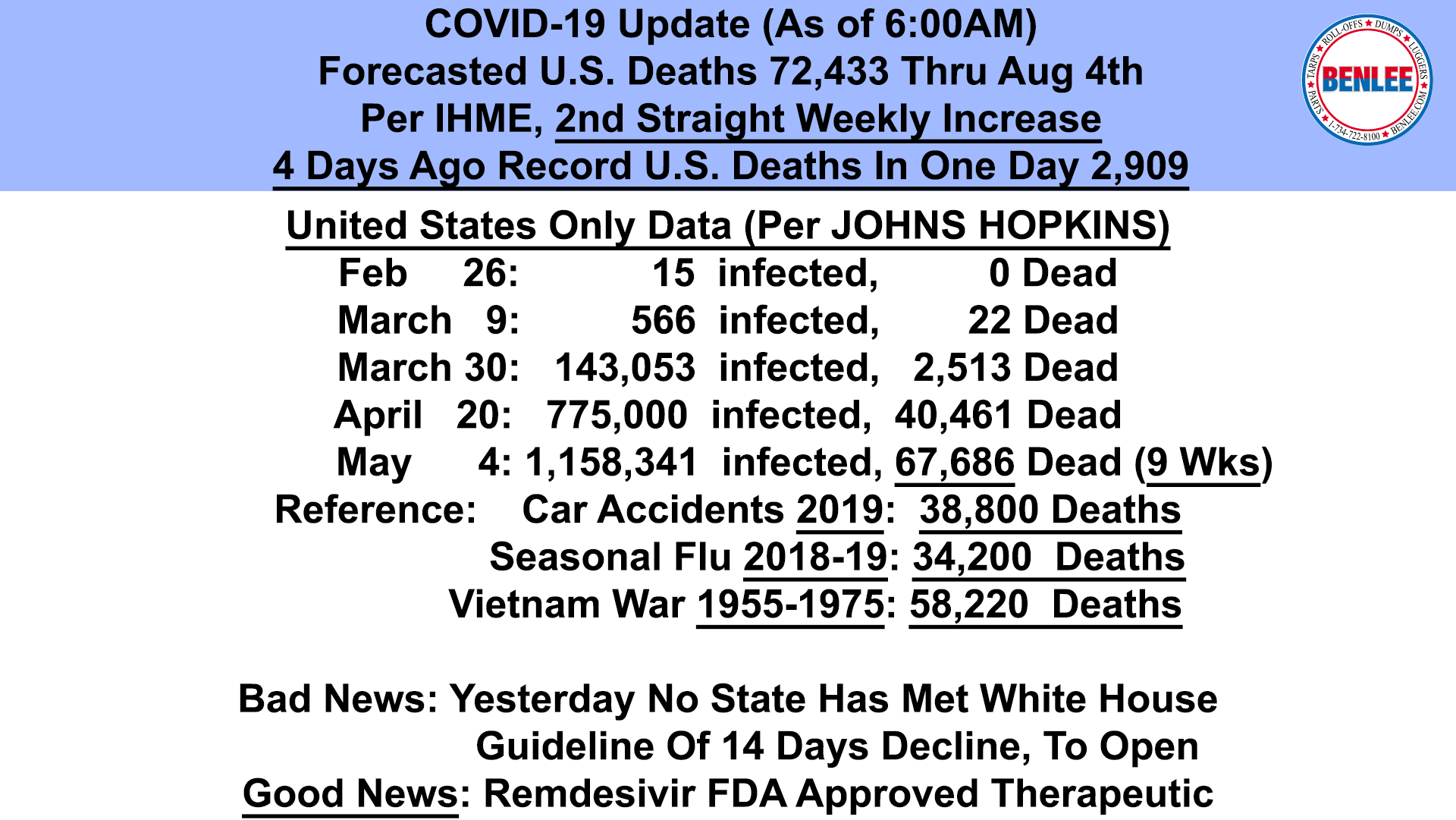

Covid-19 Deaths are now forecasted to be 73,433 which is troubling in that this forecast has increased for the second straight week. 4 days ago, the U.S. had the most COVID deaths in one day at 2,909; again, in one day. There are now 67,686 dead in the U.S., so there are now more dead in the past 9 weeks, than Americans died in the 20-year Vietnam war. Other bad news, as of Sunday, no U.S. State had met the White House guideline of 14 days decline in new cases, so as to reopen. Good news is, Remdesivir is now the first FDA drug approved as a therapeutic. A Vaccine is still about 8 to 18 plus months away.

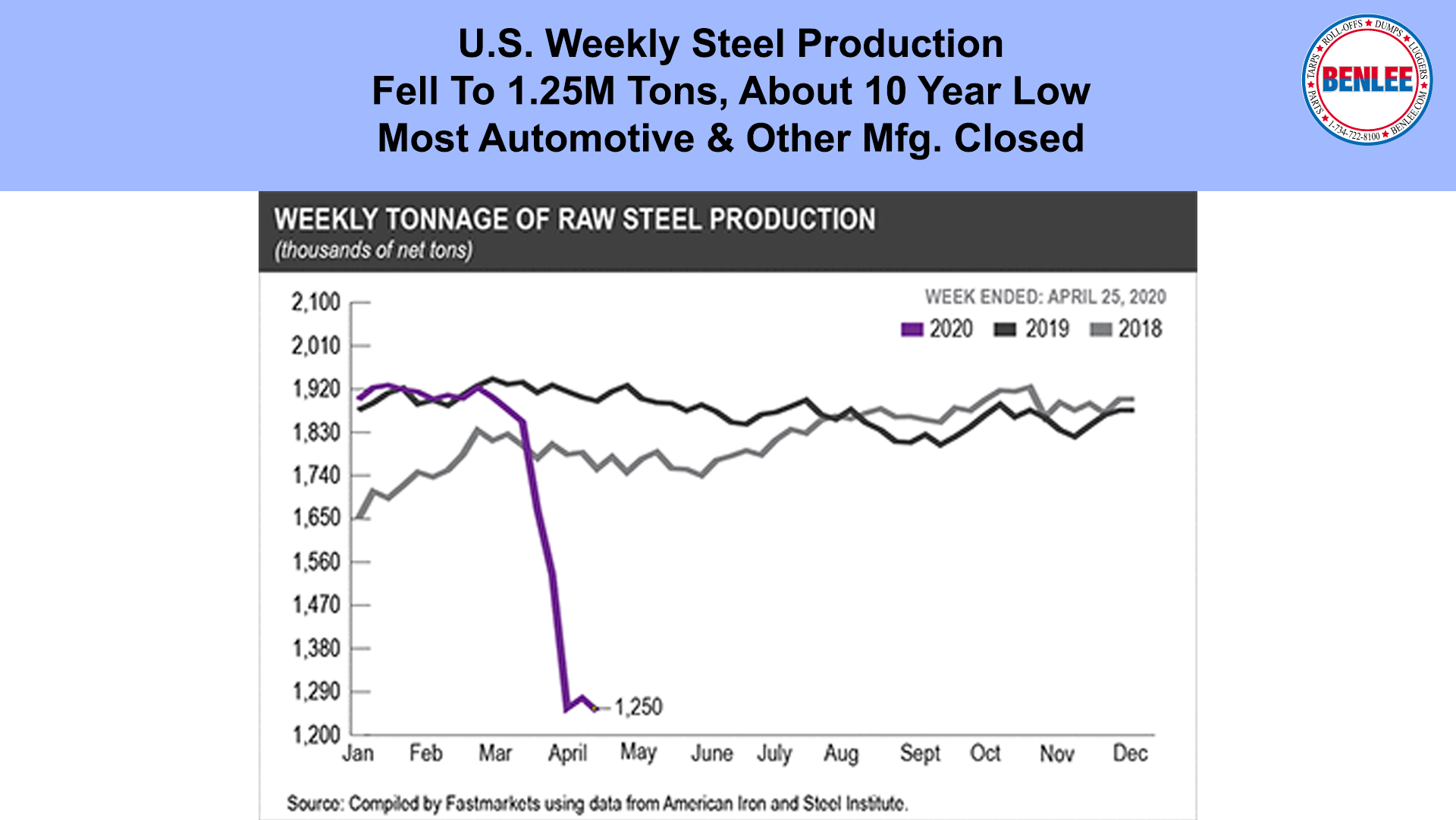

U.S. weekly steel production fell to 1.25M Tons, about a 10 year low as most automotive and other manufacturing remains closed.

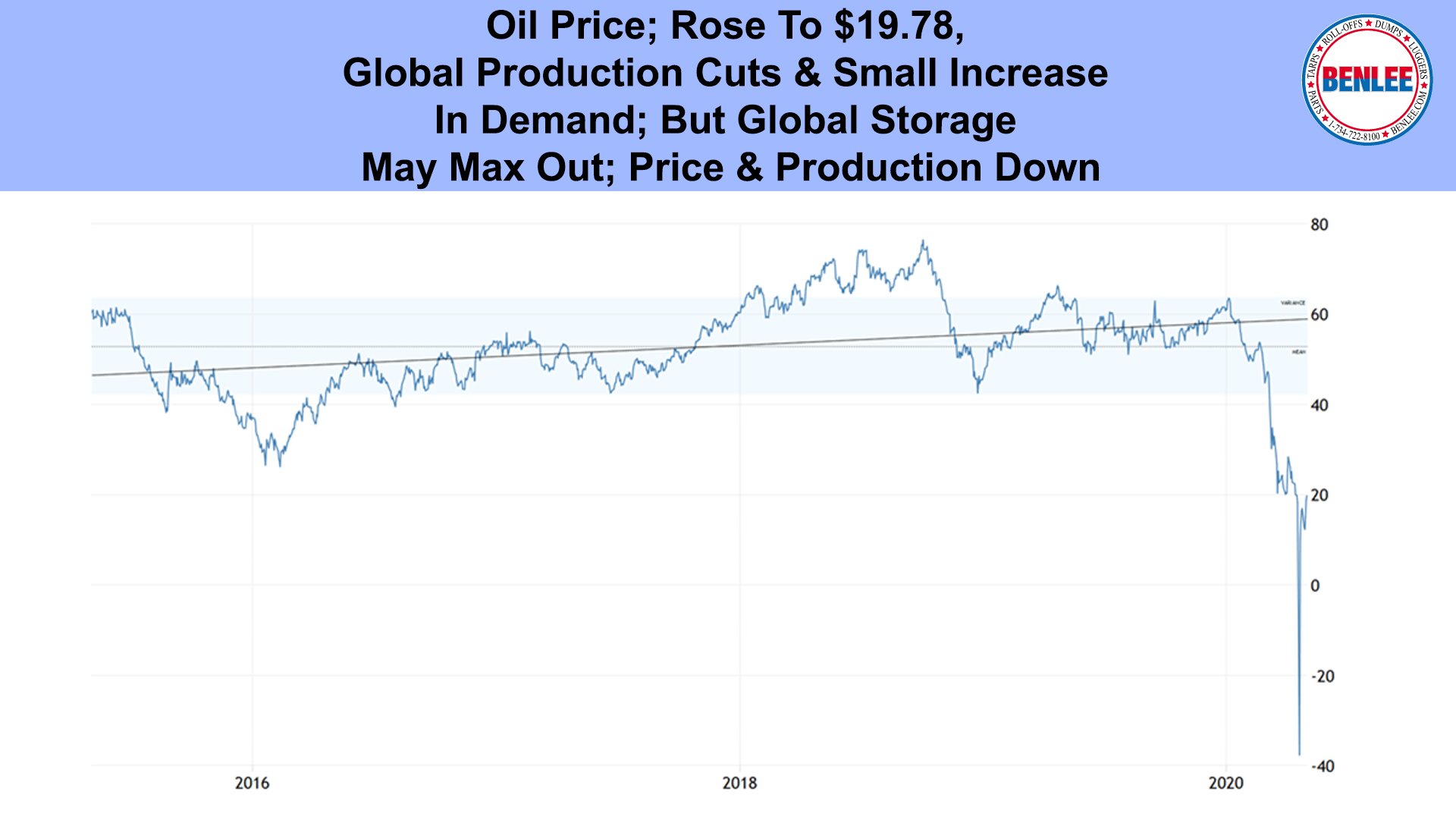

Oil price rose to $19.78/b, on global production cuts and small increases in demand, but global storage may max out, taking price and production down.

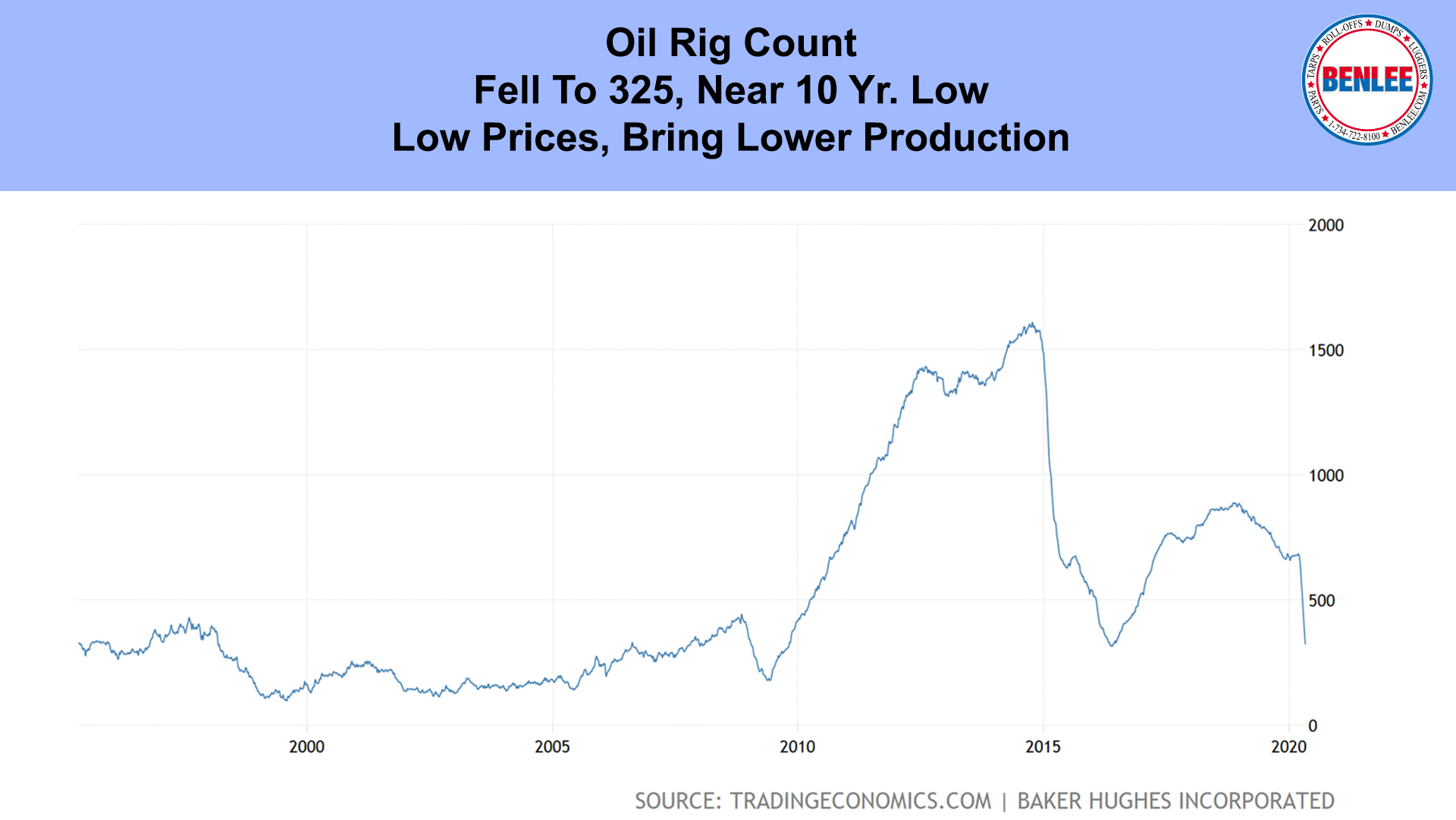

The U.S. Oil rig count fell to 325, near a 10 year low as low prices bring lower production.

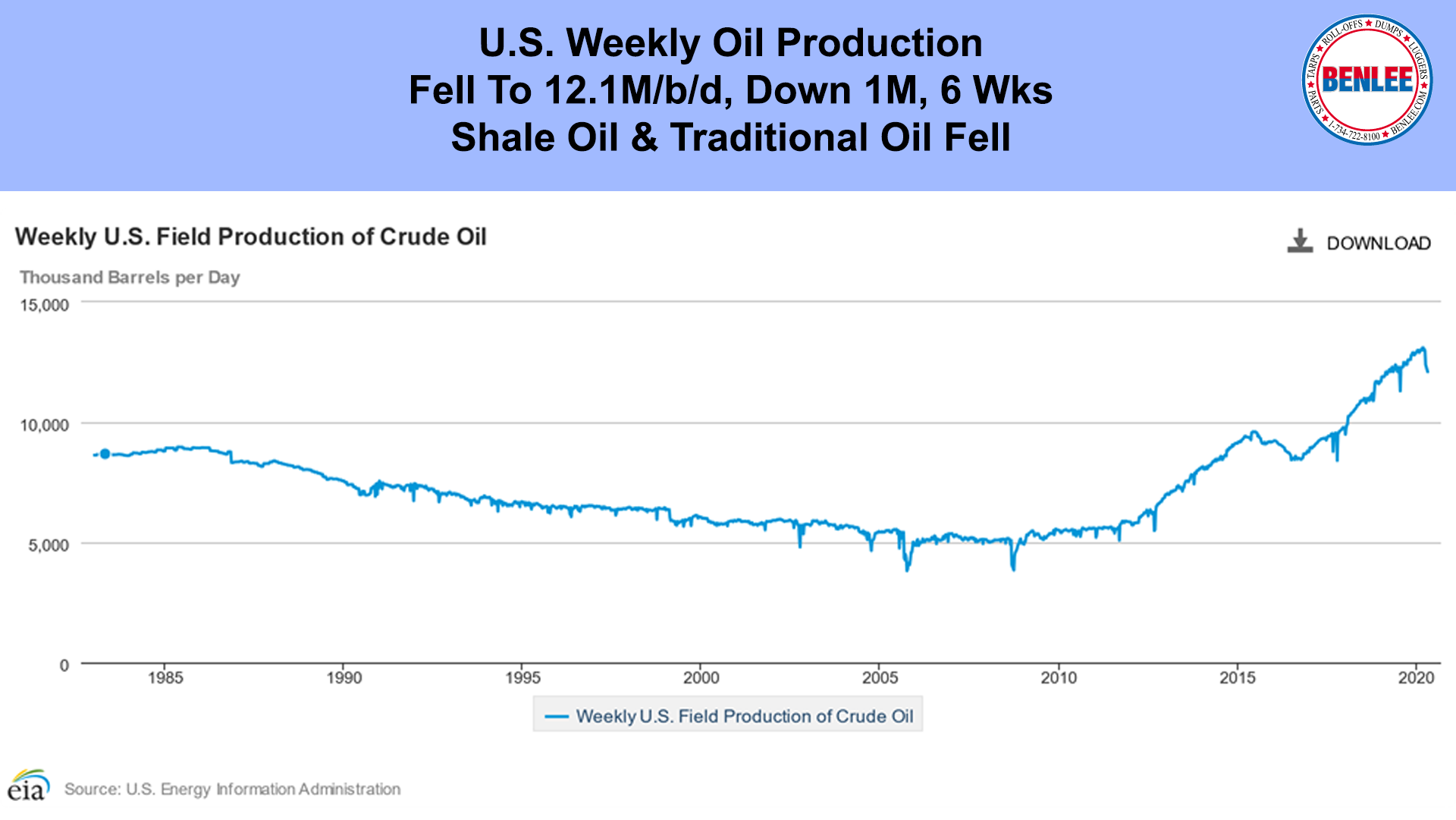

U.S. weekly oil production fell to 12.1M/b/d, down 1M/b/d in 6 weeks, as U.S. Shale oil and traditional oil fell.

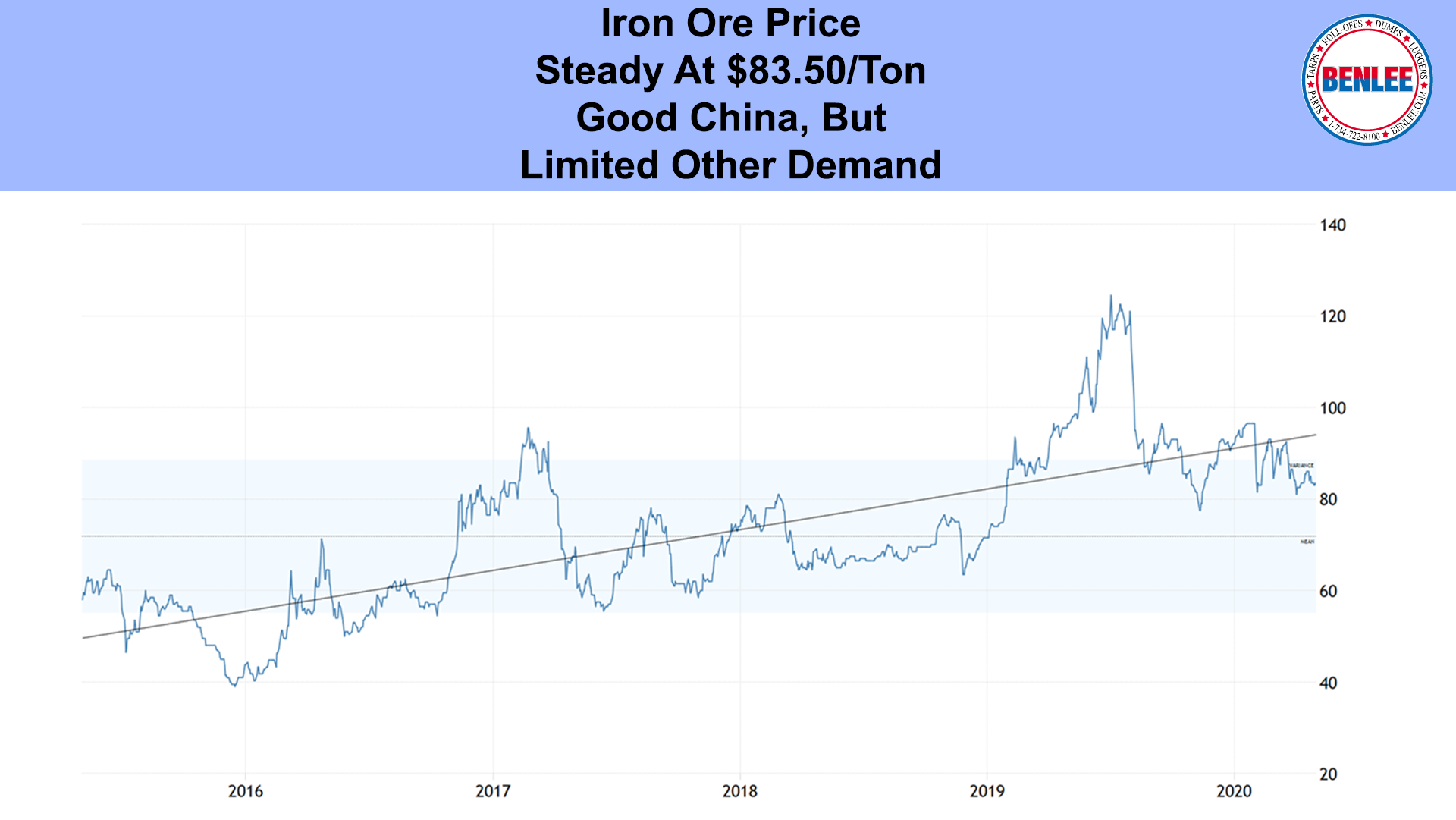

Iron ore was steady at $83.50/ton on good China, but limited other demand.

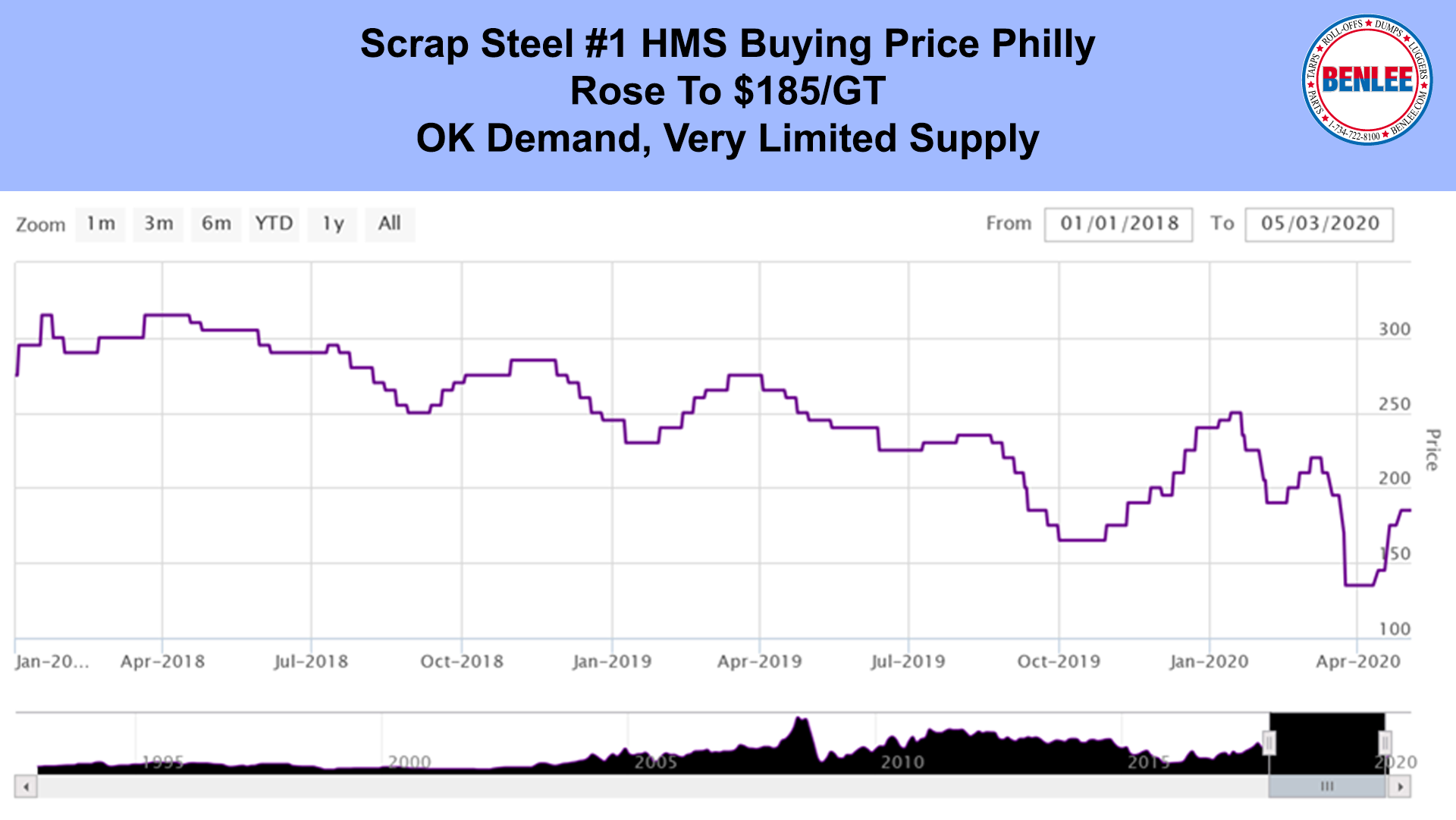

Scrap Steel No. 1 HMS export buying price Philadelphia rose to $185/GT on just OK demand, but very limited supply.

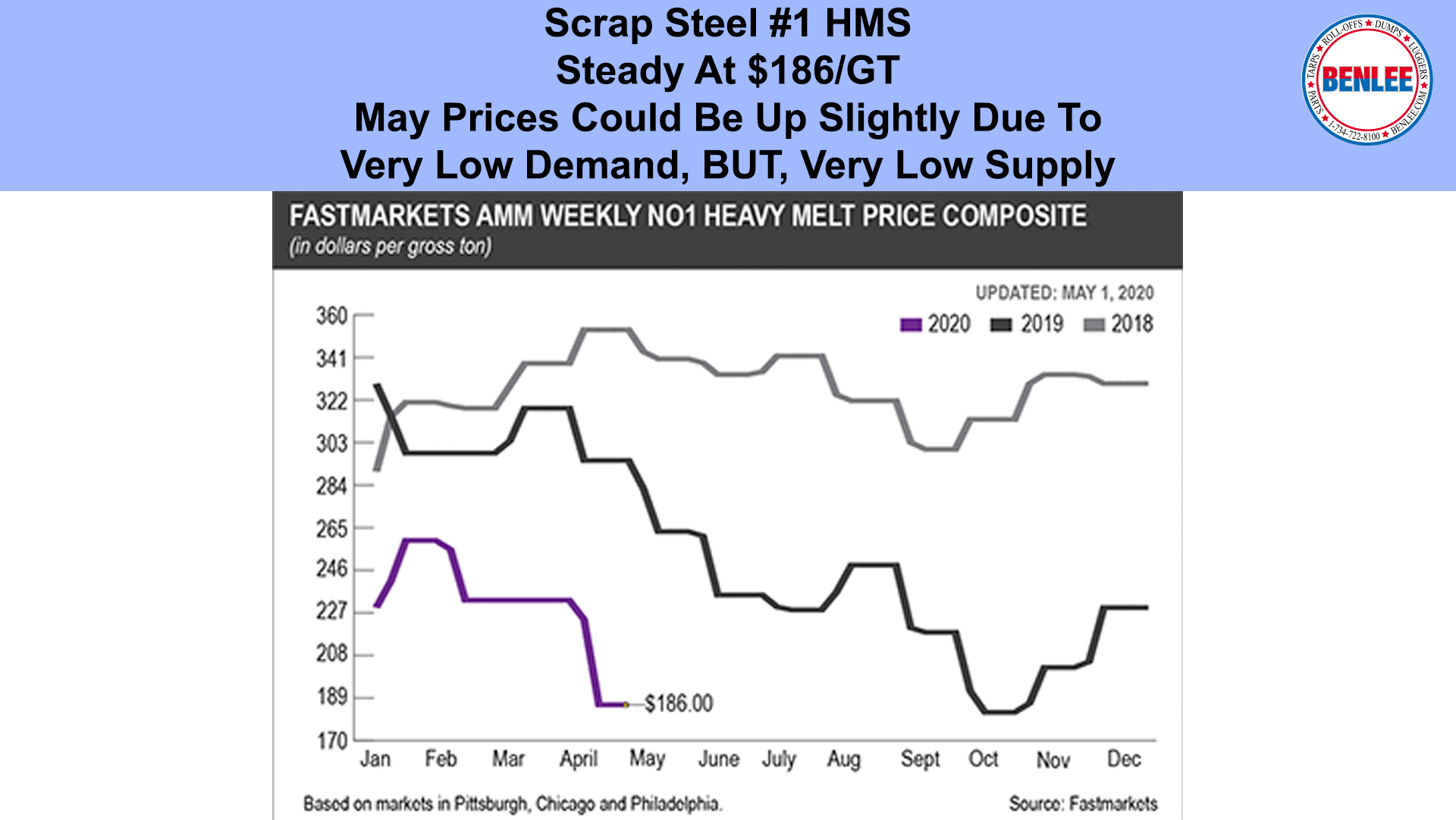

Scrap steel #1 HMS price was steady at $186/GT. May prices could up slightly, due to very low demand, BUT, very, low supply.

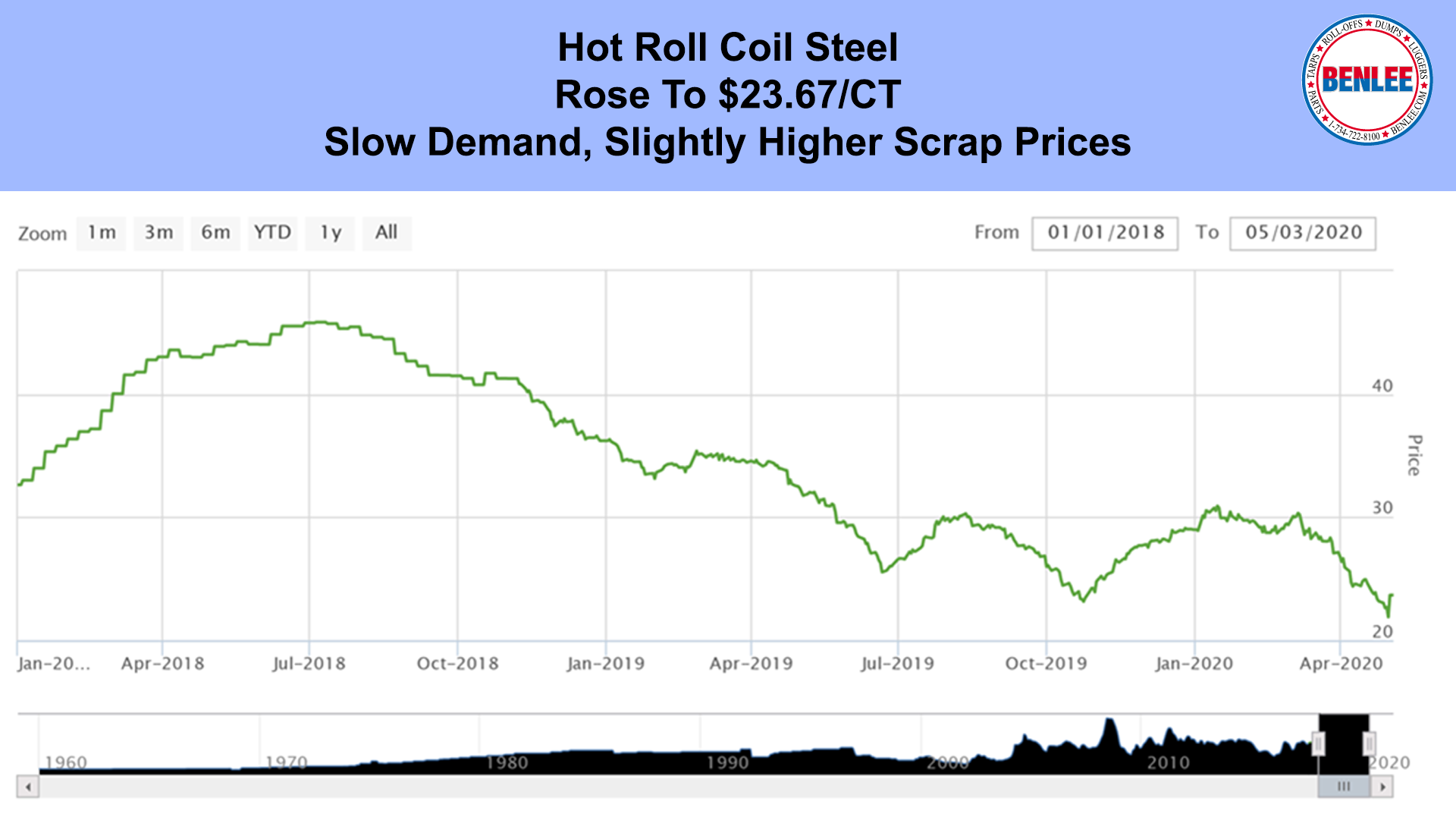

Hot Roll Coil steel rose to $23.67/Hundred on continued slow demand, but slightly higher scrap prices.

Copper fell to $2.31/lb., but off the low of about 6 weeks ago, which remains positive as China and parts of the U.S. open.

Aluminum fell to 65.4 cents per pound, on limited supply and demand.

April’s China Manufacturing index fell to 49.4, as COVID-10 hurt domestic and Chinese demand. New export orders fell the most since December 2008. The loss of jobs accelerated.

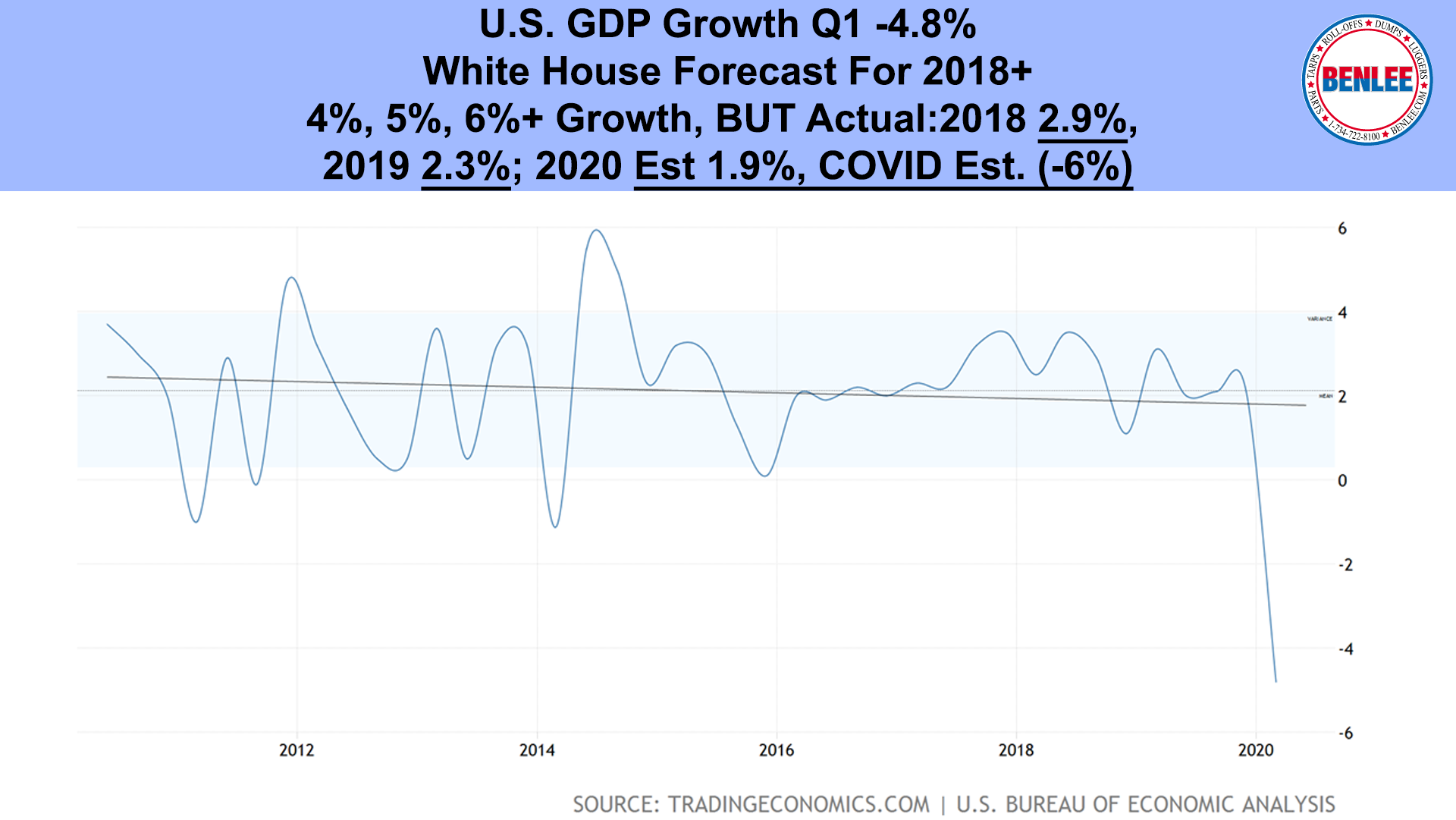

U.S. GDP for the first quarter ending March was negative 4.8%. The White House forecast for 2018 and out years was 4%, 5% and 6% growth or more. Actual 2018 was 2.9%, not 4%, 2019 slowed to 2.3%, not grew to 5% and pre COVID, the 2020 was forecast by most was to slow to 1.9%, not grow to 6% or more. Due to COVID, 2020 could be -6% or worse.

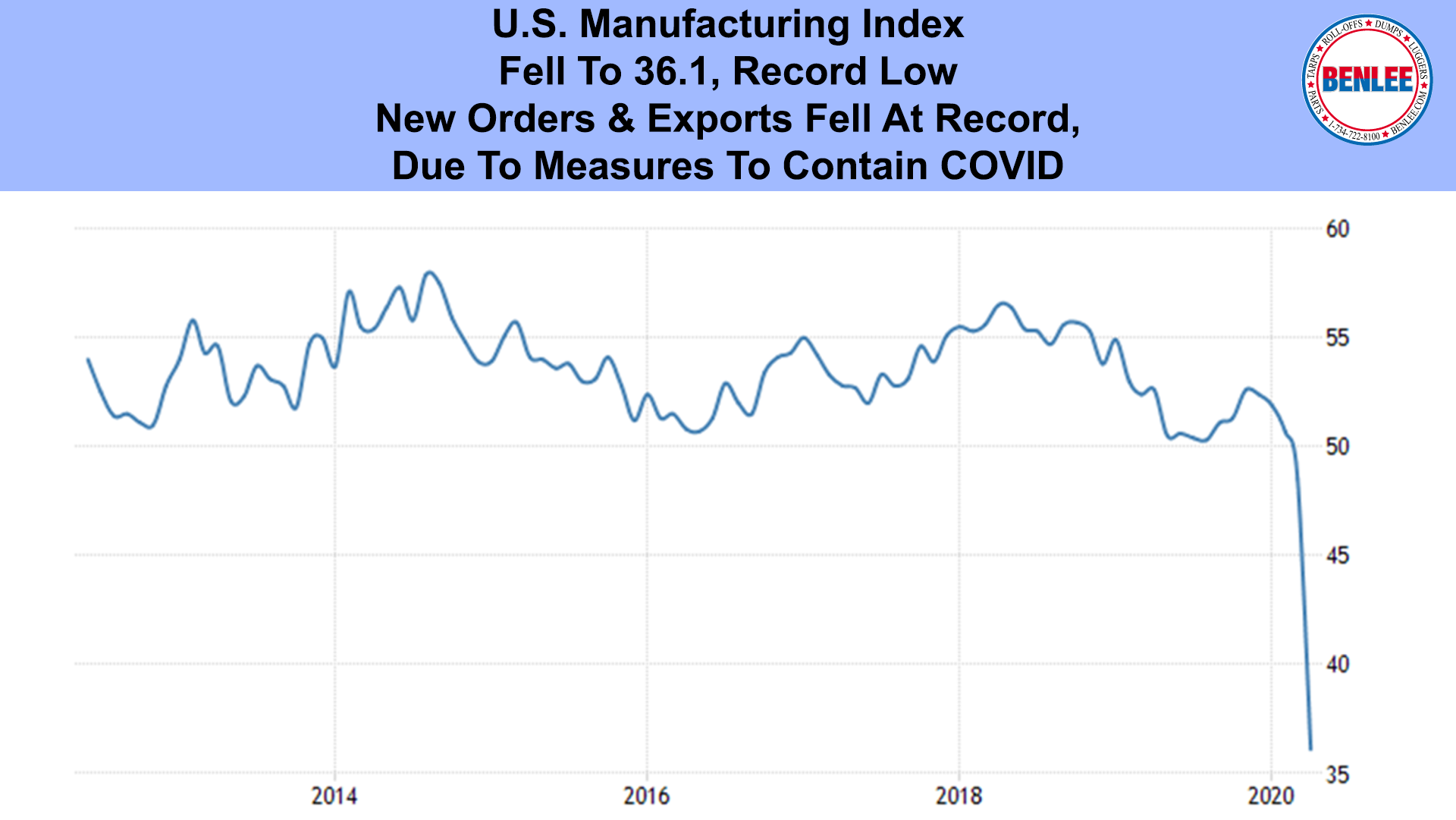

April’s U.S. Manufacturing index was revised lower to 36.1, a record low. New orders and exports fell at record rates due to measures to contain COVID.

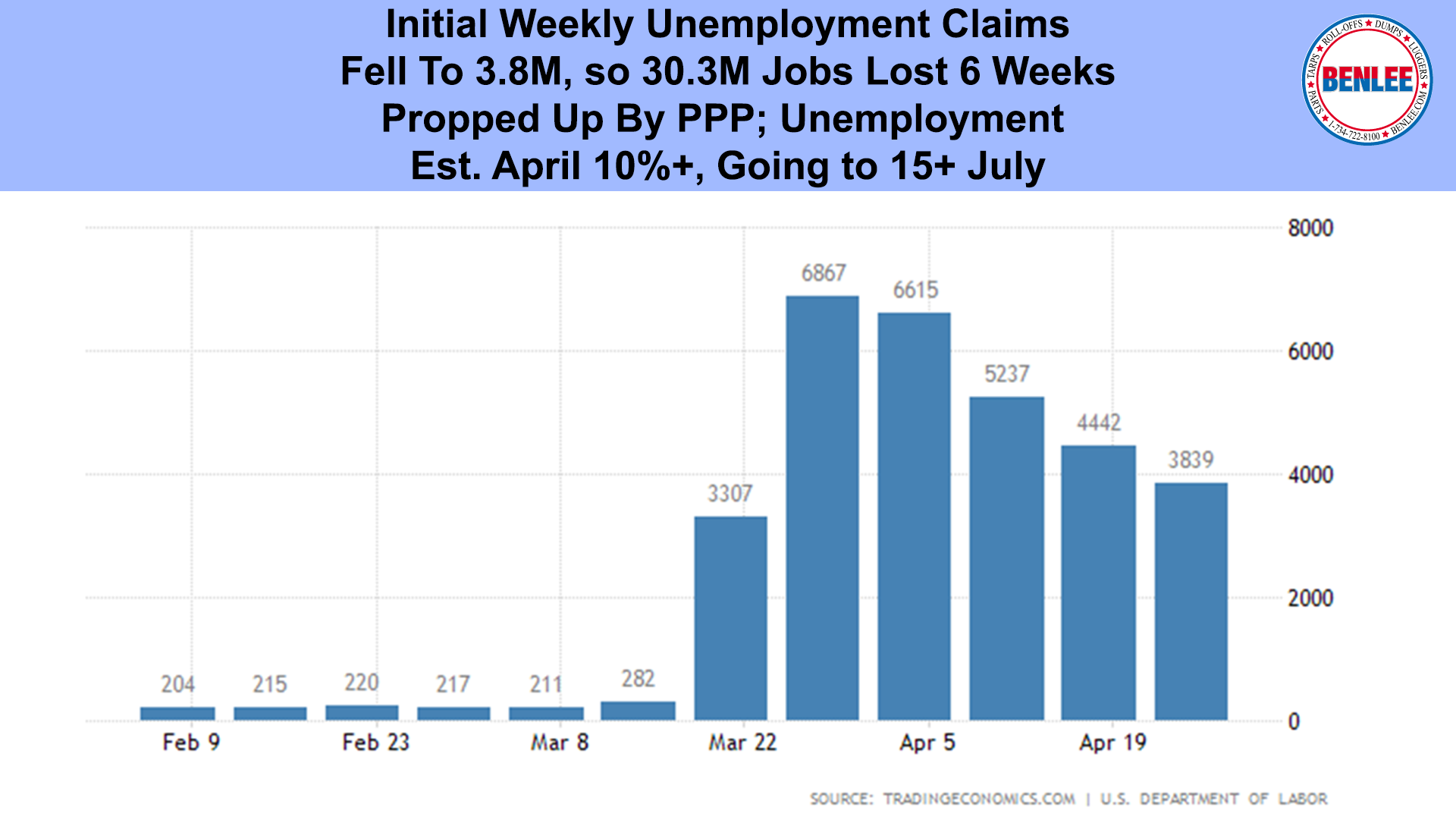

Initial U.S. Weekly Unemployment Claims fell to 3.8M, so 30.3M jobs have been lost in 6 weeks. This is a horrific number that is actually being propped up by the PPP, the Payroll protection program. Unemployment percent April is estimated to be 10% plus, going to 15% plus July.

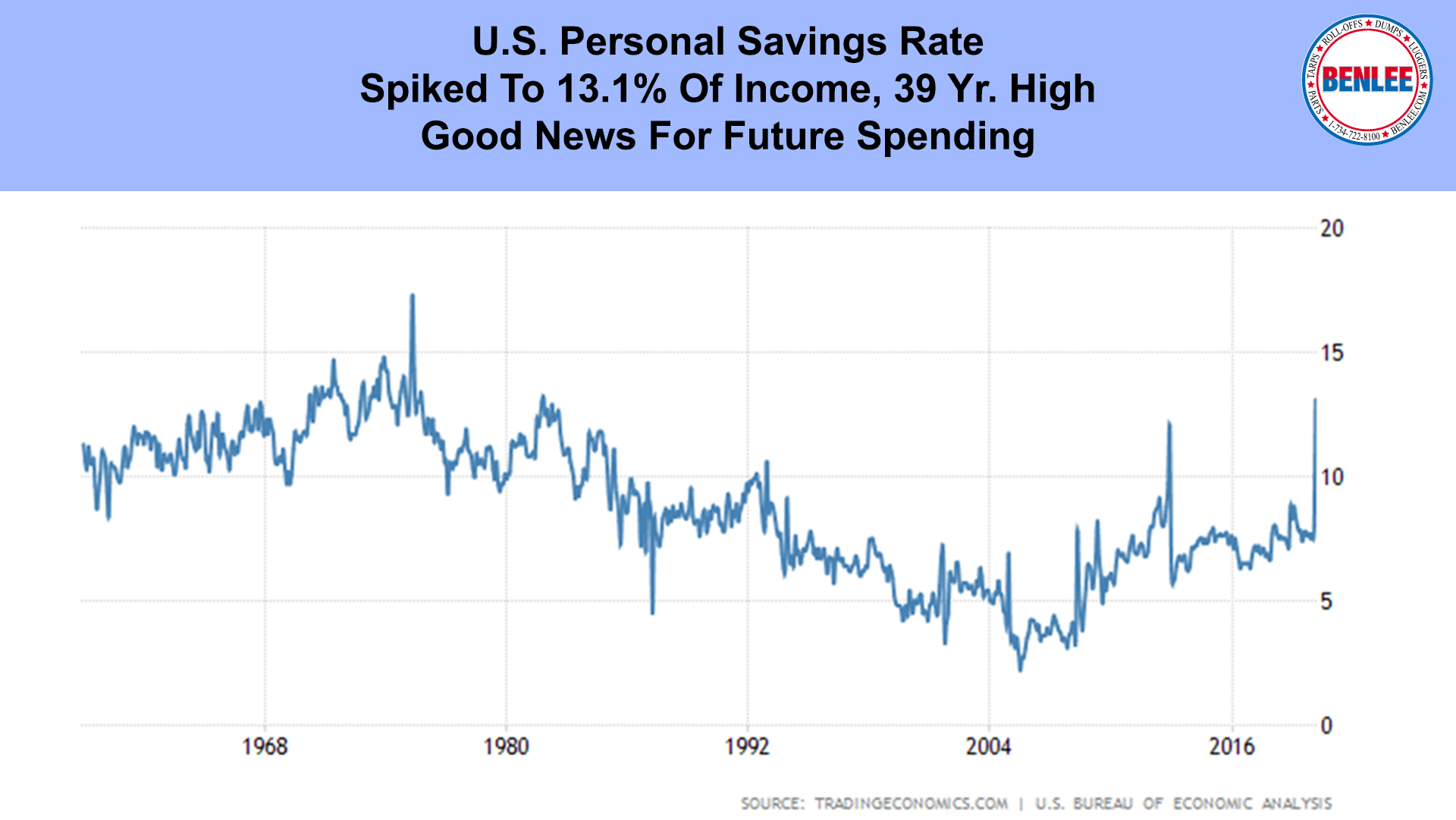

March’s U.S. Personal savings rate spiked to 13.1% a 39-year high, as people stayed home and couldn’t spend. Good news for future spending.

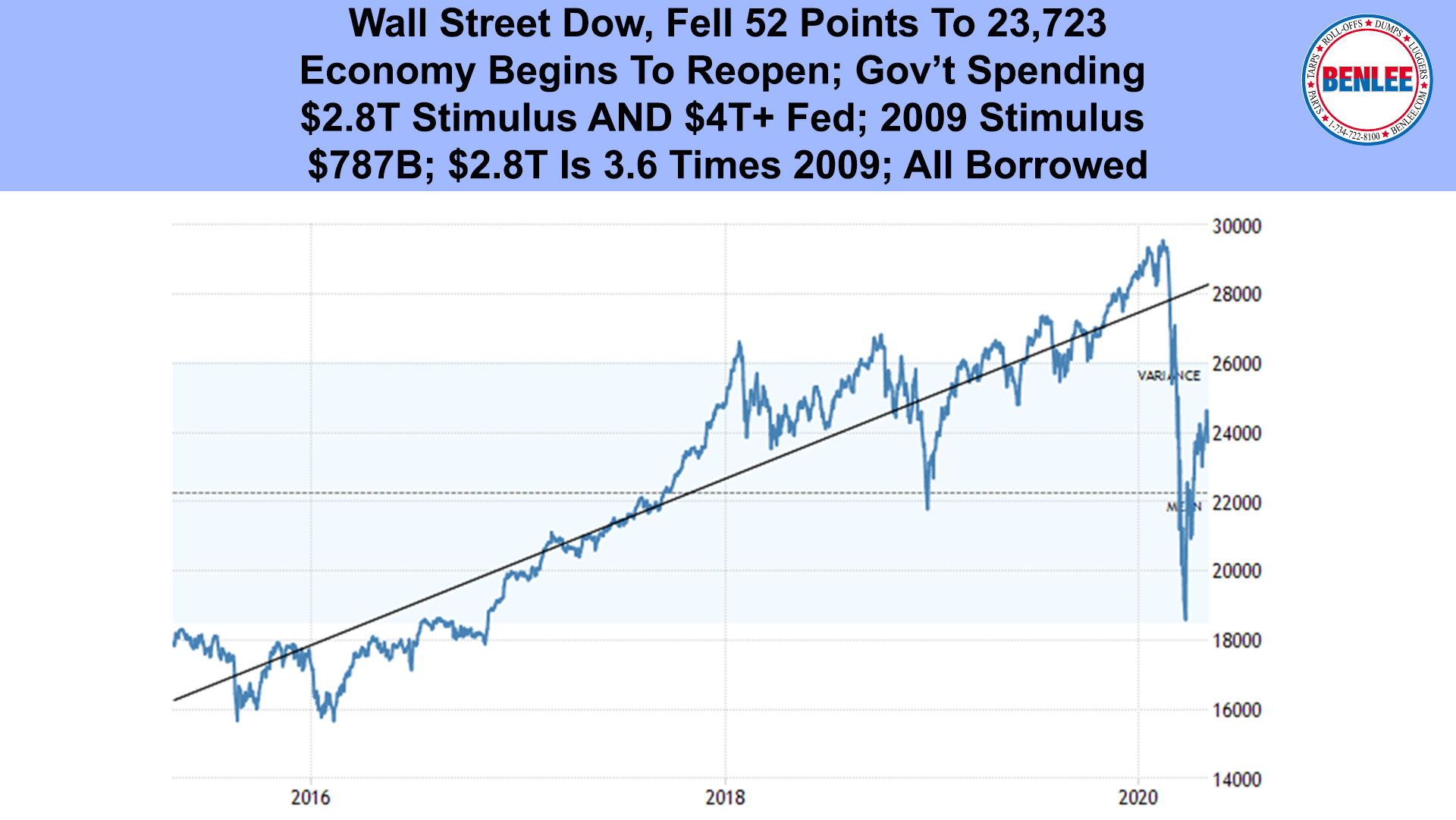

Wall Street’s Dow Jones fell 52 points to 23,723 as the economy begins to reopen. The U.S. government is spending about $2.8 Trillion of stimulus, combined with $4Trillion+ of Federal Reserve buying. As a comparison the 2009 Stimulus was $787Billion, so the $2.8T is 3.6 Times 2009. Note this is ALL Borrowed money. Nothing is free.

Member

Member