Loading price data

This is the Global Economic, Commodities, Scrap Metal and Recycling Report, by our BENLEE Roll off Trailer and Lugger Truck, May 3rd, 2021.

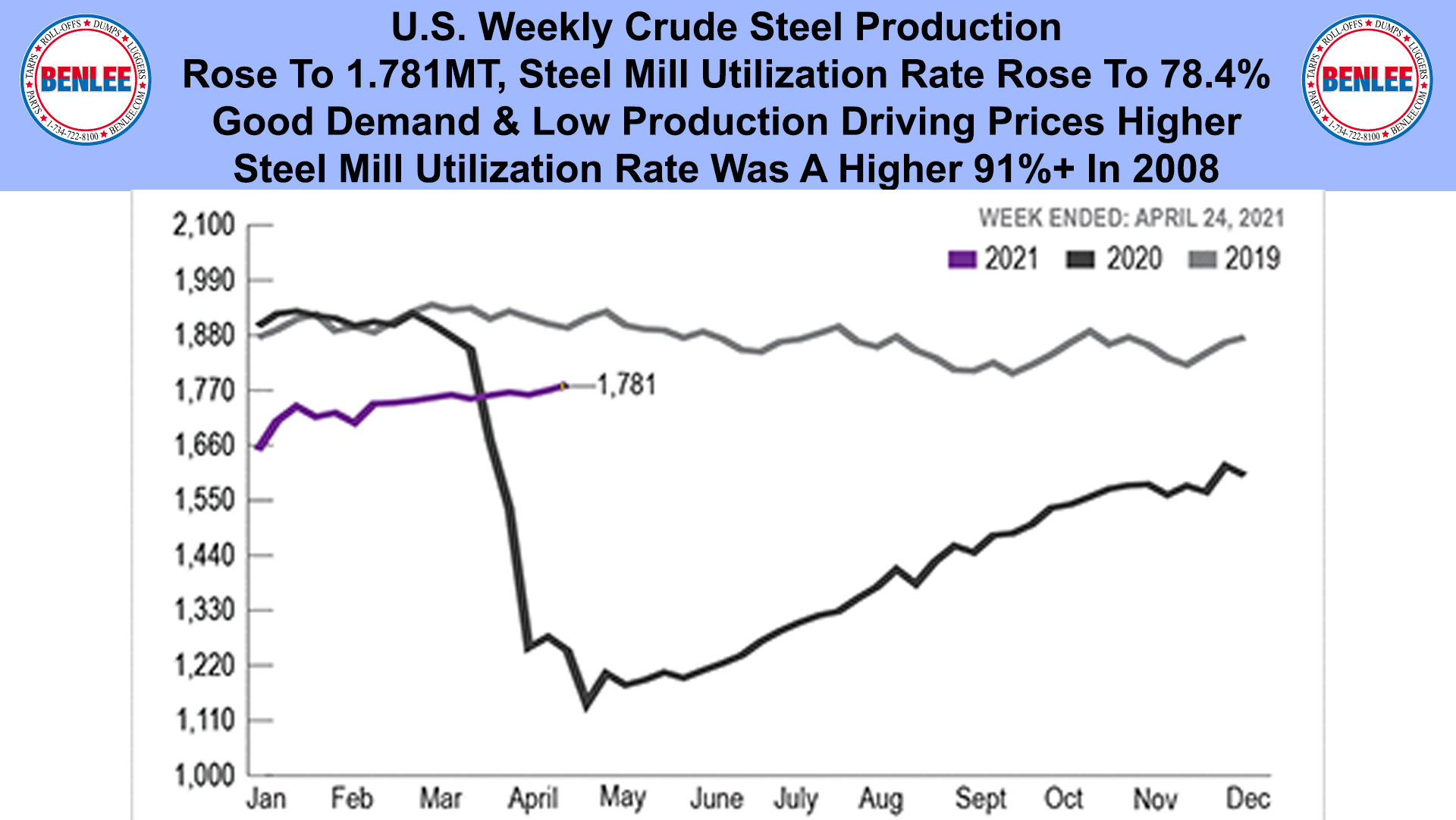

U.S. Weekly crude steel production rose to 1.781MT, as the steel mill utilization rose to 78.4%. Good demand and low production is driving prices higher. The steel mill utilization rate was a high 91% plus in 2008.

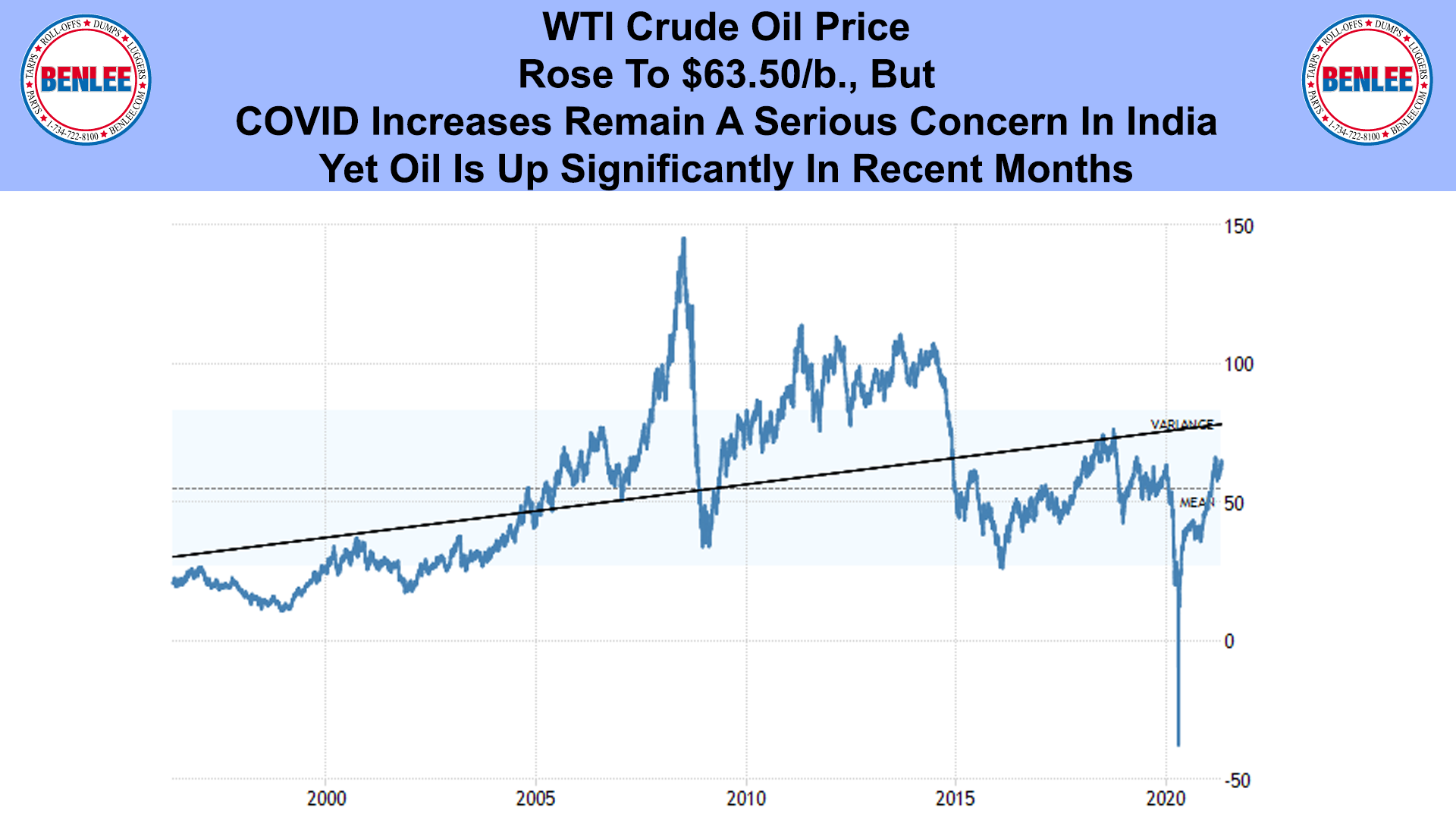

WTI Crude oil price rose to $63.50/b., but COVID increases remain a serious concern in India, yet oil is up significantly in recent months.

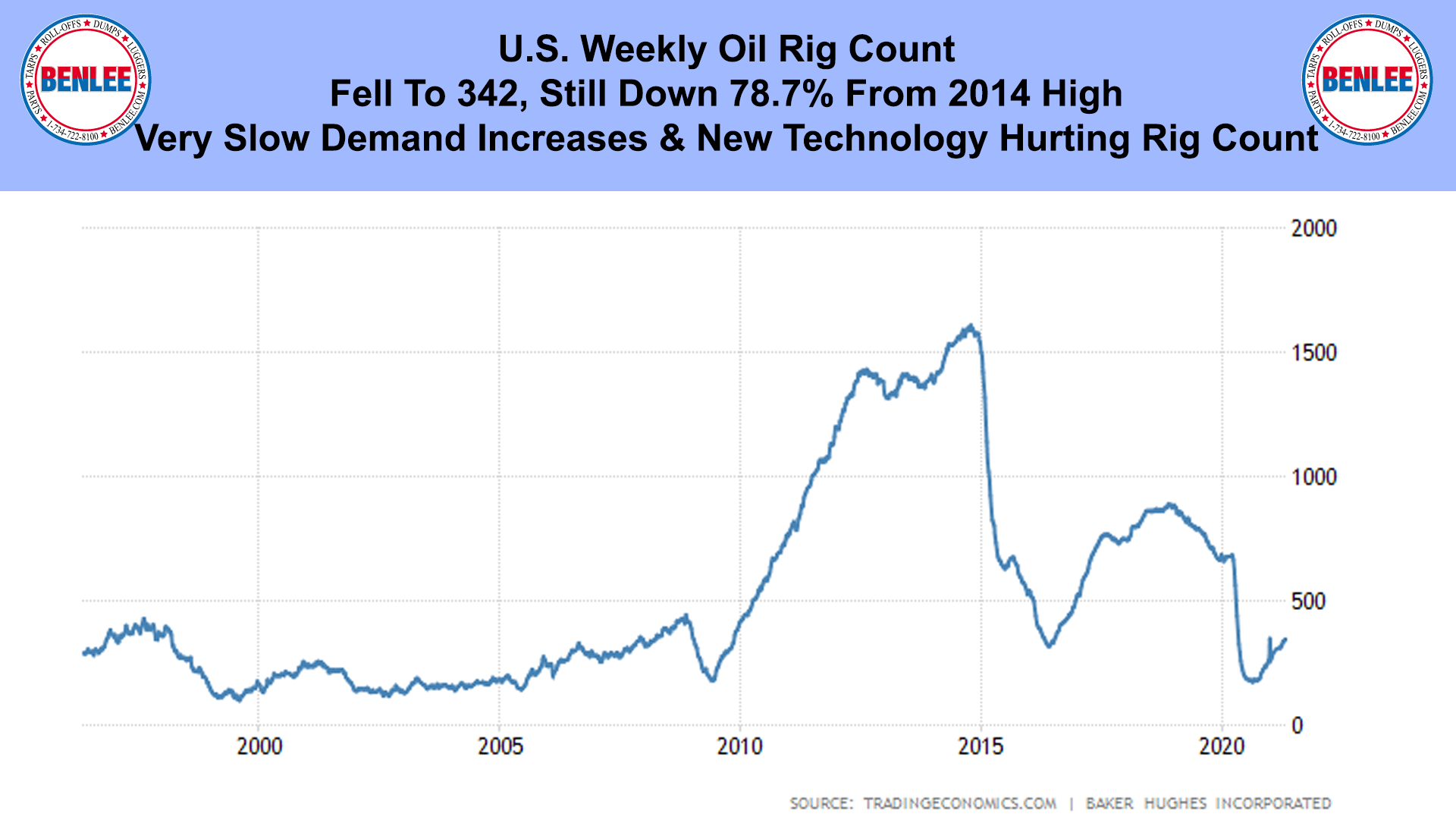

The U.S. Weekly Oil rig count fell to 342 still down 78.7% from 2014’s high on very slow demand increases and new technology hurting the rig count.

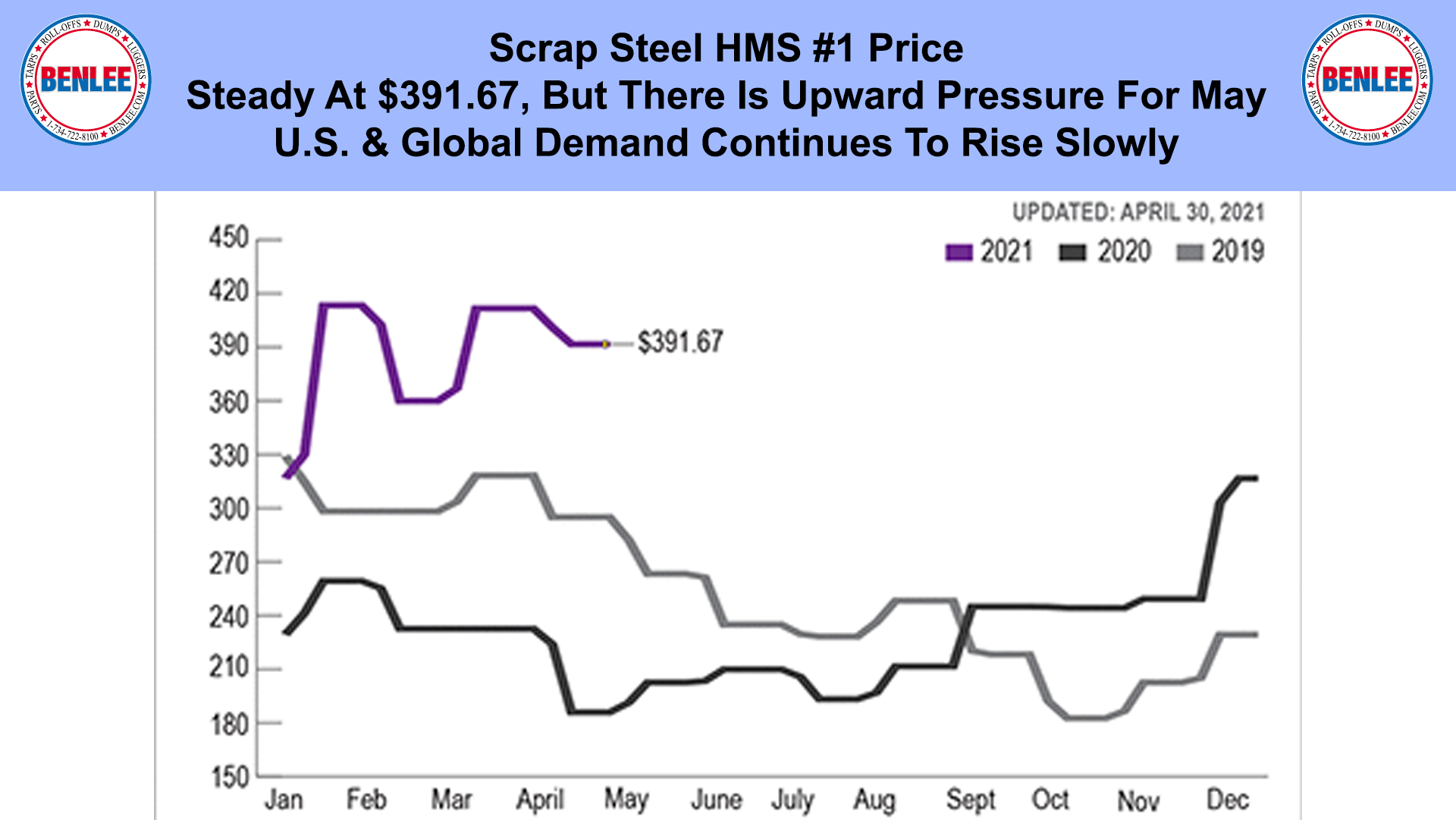

Scrap steel #1 HMS was steady at $391.67/GT, but there is upward price pressure for May. U.S. and global demand continue to rise slowly.

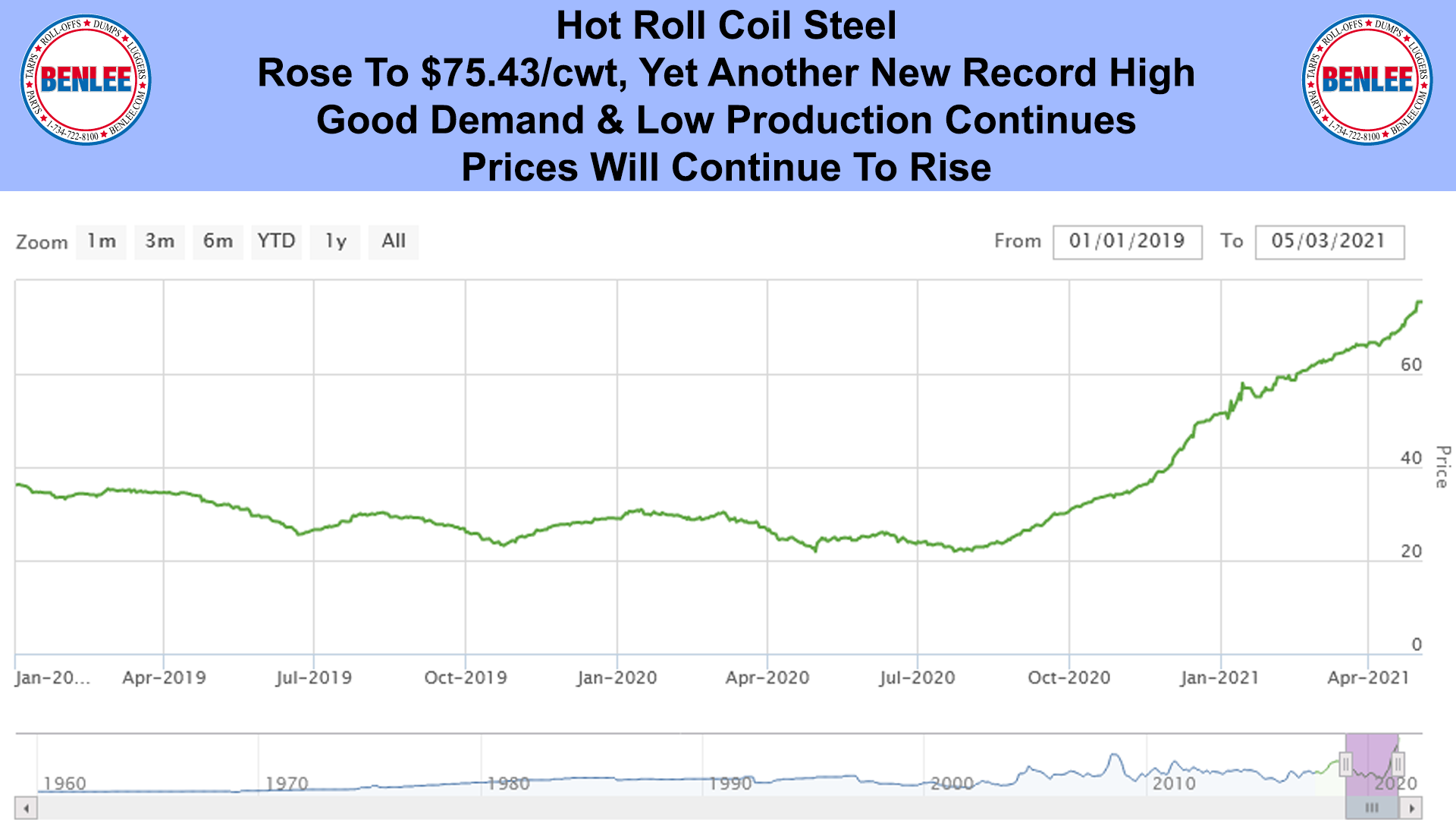

Hot roll coil steel rose to $75.43/cwt, yet another record high. Good demand and low production continue. Prices will continue to rise.

Copper price rose to $4.46/lb., a 10 year high on the hopes of robust economic growth. Growth may be driven by the multi trillion-dollar U.S. Jobs and Family plans.

Aluminum price rose to $1.10/lb. a multiyear high on strong Chinese demand in Automobile and construction. Supply has been hurt by China shutting down 34 alloy plants to limit emissions.

China April Caxin Manufacturing PMI Index rose to 51.9, a 4-month high. Sentiment remained upbeat with incredibly strong exports to the U.S. U.S. consumers are spending stimulus money on Chinese made goods.

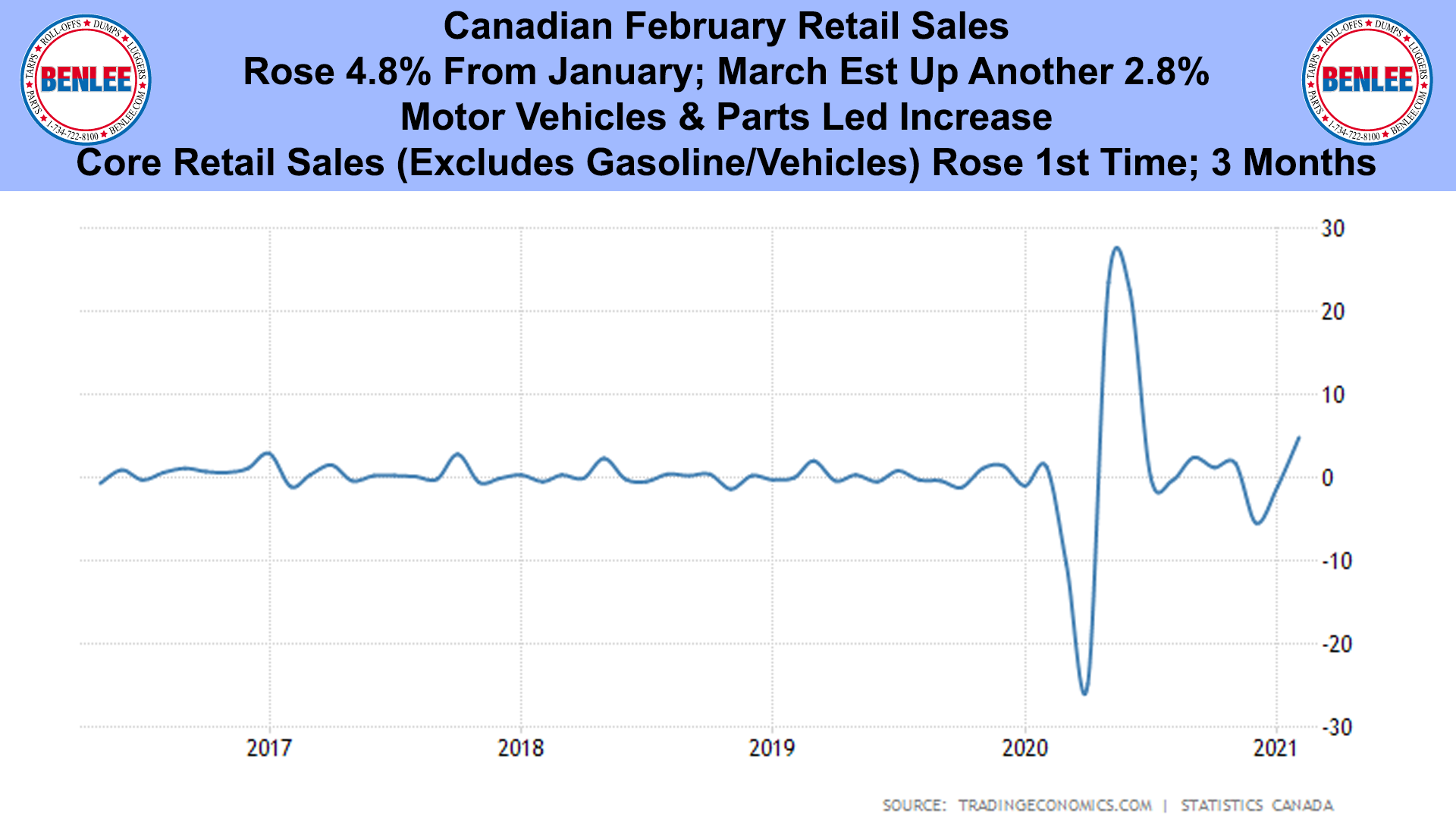

Canadian February Retail sales rose 4.8% from January with March estimated up another 2.8%. Motor vehicles and parts led the increase. Core retail sales, which excluded gasoline and vehicles, rose for the 1st time in 3 months.

U.S. Federal Reserve Rate, held steady at 0 to .25% and the Fed will continue to purchase $120B/month of Bonds. Bond purchases increase the money supply, keeping interest rates low. The Federal Reserve believes the increasing inflation will be temporary.

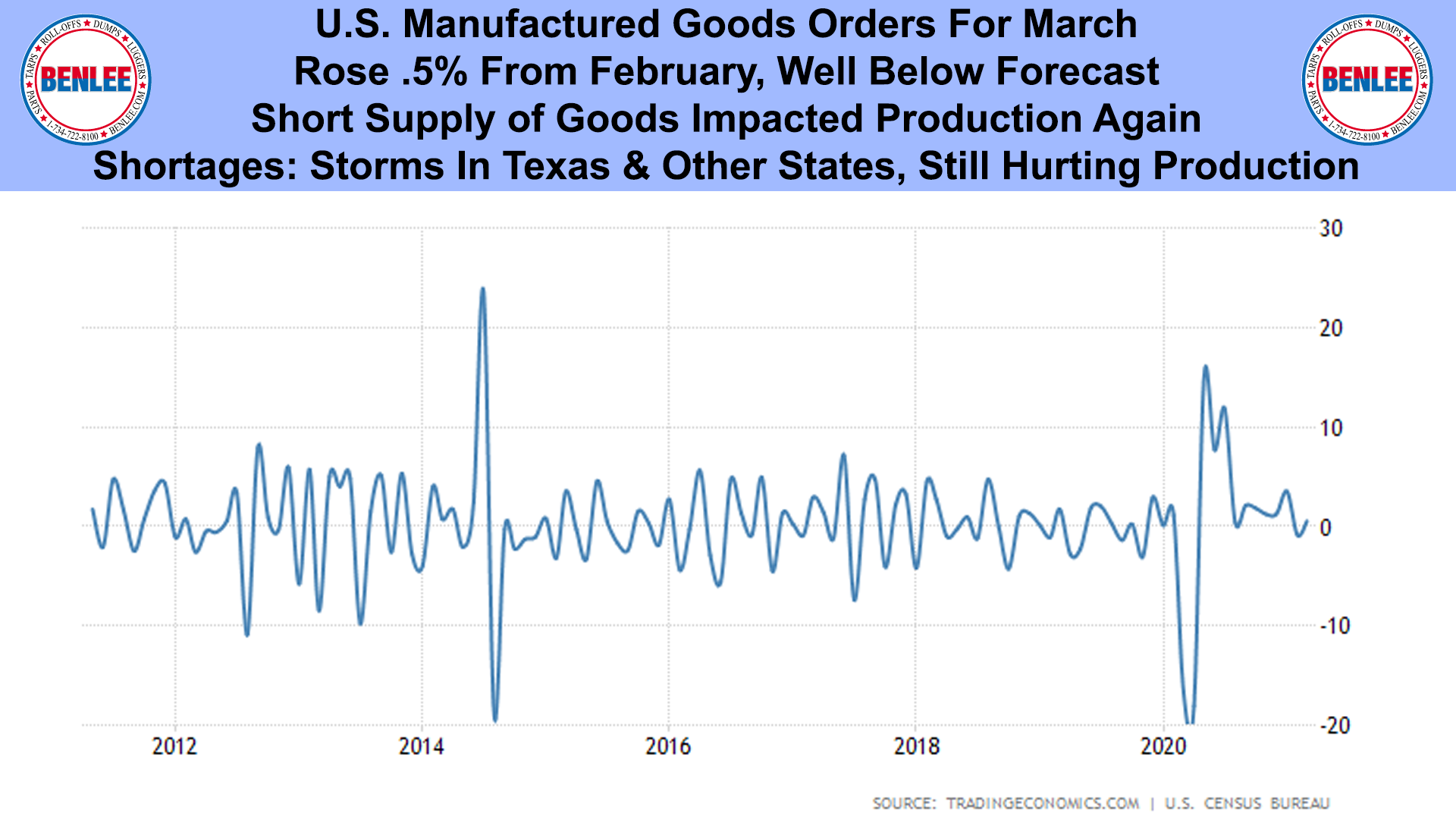

U.S. Manufactured goods Orders for March, rose .5% from February, well below forecast. Short supply of goods impacted production again. Shortages due to storms in Texas & other states are still hurting production.

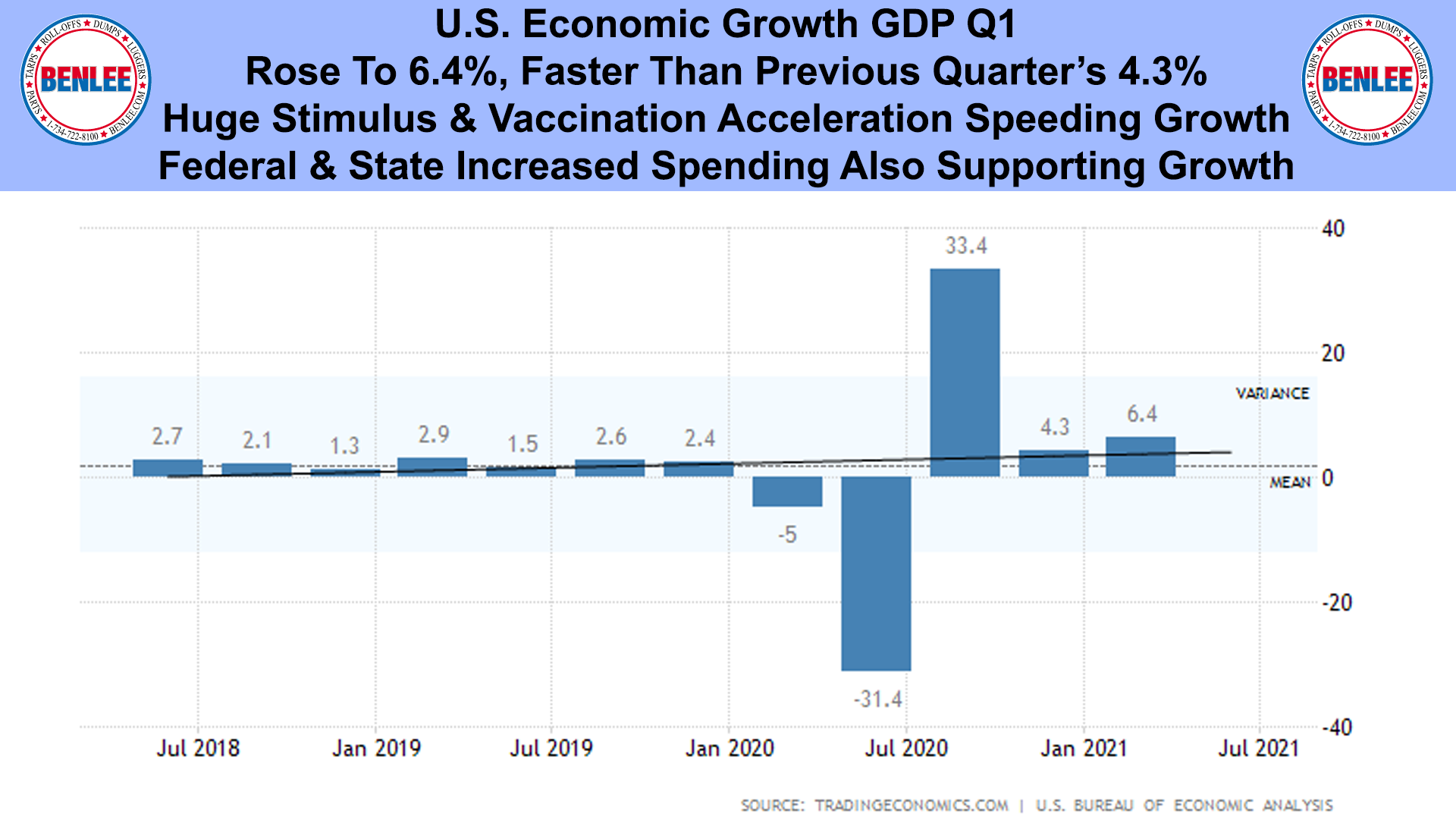

U.S. Economic growth, GDP for Q1, rose 6.4%, faster than the previous quarter’s 4.3%. Huge stimulus and vaccine acceleration is speeding growth. Federal and State increased spending is also supporting growth.

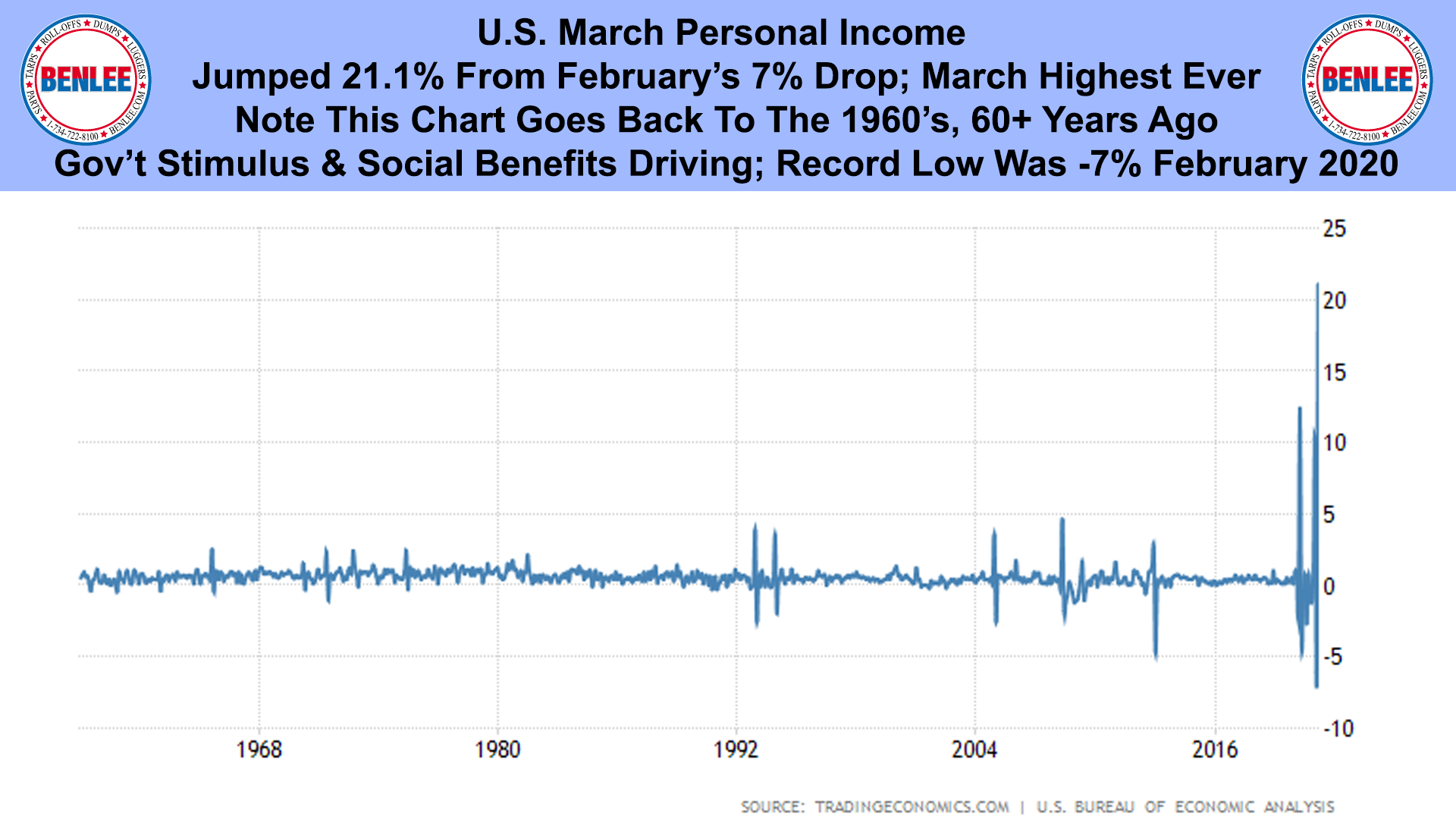

U.S. March Personal Income, jumped 21.1% from February’s 7% drop. March was the highest ever. This chart does back to the1960’s, 60+years ago. Government stimulus and social benefits are driving growth. The record low was -7% in February 2020.

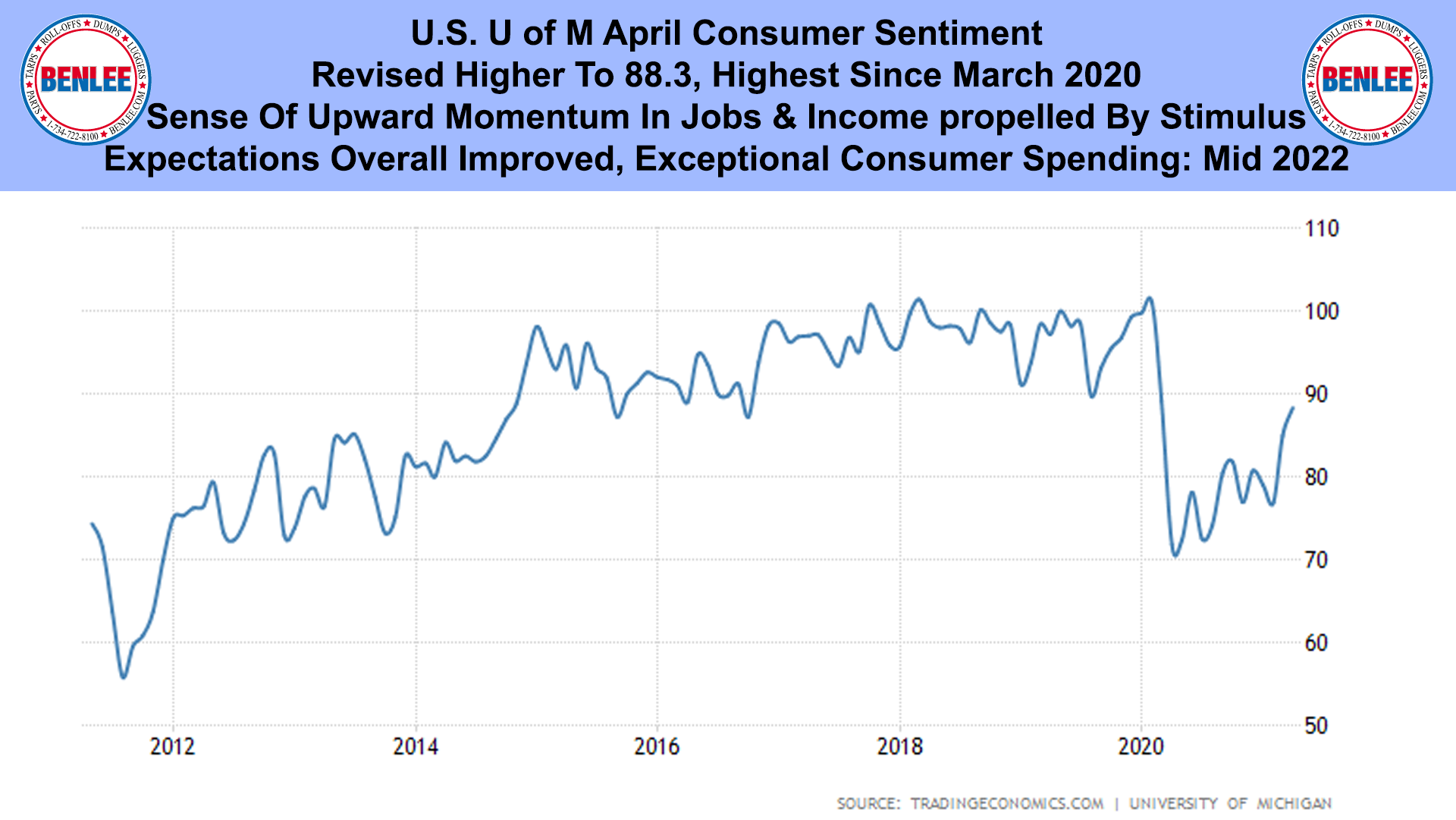

U.S. U of M April Consumer Sentiment was revised higher to 88.3 the highest since March 2020. There was a sense of upward momentum in jobs and income propelled by stimulus. Expectations overall improved and there is expected to be exceptional consumer spending until mid-2022.

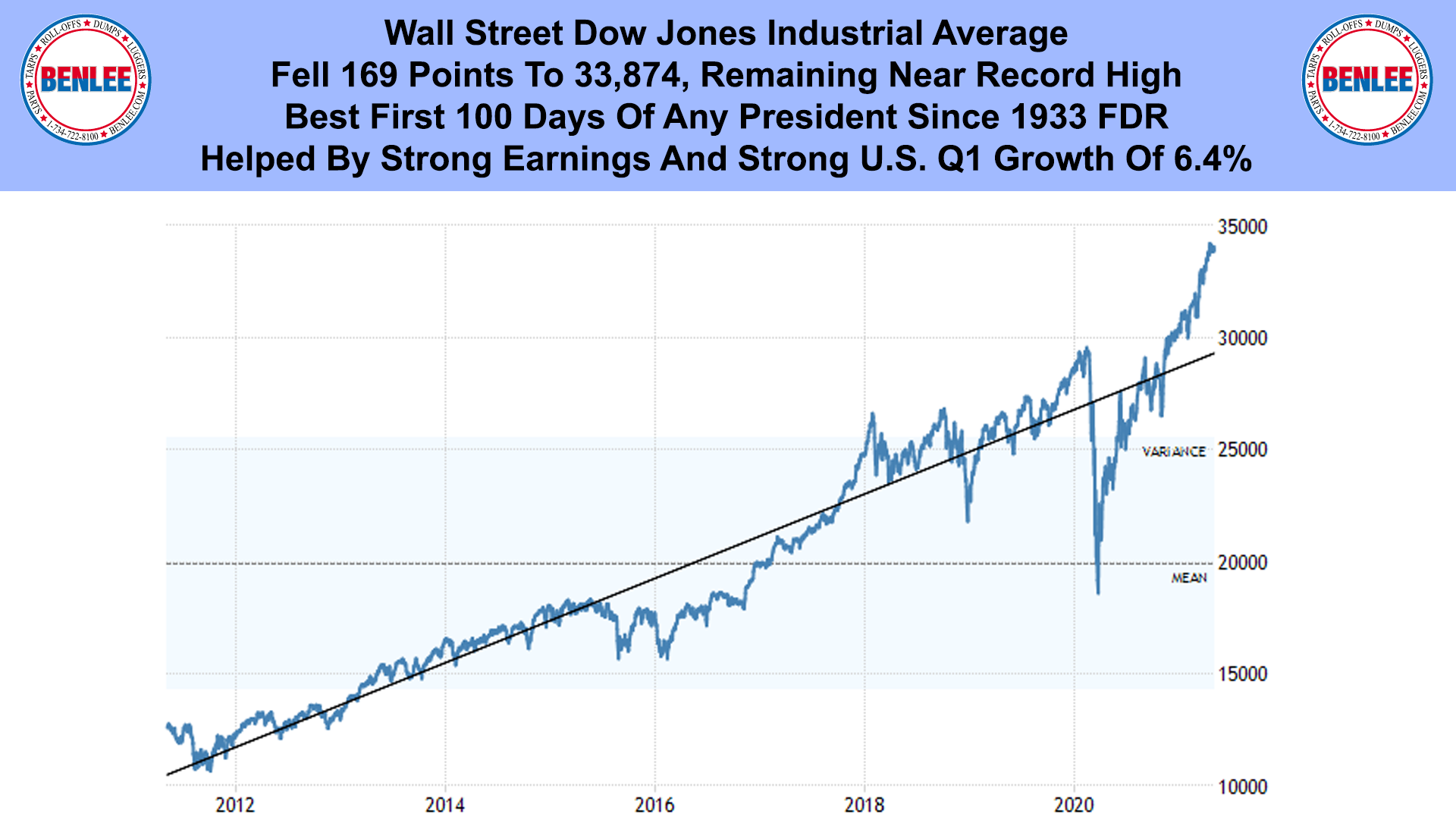

Wall Street’s Dow Jones Industrial Average fell 169 points to 33,874, remaining near the record high. It was the best first 100 days of any President since 1933 when FDR was President, helped by strong earnings and strong U.S. Q1 Growth of 6.4%.

Member

Member