Loading price data

This is the Global Economic, Commodities, Scrap Metal and Recycling Report, by our BENLEE Roll off Trailer and Lugger Truck, June 28th, 2021.

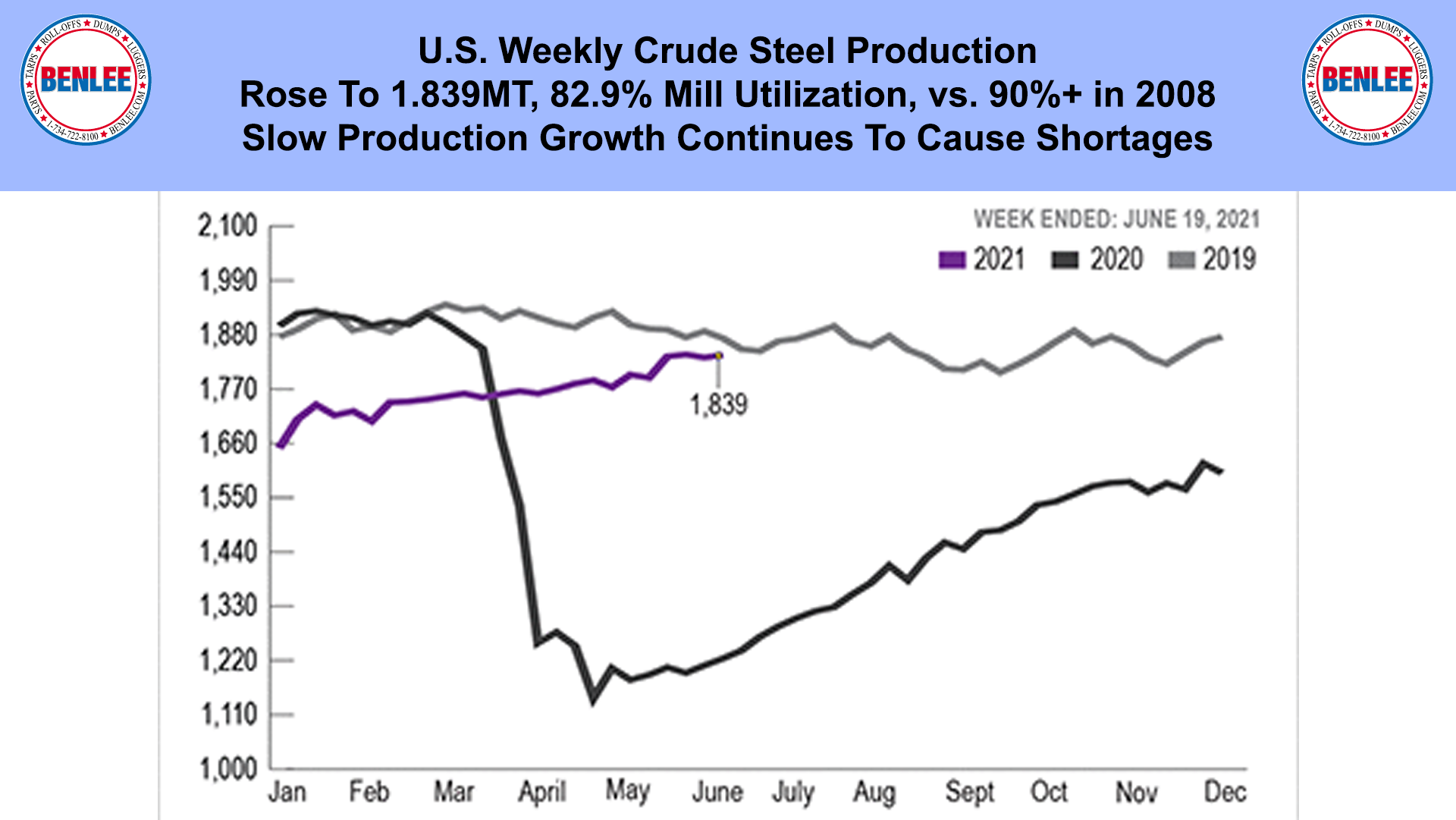

U.S. Weekly crude steel production rose to 1.839MT, an 82.9% steel mill utilization rate vs. 90%+ in 2008. Slow production growth, continues to cause shortages.

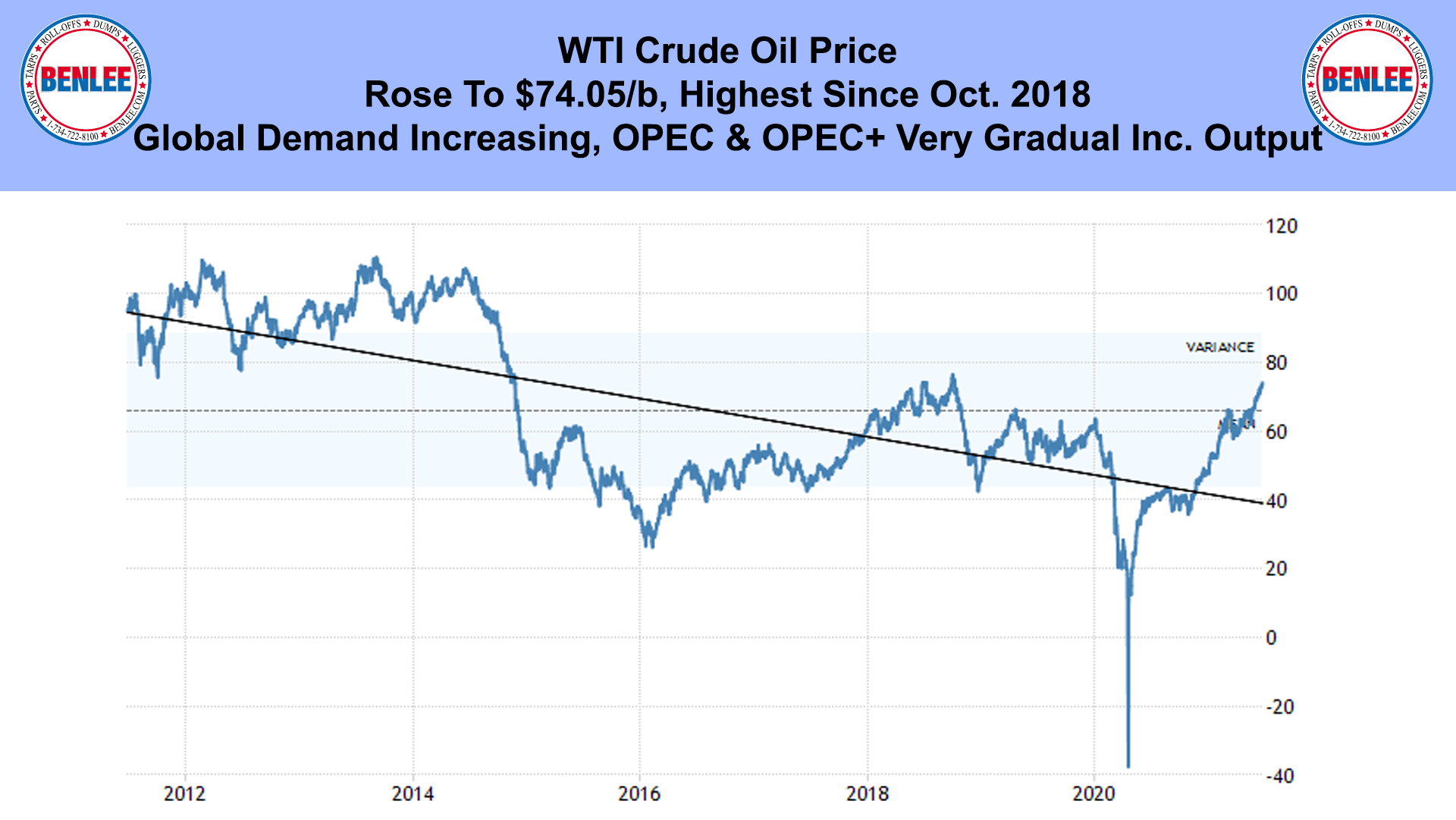

WTI Crude oil price rose to $74.05/b, the highest since October 2018. Global demand is increasing, as OPEC and OPEC+ very gradually increase output.

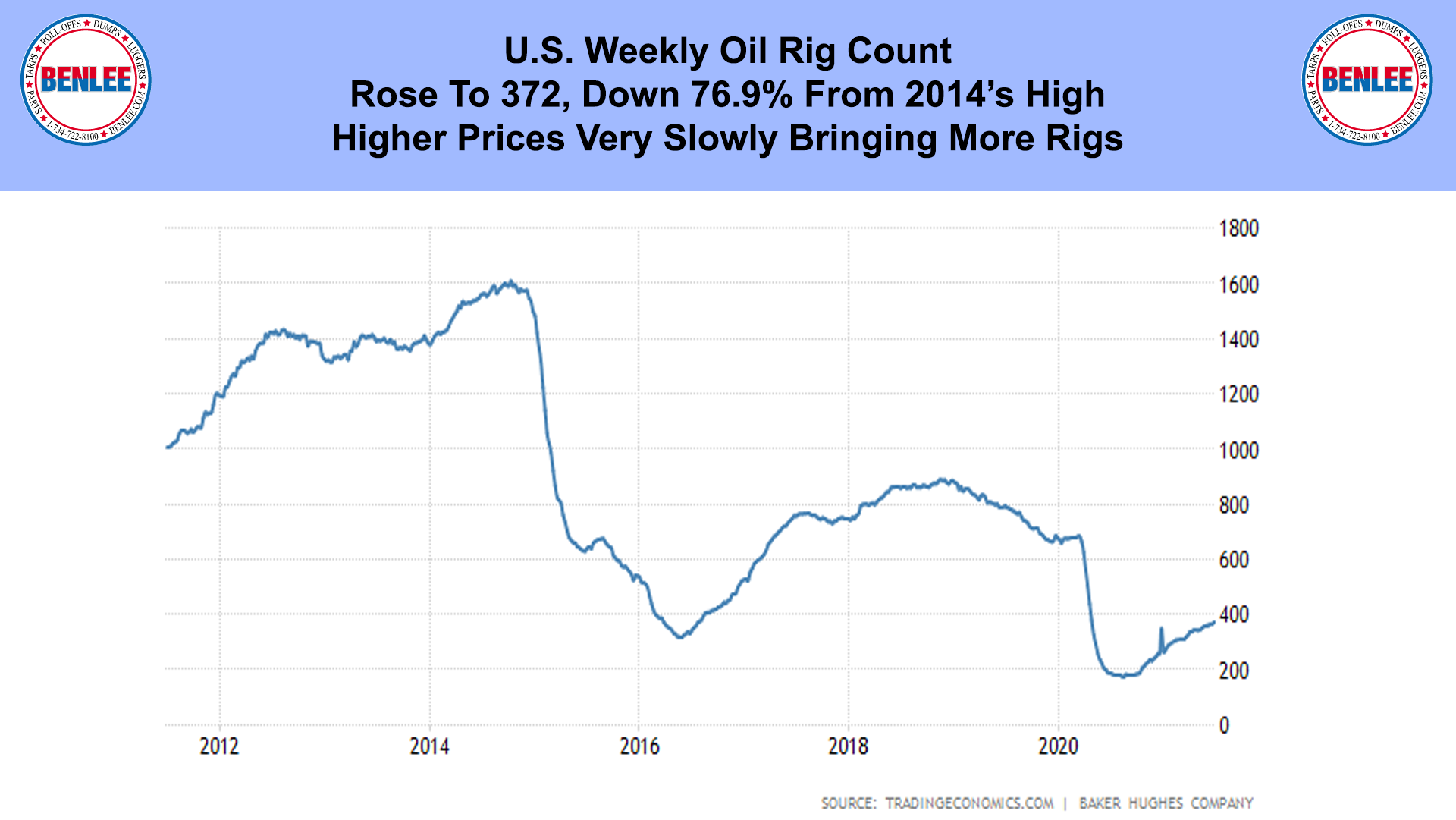

The U.S. Weekly Oil rig count rose to 372, down 76.9% from 2014’s high. Higher prices are slowly bringing more rigs.

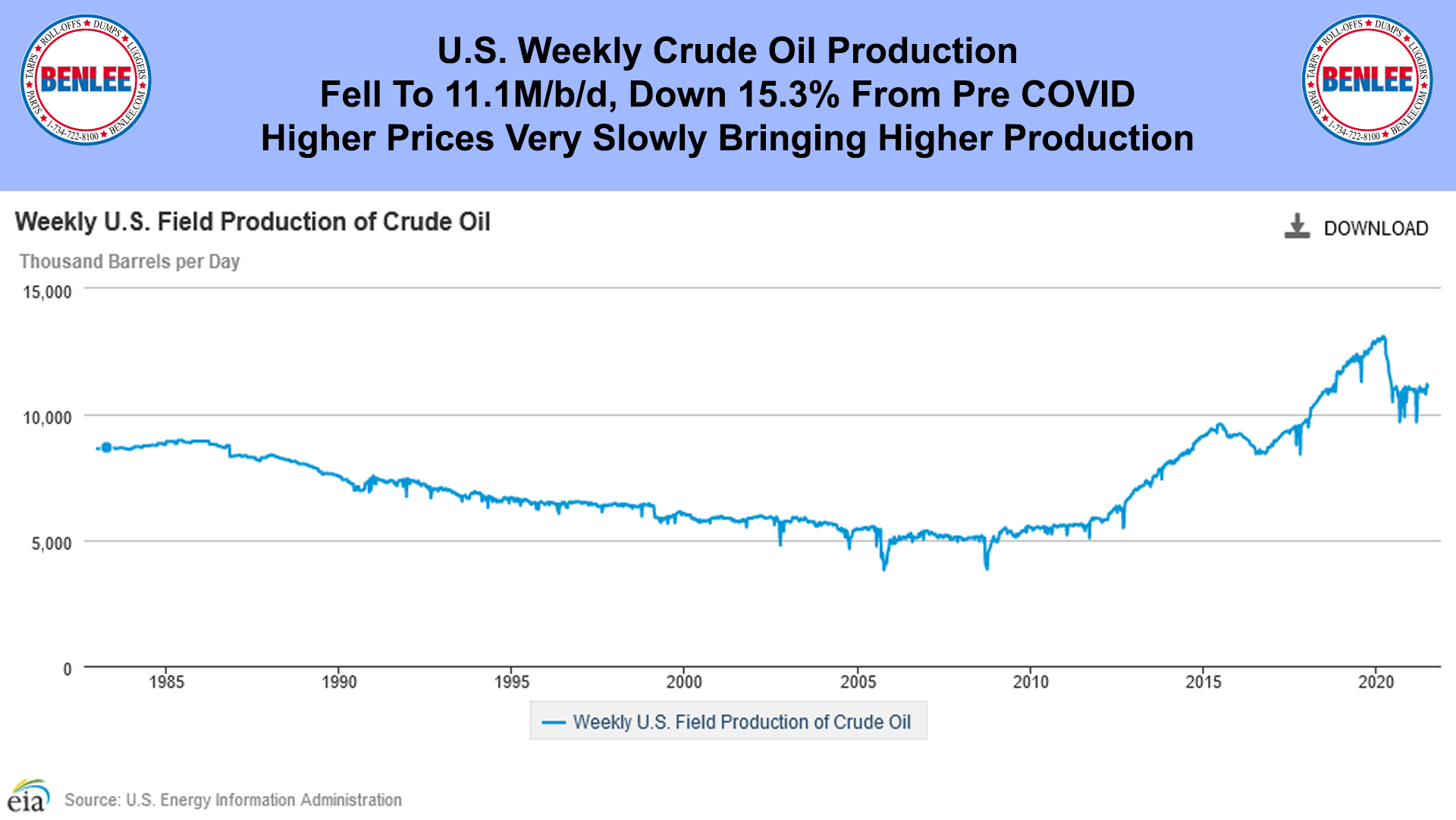

U.S. weekly crude oil production fell to 11.1M/b/d, down 15.3% from Pre COVID. Higher prices are very slowing bringing higher production.

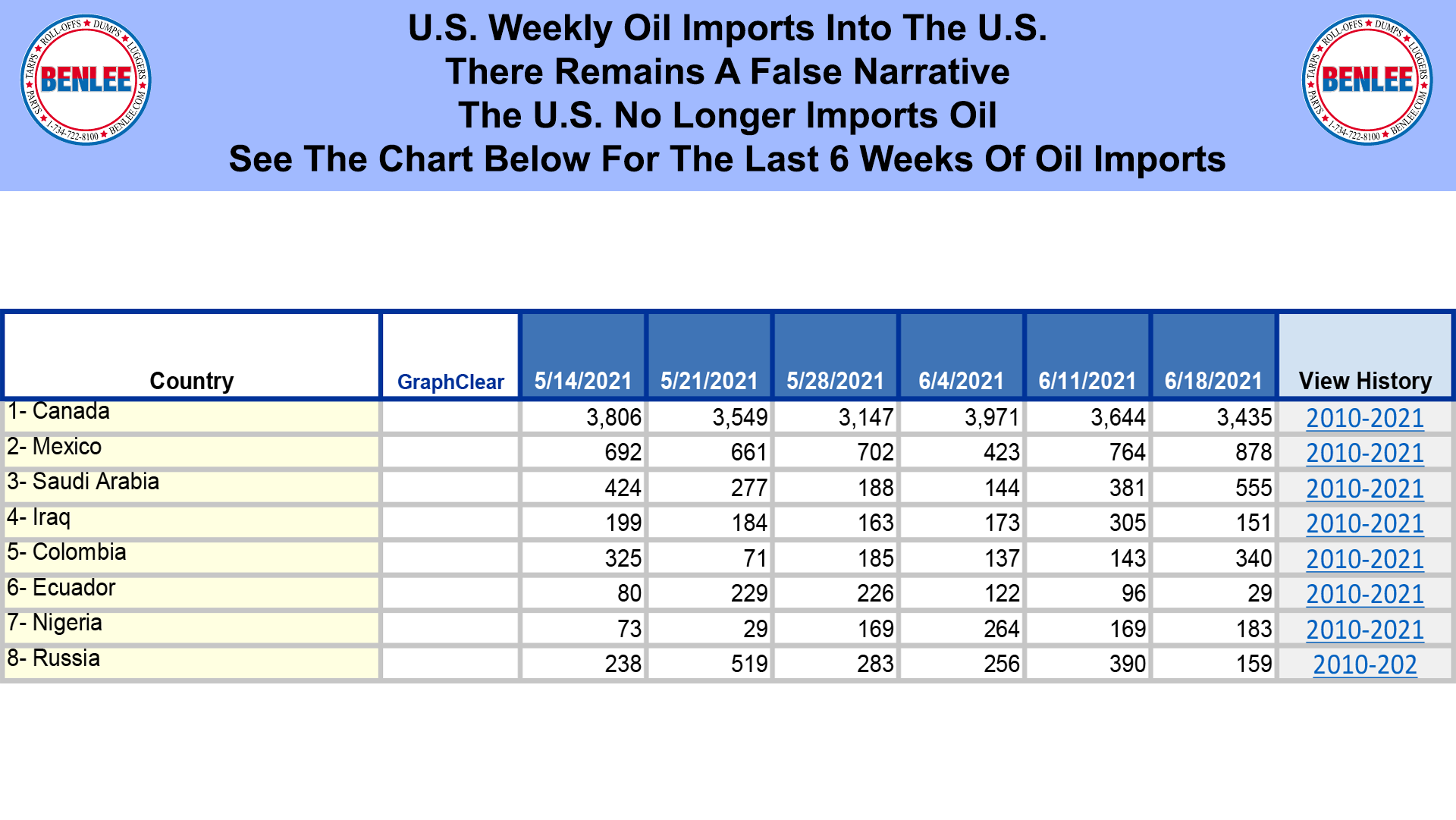

U.S. Weekly Oil Imports. There remains a false narrative that the U.S. no longer imports oil. See the chart below for the last 6 weeks of oil imports. They come from Canada, Mexico, Saudi Arabia, Iraq, Columbia, Equator, Nigeria and yes, even from Russia.

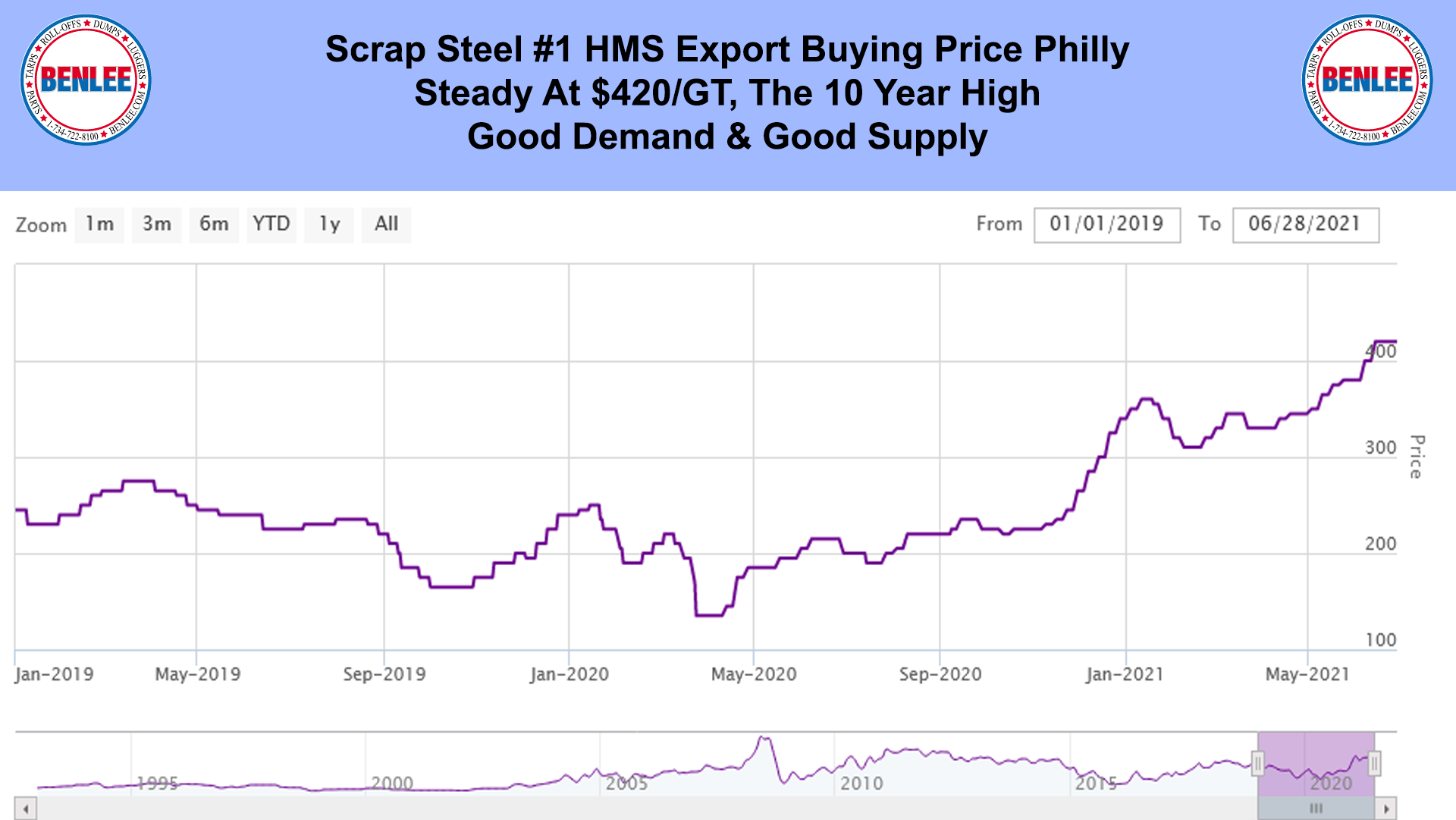

Scrap steel #1 HMS export buying price Philly, was steady at $420/GT, the 10 year high on good demand and good supply.

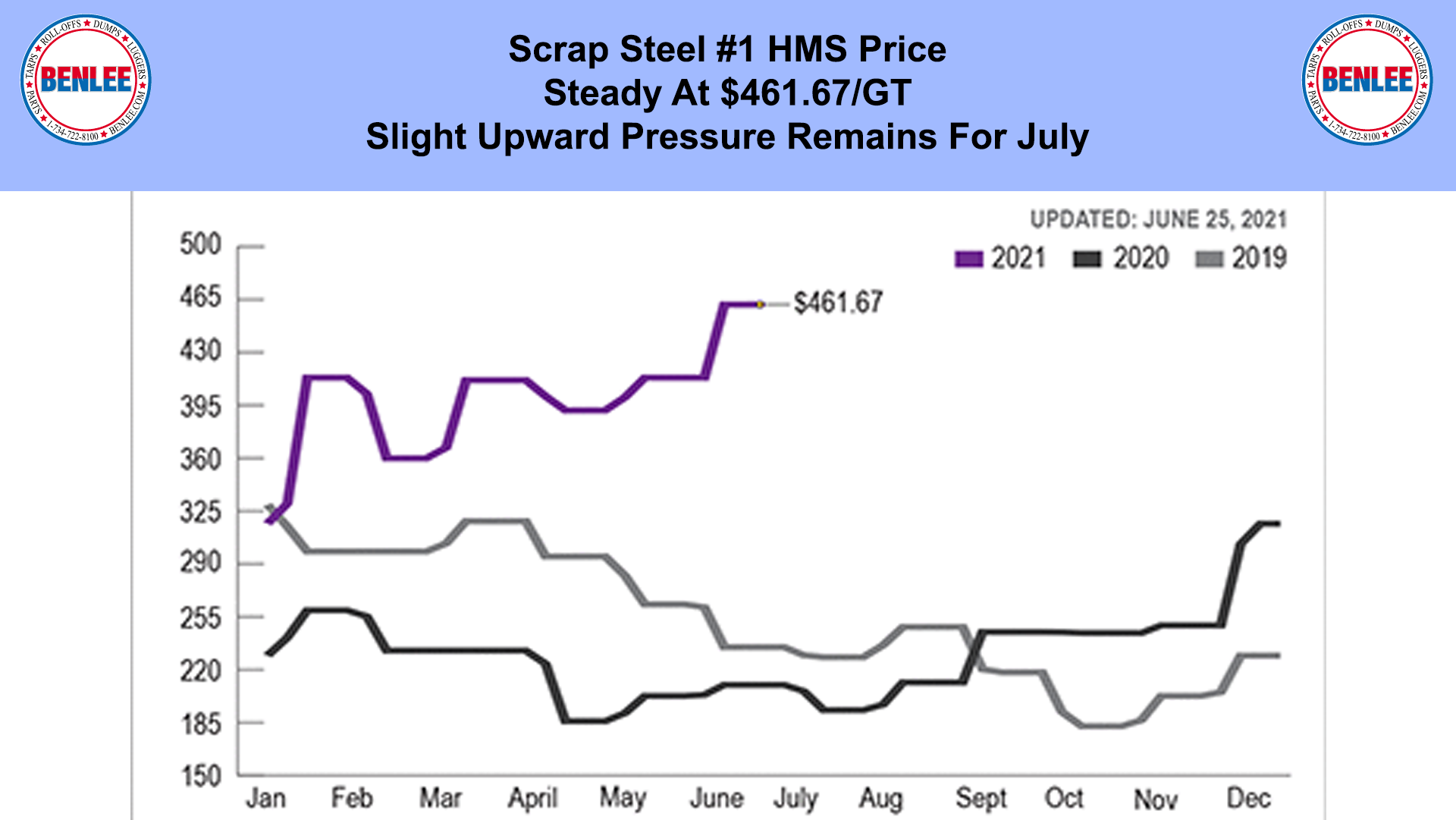

Scrap steel #1 HMS price was steady at $461.67/GT, as slight upward pressure remains for July.

Copper price rose to $4.28/lb., 10% off the recent high on good demand and China releasing copper stockpiles.

Aluminum price rose to $1.11/lb., 2,446/mt. on good demand and China releasing Aluminum stockpiles.

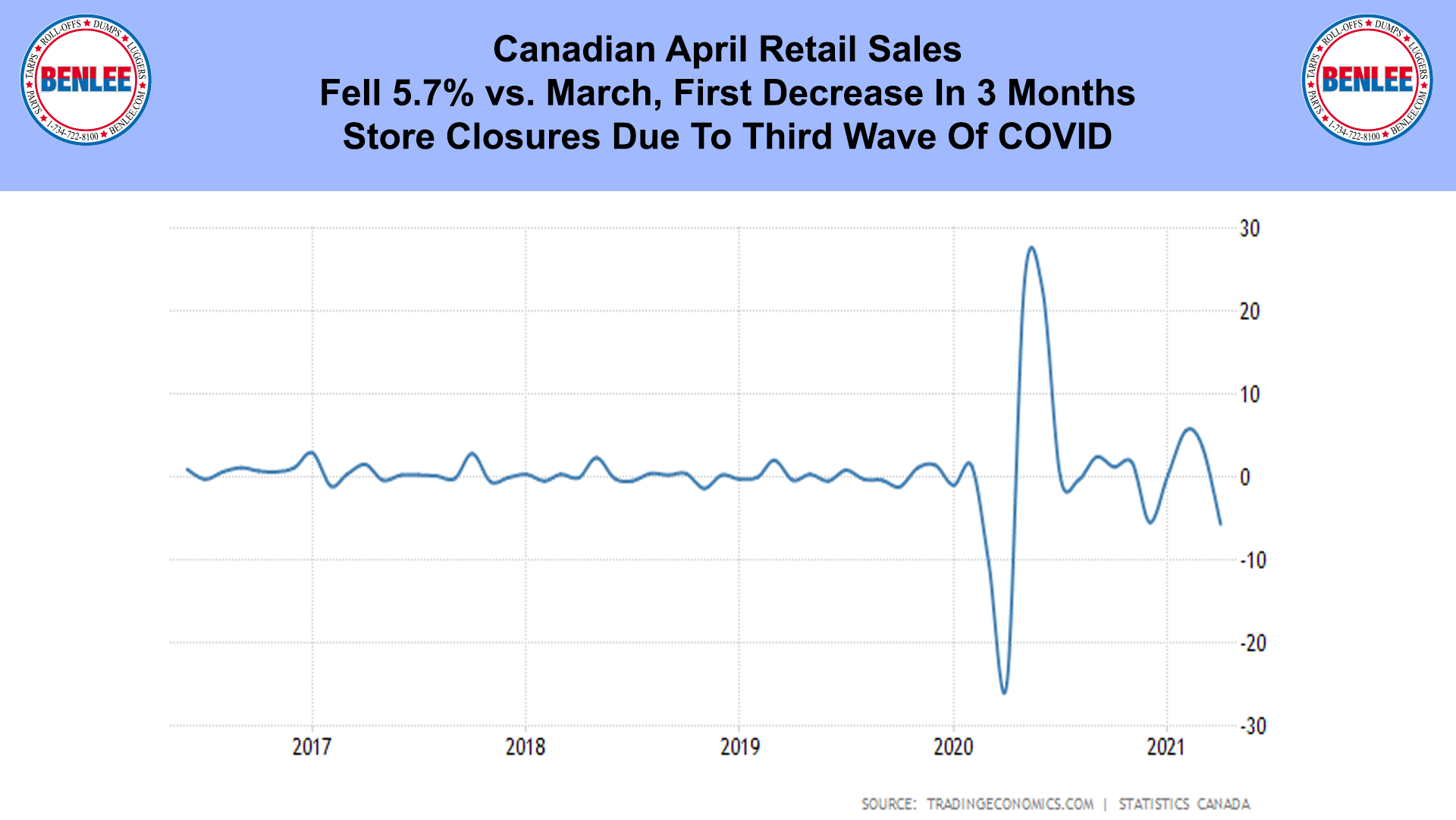

Canadian April retail sales fell 5.7% vs. March, the first decrease in 3 months, mainly due to store closures due to the third wave of COVID.

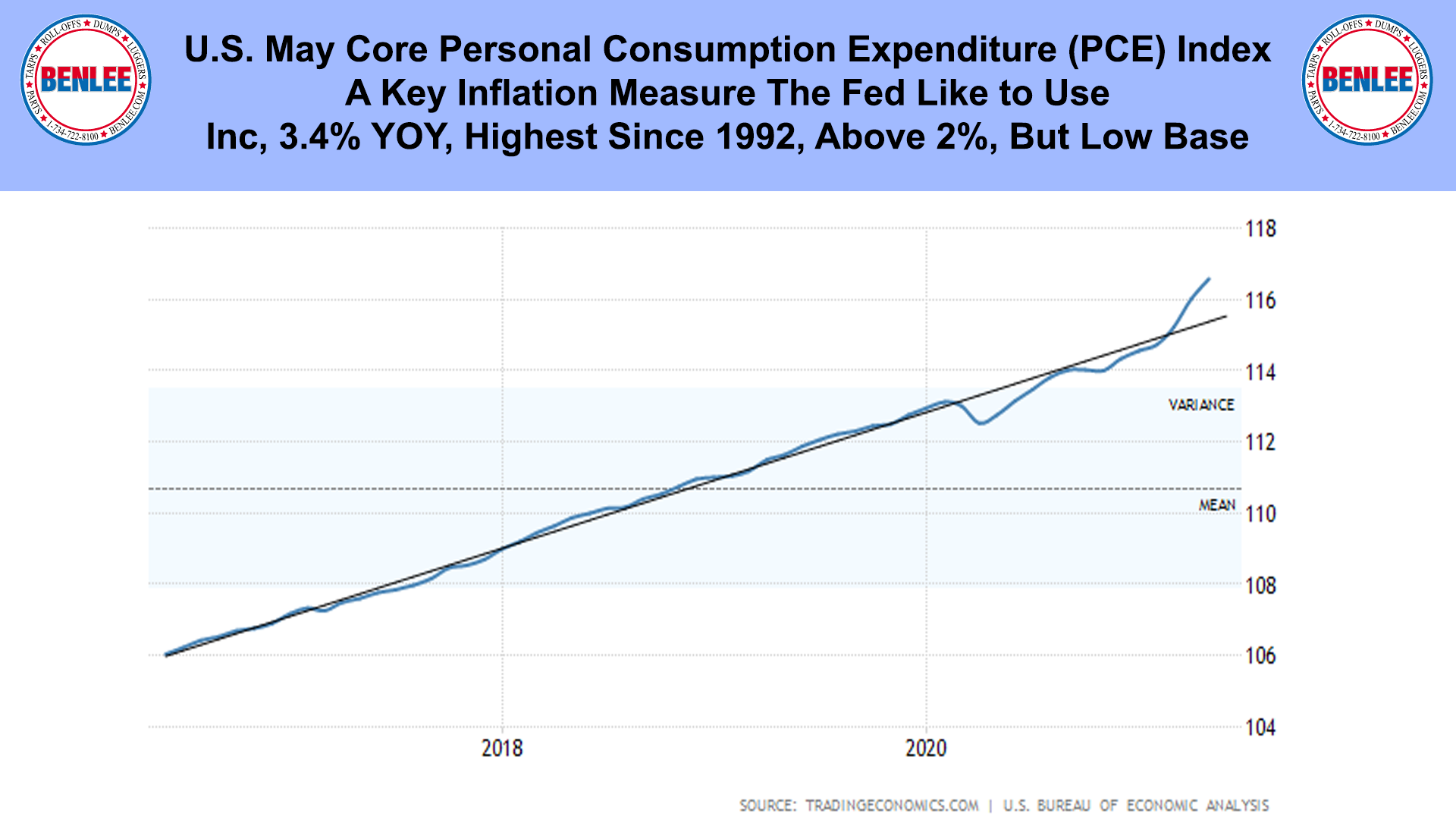

U.S. May core personal consumption expenditure (PCE) index is a key inflation measure the Feds like to use. Inflation increased 3.4% year over year, the highest since 1992, above the 2% Fed target, but that was from a low base.

.png)

U.S. Q1 GDP, grew at 6.4%, which is the 2nd estimate. Growth could be 9% in Q2. There was 2.2% average growth in the 2 years pre COVID. Unfortunately, the 2017 tax cut forecast of 4 and 5% growth never happened.

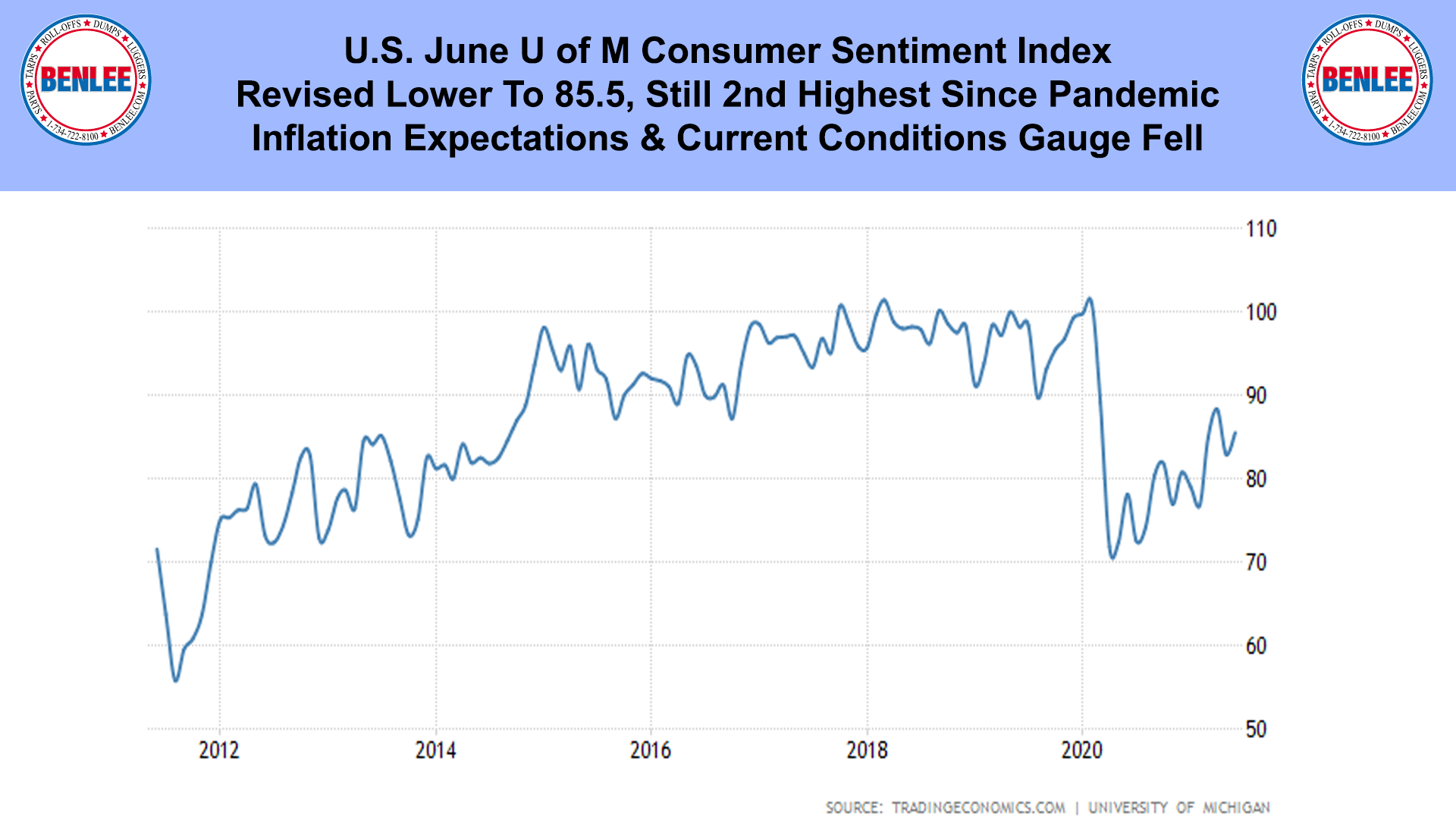

U.S. June U of M consumer sentiment index was revised lower to 85.5, still the 2nd highest since the pandemic. Inflation expectations and the current conditions gauge, fell.

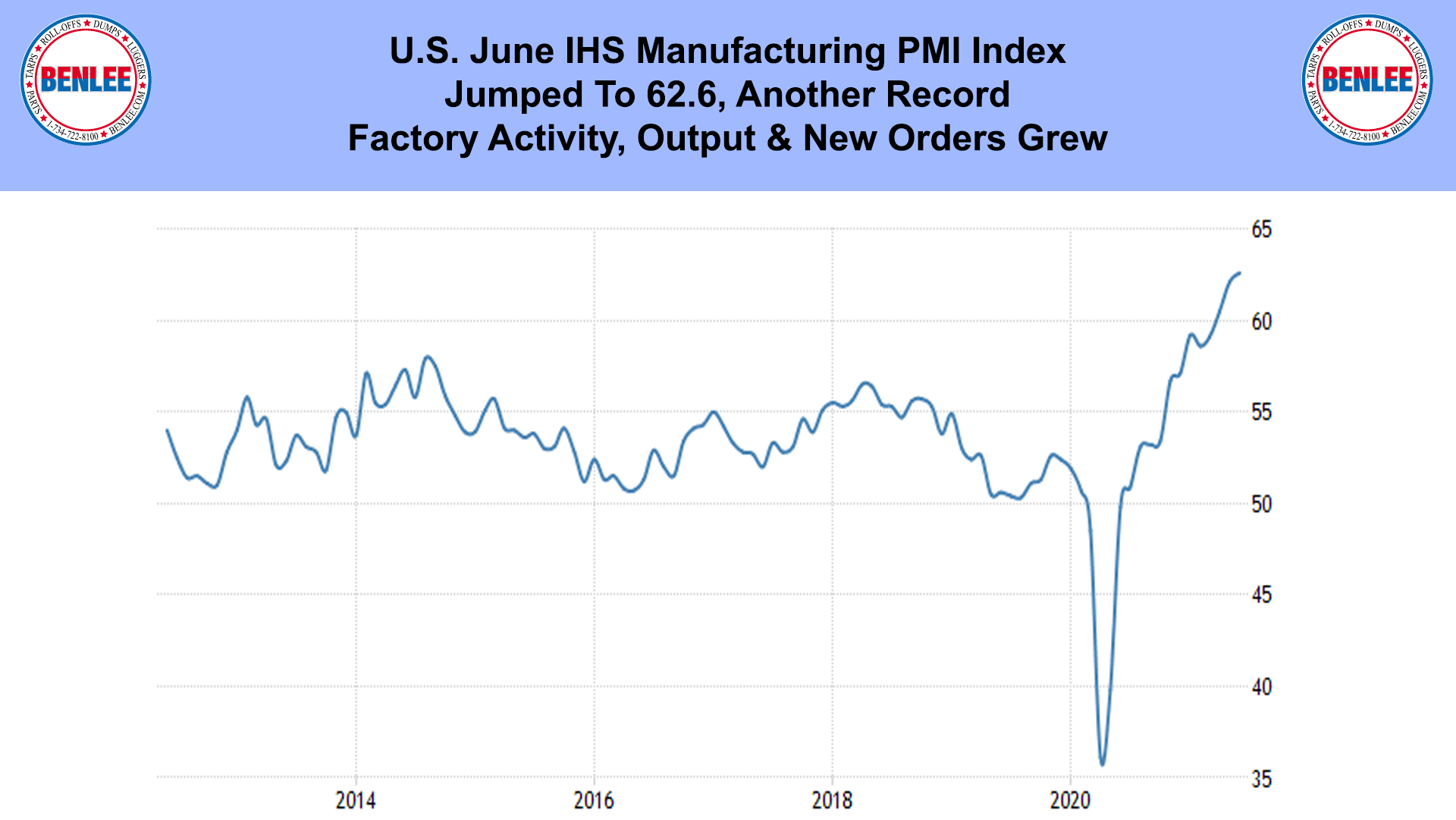

U.S. June IHS manufacturing PMI index jumped to 62.6, another record. Factory activity, output and new orders grew.

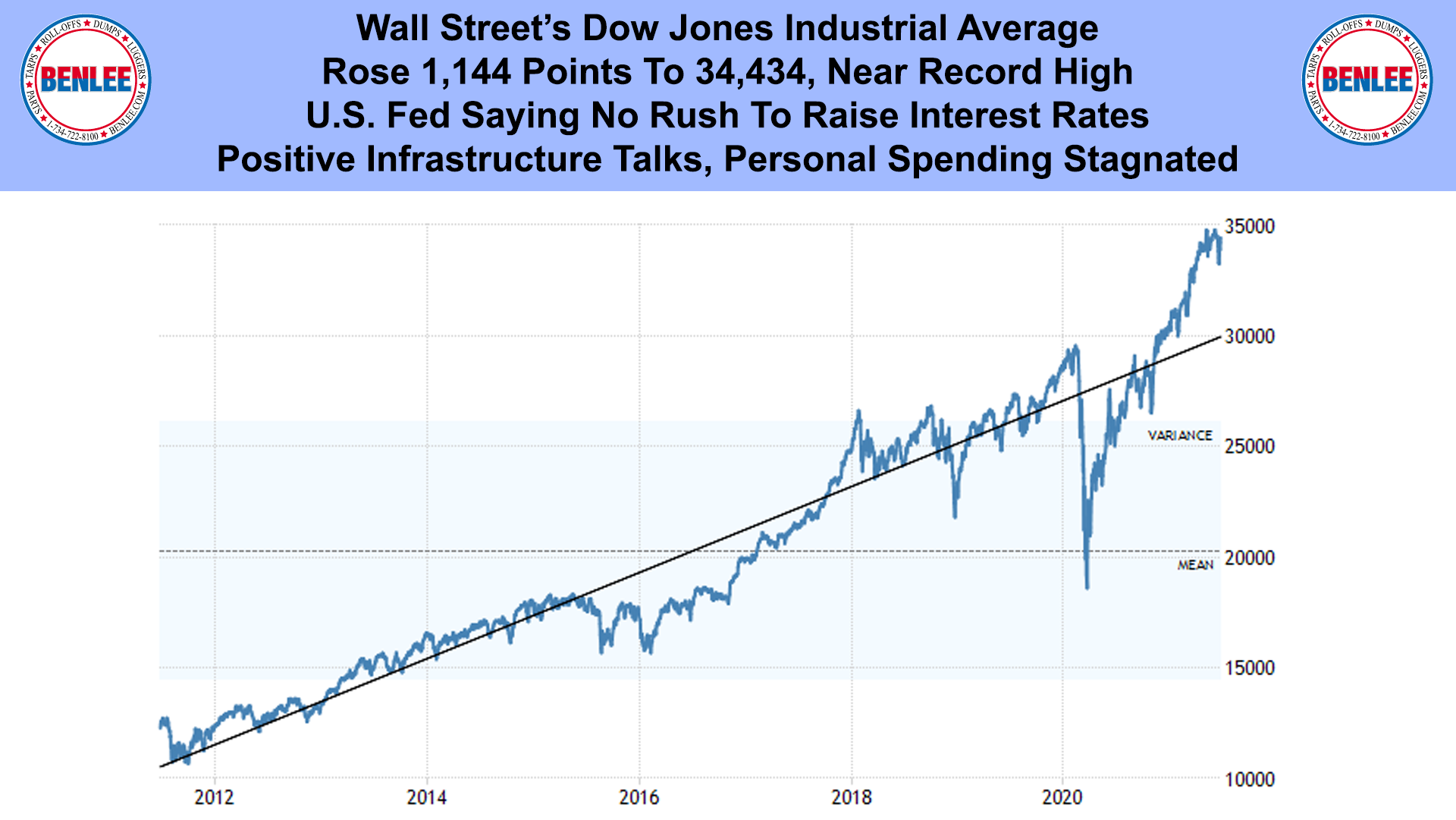

Wall Street’s Dow Jones Industrial Average rose 1,144 points to 34,434, near a record high as the U.S. Federal Reserve said there was no rush to raise interest rates. Also, there were positive infrastructure talks, but personal spending stagnated.

Member

Member